Some Nestlé (Malaysia) Berhad (KLSE:NESTLE) Shareholders Look For Exit As Shares Take 26% Pounding

Unfortunately for some shareholders, the Nestlé (Malaysia) Berhad (KLSE:NESTLE) share price has dived 26% in the last thirty days, prolonging recent pain. Instead of being rewarded, shareholders who have already held through the last twelve months are now sitting on a 43% share price drop.

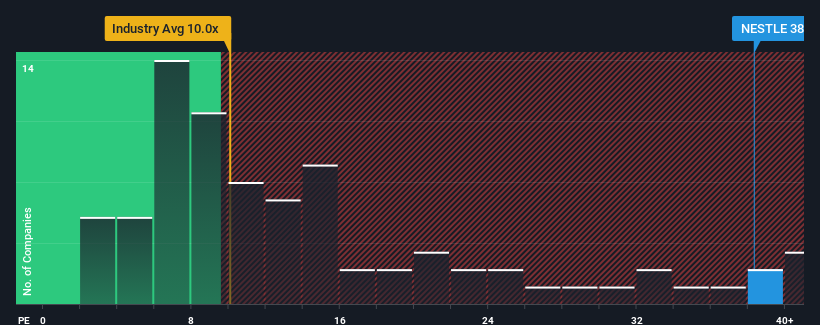

In spite of the heavy fall in price, Nestlé (Malaysia) Berhad may still be sending very bearish signals at the moment with a price-to-earnings (or "P/E") ratio of 38.3x, since almost half of all companies in Malaysia have P/E ratios under 14x and even P/E's lower than 8x are not unusual. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so lofty.

While the market has experienced earnings growth lately, Nestlé (Malaysia) Berhad's earnings have gone into reverse gear, which is not great. One possibility is that the P/E is high because investors think this poor earnings performance will turn the corner. If not, then existing shareholders may be extremely nervous about the viability of the share price.

View our latest analysis for Nestlé (Malaysia) Berhad

Is There Enough Growth For Nestlé (Malaysia) Berhad?

In order to justify its P/E ratio, Nestlé (Malaysia) Berhad would need to produce outstanding growth well in excess of the market.

Taking a look back first, the company's earnings per share growth last year wasn't something to get excited about as it posted a disappointing decline of 37%. The last three years don't look nice either as the company has shrunk EPS by 27% in aggregate. So unfortunately, we have to acknowledge that the company has not done a great job of growing earnings over that time.

Shifting to the future, estimates from the twelve analysts covering the company suggest earnings should grow by 11% each year over the next three years. With the market predicted to deliver 9.5% growth each year, the company is positioned for a comparable earnings result.

In light of this, it's curious that Nestlé (Malaysia) Berhad's P/E sits above the majority of other companies. Apparently many investors in the company are more bullish than analysts indicate and aren't willing to let go of their stock right now. These shareholders may be setting themselves up for disappointment if the P/E falls to levels more in line with the growth outlook.

The Bottom Line On Nestlé (Malaysia) Berhad's P/E

A significant share price dive has done very little to deflate Nestlé (Malaysia) Berhad's very lofty P/E. We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

We've established that Nestlé (Malaysia) Berhad currently trades on a higher than expected P/E since its forecast growth is only in line with the wider market. When we see an average earnings outlook with market-like growth, we suspect the share price is at risk of declining, sending the high P/E lower. Unless these conditions improve, it's challenging to accept these prices as being reasonable.

You should always think about risks. Case in point, we've spotted 2 warning signs for Nestlé (Malaysia) Berhad you should be aware of, and 1 of them is a bit concerning.

If P/E ratios interest you, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

If you're looking to trade Nestlé (Malaysia) Berhad, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Nestlé (Malaysia) Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:NESTLE

Nestlé (Malaysia) Berhad

Manufactures and sells food and beverage products in Malaysia and internationally.

Moderate growth potential with mediocre balance sheet.

Market Insights

Community Narratives