Advertisement

Tune Protect Group Berhad's (KLSE:TUNEPRO) Subdued P/S Might Signal An Opportunity

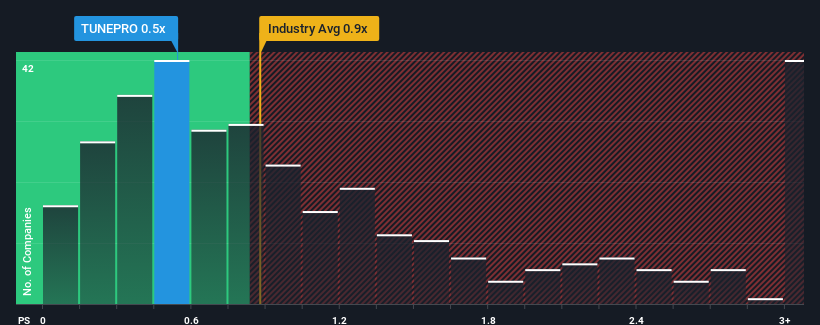

With a median price-to-sales (or "P/S") ratio of close to 0.7x in the Insurance industry in Malaysia, you could be forgiven for feeling indifferent about Tune Protect Group Berhad's (KLSE:TUNEPRO) P/S ratio of 0.5x. Although, it's not wise to simply ignore the P/S without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

See our latest analysis for Tune Protect Group Berhad

How Tune Protect Group Berhad Has Been Performing

With revenue growth that's superior to most other companies of late, Tune Protect Group Berhad has been doing relatively well. Perhaps the market is expecting this level of performance to taper off, keeping the P/S from soaring. If the company manages to stay the course, then investors should be rewarded with a share price that matches its revenue figures.

Keen to find out how analysts think Tune Protect Group Berhad's future stacks up against the industry? In that case, our free report is a great place to start .Is There Some Revenue Growth Forecasted For Tune Protect Group Berhad?

There's an inherent assumption that a company should be matching the industry for P/S ratios like Tune Protect Group Berhad's to be considered reasonable.

If we review the last year of revenue growth, the company posted a worthy increase of 13%. The latest three year period has also seen an excellent 71% overall rise in revenue, aided somewhat by its short-term performance. Therefore, it's fair to say the revenue growth recently has been superb for the company.

Shifting to the future, estimates from the one analyst covering the company suggest revenue should grow by 11% per year over the next three years. That's shaping up to be materially higher than the 6.9% per annum growth forecast for the broader industry.

With this in consideration, we find it intriguing that Tune Protect Group Berhad's P/S is closely matching its industry peers. It may be that most investors aren't convinced the company can achieve future growth expectations.

What We Can Learn From Tune Protect Group Berhad's P/S?

We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

Despite enticing revenue growth figures that outpace the industry, Tune Protect Group Berhad's P/S isn't quite what we'd expect. When we see a strong revenue outlook, with growth outpacing the industry, we can only assume potential uncertainty around these figures are what might be placing slight pressure on the P/S ratio. At least the risk of a price drop looks to be subdued, but investors seem to think future revenue could see some volatility.

Before you take the next step, you should know about the 1 warning sign for Tune Protect Group Berhad that we have uncovered.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Valuation is complex, but we're here to simplify it.

Discover if Tune Protect Group Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:TUNEPRO

Tune Protect Group Berhad

A financial holding company, provides underwriting and reinsurance services for non-life insurance products in Malaysia and internationally.

Excellent balance sheet with moderate growth potential.

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|12.2% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|17.1% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.7% undervalued

TR

Community Contributor