Genting Plantations Berhad's (KLSE:GENP) Share Price Not Quite Adding Up

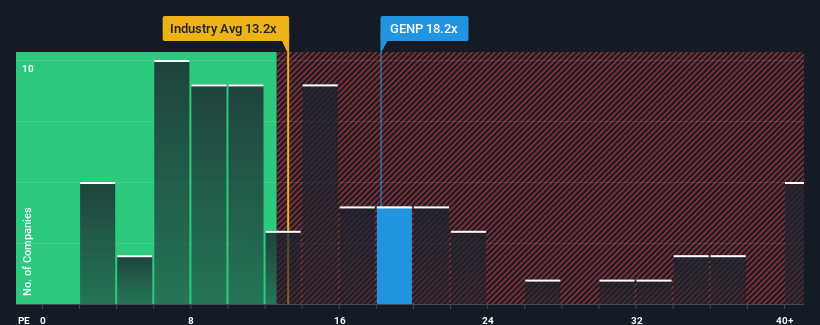

When close to half the companies in Malaysia have price-to-earnings ratios (or "P/E's") below 15x, you may consider Genting Plantations Berhad (KLSE:GENP) as a stock to potentially avoid with its 18.2x P/E ratio. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's as high as it is.

Genting Plantations Berhad's earnings growth of late has been pretty similar to most other companies. One possibility is that the P/E is high because investors think this modest earnings performance will accelerate. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Check out our latest analysis for Genting Plantations Berhad

How Is Genting Plantations Berhad's Growth Trending?

There's an inherent assumption that a company should outperform the market for P/E ratios like Genting Plantations Berhad's to be considered reasonable.

If we review the last year of earnings growth, the company posted a worthy increase of 13%. Still, lamentably EPS has fallen 12% in aggregate from three years ago, which is disappointing. So unfortunately, we have to acknowledge that the company has not done a great job of growing earnings over that time.

Turning to the outlook, the next three years should generate growth of 4.8% per annum as estimated by the eleven analysts watching the company. Meanwhile, the rest of the market is forecast to expand by 14% each year, which is noticeably more attractive.

In light of this, it's alarming that Genting Plantations Berhad's P/E sits above the majority of other companies. Apparently many investors in the company are way more bullish than analysts indicate and aren't willing to let go of their stock at any price. There's a good chance these shareholders are setting themselves up for future disappointment if the P/E falls to levels more in line with the growth outlook.

The Final Word

Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

Our examination of Genting Plantations Berhad's analyst forecasts revealed that its inferior earnings outlook isn't impacting its high P/E anywhere near as much as we would have predicted. When we see a weak earnings outlook with slower than market growth, we suspect the share price is at risk of declining, sending the high P/E lower. Unless these conditions improve markedly, it's very challenging to accept these prices as being reasonable.

It is also worth noting that we have found 1 warning sign for Genting Plantations Berhad that you need to take into consideration.

It's important to make sure you look for a great company, not just the first idea you come across. So take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:GENP

Genting Plantations Berhad

Engages in the oil palm plantation, property development and investment, genomics research and development, and downstream manufacturing activities in Malaysia and Indonesia.

Proven track record with adequate balance sheet.

Similar Companies

Market Insights

Community Narratives