Advertisement

I Built A List Of Growing Companies And QL Resources Berhad (KLSE:QL) Made The Cut

Like a puppy chasing its tail, some new investors often chase 'the next big thing', even if that means buying 'story stocks' without revenue, let alone profit. And in their study titled Who Falls Prey to the Wolf of Wall Street?' Leuz et. al. found that it is 'quite common' for investors to lose money by buying into 'pump and dump' schemes.

If, on the other hand, you like companies that have revenue, and even earn profits, then you may well be interested in QL Resources Berhad (KLSE:QL). Even if the shares are fully valued today, most capitalists would recognize its profits as the demonstration of steady value generation. In comparison, loss making companies act like a sponge for capital - but unlike such a sponge they do not always produce something when squeezed.

Check out our latest analysis for QL Resources Berhad

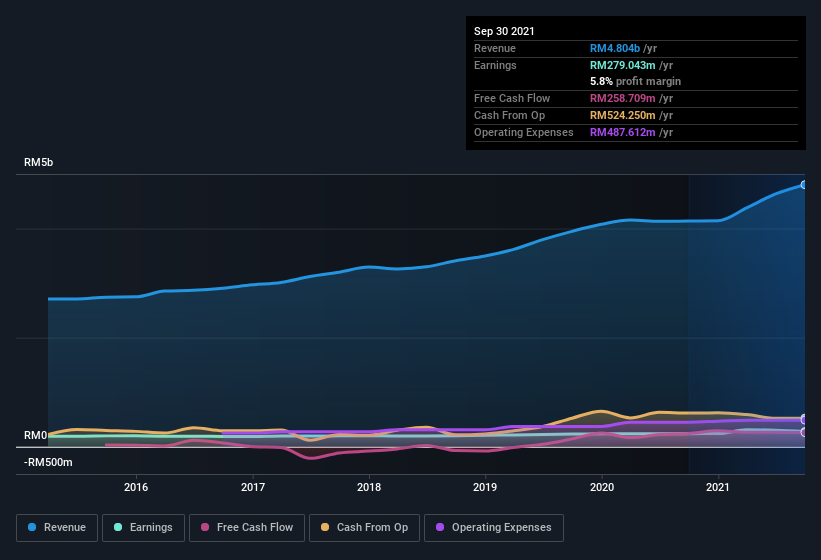

QL Resources Berhad's Earnings Per Share Are Growing.

If a company can keep growing earnings per share (EPS) long enough, its share price will eventually follow. It's no surprise, then, that I like to invest in companies with EPS growth. Over the last three years, QL Resources Berhad has grown EPS by 11% per year. That growth rate is fairly good, assuming the company can keep it up.

Careful consideration of revenue growth and earnings before interest and taxation (EBIT) margins can help inform a view on the sustainability of the recent profit growth. While QL Resources Berhad did well to grow revenue over the last year, EBIT margins were dampened at the same time. So it seems the future my hold further growth, especially if EBIT margins can stabilize.

In the chart below, you can see how the company has grown earnings, and revenue, over time. Click on the chart to see the exact numbers.

In investing, as in life, the future matters more than the past. So why not check out this free interactive visualization of QL Resources Berhad's forecast profits?

Are QL Resources Berhad Insiders Aligned With All Shareholders?

I like company leaders to have some skin in the game, so to speak, because it increases alignment of incentives between the people running the business, and its true owners. So it is good to see that QL Resources Berhad insiders have a significant amount of capital invested in the stock. Indeed, they have a glittering mountain of wealth invested in it, currently valued at RM445m. I would find that kind of skin in the game quite encouraging, if I owned shares, since it would ensure that the leaders of the company would also experience my success, or failure, with the stock.

It's good to see that insiders are invested in the company, but are remuneration levels reasonable? A brief analysis of the CEO compensation suggests they are. For companies with market capitalizations between RM8.4b and RM27b, like QL Resources Berhad, the median CEO pay is around RM4.3m.

The QL Resources Berhad CEO received RM2.7m in compensation for the year ending . That comes in below the average for similar sized companies, and seems pretty reasonable to me. CEO remuneration levels are not the most important metric for investors, but when the pay is modest, that does support enhanced alignment between the CEO and the ordinary shareholders. It can also be a sign of a culture of integrity, in a broader sense.

Should You Add QL Resources Berhad To Your Watchlist?

As I already mentioned, QL Resources Berhad is a growing business, which is what I like to see. Earnings growth might be the main game for QL Resources Berhad, but the fun does not stop there. With a meaningful level of insider ownership, and reasonable CEO pay, a reasonable mind might conclude that this is one stock worth watching. Even so, be aware that QL Resources Berhad is showing 1 warning sign in our investment analysis , you should know about...

Although QL Resources Berhad certainly looks good to me, I would like it more if insiders were buying up shares. If you like to see insider buying, too, then this free list of growing companies that insiders are buying, could be exactly what you're looking for.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Valuation is complex, but we're here to simplify it.

Discover if QL Resources Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:QL

QL Resources Berhad

An investment holding, operates as an agro-food company in Malaysia, Indonesia, Vietnam, and internationally.

Flawless balance sheet with limited growth.

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

8 followersusers have followed this narrative

5 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$126.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

CO

composite32 on Power Solutions International ·

PSIX The timing of insider sales is a serious question mark

Fair Value:US$37.3845.7% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TA

Talos on Marvell Technology ·

The Great Strategy Swap – Selling "Old Auto" to Buy "Future Light"

Fair Value:US$155.3740.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TA

Talos on NVIDIA ·

Not a Bubble, But the "Industrial Revolution 4.0" Engine

Fair Value:US$294.9238.5% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.6% undervalued

112 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.6% undervalued

946 followersusers have followed this narrative

6 commentsusers have commented on this narrative

24 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3407.2% undervalued

147 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative