Innoprise Plantations Berhad's (KLSE:INNO) Shareholders Will Receive A Bigger Dividend Than Last Year

Innoprise Plantations Berhad's (KLSE:INNO) dividend will be increasing from last year's payment of the same period to MYR0.038 on 23rd of December. This will take the annual payment to 5.7% of the stock price, which is above what most companies in the industry pay.

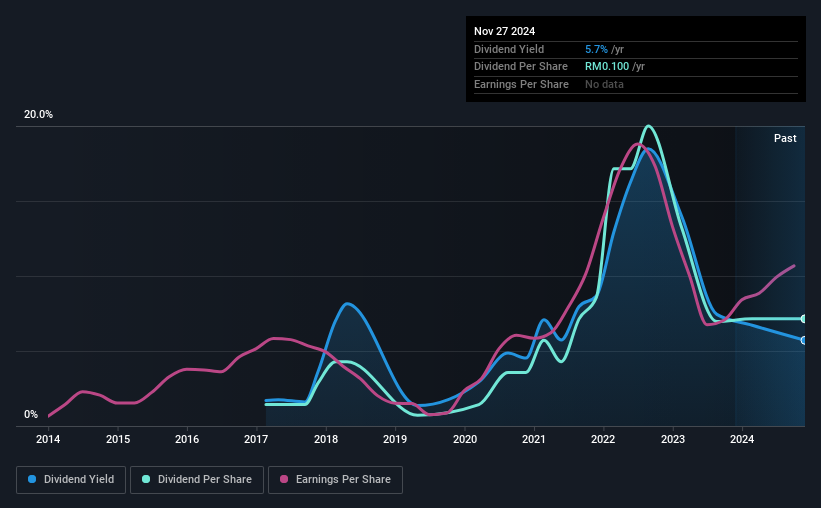

See our latest analysis for Innoprise Plantations Berhad

Innoprise Plantations Berhad's Future Dividend Projections Appear Well Covered By Earnings

While it is great to have a strong dividend yield, we should also consider whether the payment is sustainable. Before making this announcement, Innoprise Plantations Berhad's was paying out quite a large proportion of earnings and 78% of free cash flows. This indicates that the company is more focused on returning cash to shareholders than growing the business, but it is still in a reasonable range to continue with.

Over the next year, EPS could expand by 65.3% if recent trends continue. If the dividend continues on this path, the payout ratio could be 65% by next year, which we think can be pretty sustainable going forward.

Innoprise Plantations Berhad's Dividend Has Lacked Consistency

Even in its relatively short history, the company has reduced the dividend at least once. If the company cuts once, it definitely isn't argument against the possibility of it cutting in the future. Since 2016, the dividend has gone from MYR0.02 total annually to MYR0.10. This means that it has been growing its distributions at 22% per annum over that time. Dividends have grown rapidly over this time, but with cuts in the past we are not certain that this stock will be a reliable source of income in the future.

The Dividend Looks Likely To Grow

With a relatively unstable dividend, it's even more important to evaluate if earnings per share is growing, which could point to a growing dividend in the future. Innoprise Plantations Berhad has impressed us by growing EPS at 65% per year over the past five years. Fast growing earnings are great, but this can rarely be sustained without some reinvestment into the business, which Innoprise Plantations Berhad hasn't been doing.

Our Thoughts On Innoprise Plantations Berhad's Dividend

Overall, we always like to see the dividend being raised, but we don't think Innoprise Plantations Berhad will make a great income stock. While Innoprise Plantations Berhad is earning enough to cover the dividend, we are generally unimpressed with its future prospects. We would probably look elsewhere for an income investment.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. For instance, we've picked out 1 warning sign for Innoprise Plantations Berhad that investors should take into consideration. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:INNO

Innoprise Plantations Berhad

An investment holding company, cultivates oil palms and plantation trees in Malaysia.

Outstanding track record with excellent balance sheet and pays a dividend.

Market Insights

Community Narratives