TH Plantations Berhad's (KLSE:THPLANT) 41% Price Boost Is Out Of Tune With Earnings

The TH Plantations Berhad (KLSE:THPLANT) share price has done very well over the last month, posting an excellent gain of 41%. The last 30 days bring the annual gain to a very sharp 26%.

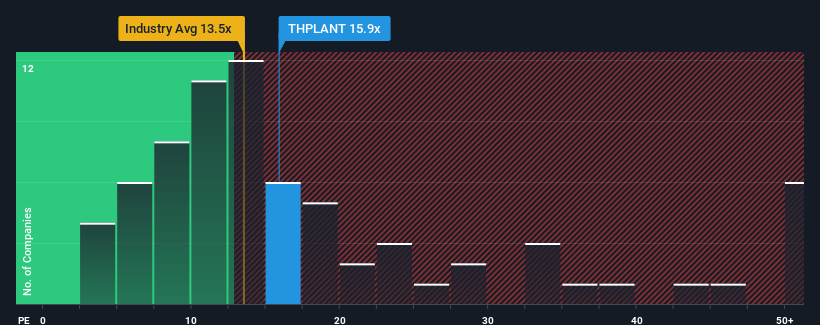

Even after such a large jump in price, there still wouldn't be many who think TH Plantations Berhad's price-to-earnings (or "P/E") ratio of 15.9x is worth a mention when the median P/E in Malaysia is similar at about 16x. While this might not raise any eyebrows, if the P/E ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

TH Plantations Berhad has been struggling lately as its earnings have declined faster than most other companies. One possibility is that the P/E is moderate because investors think the company's earnings trend will eventually fall in line with most others in the market. If you still like the company, you'd want its earnings trajectory to turn around before making any decisions. Or at the very least, you'd be hoping it doesn't keep underperforming if your plan is to pick up some stock while it's not in favour.

View our latest analysis for TH Plantations Berhad

What Are Growth Metrics Telling Us About The P/E?

There's an inherent assumption that a company should be matching the market for P/E ratios like TH Plantations Berhad's to be considered reasonable.

Retrospectively, the last year delivered a frustrating 9.1% decrease to the company's bottom line. This has erased any of its gains during the last three years, with practically no change in EPS being achieved in total. Accordingly, shareholders probably wouldn't have been overly satisfied with the unstable medium-term growth rates.

Turning to the outlook, the next year should bring diminished returns, with earnings decreasing 22% as estimated by the dual analysts watching the company. With the market predicted to deliver 16% growth , that's a disappointing outcome.

In light of this, it's somewhat alarming that TH Plantations Berhad's P/E sits in line with the majority of other companies. It seems most investors are hoping for a turnaround in the company's business prospects, but the analyst cohort is not so confident this will happen. There's a good chance these shareholders are setting themselves up for future disappointment if the P/E falls to levels more in line with the negative growth outlook.

The Final Word

Its shares have lifted substantially and now TH Plantations Berhad's P/E is also back up to the market median. Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

Our examination of TH Plantations Berhad's analyst forecasts revealed that its outlook for shrinking earnings isn't impacting its P/E as much as we would have predicted. When we see a poor outlook with earnings heading backwards, we suspect share price is at risk of declining, sending the moderate P/E lower. This places shareholders' investments at risk and potential investors in danger of paying an unnecessary premium.

Having said that, be aware TH Plantations Berhad is showing 3 warning signs in our investment analysis, and 1 of those is potentially serious.

If these risks are making you reconsider your opinion on TH Plantations Berhad, explore our interactive list of high quality stocks to get an idea of what else is out there.

If you're looking to trade TH Plantations Berhad, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if TH Plantations Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:THPLANT

TH Plantations Berhad

An investment holding company, engages in the cultivation of oil palm in Malaysia and Indonesia.

Undervalued with solid track record and pays a dividend.

Market Insights

Community Narratives