Advertisement

C.I. Holdings Berhad (KLSE:CIHLDG) Will Pay A Larger Dividend Than Last Year At MYR0.20

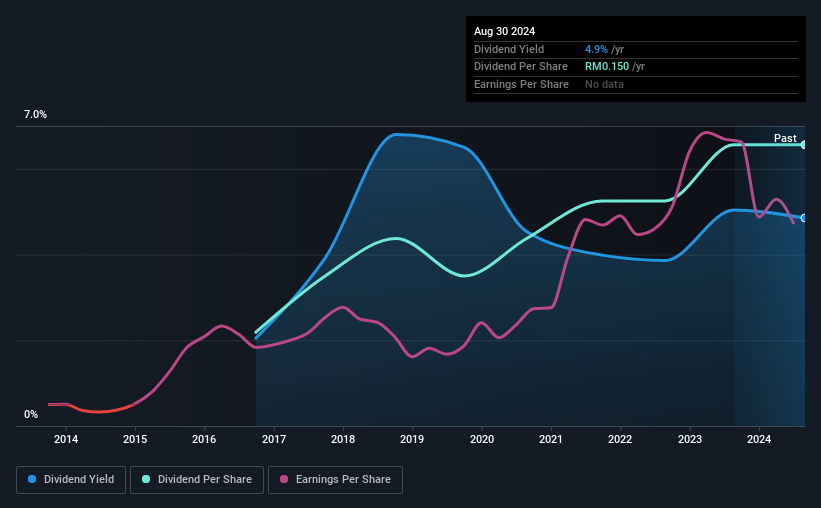

The board of C.I. Holdings Berhad (KLSE:CIHLDG) has announced that the dividend on 14th of October will be increased to MYR0.20, which will be 33% higher than last year's payment of MYR0.15 which covered the same period. This takes the dividend yield to 4.9%, which shareholders will be pleased with.

See our latest analysis for C.I. Holdings Berhad

C.I. Holdings Berhad's Earnings Easily Cover The Distributions

If the payments aren't sustainable, a high yield for a few years won't matter that much. However, C.I. Holdings Berhad's earnings easily cover the dividend. As a result, a large proportion of what it earned was being reinvested back into the business.

If the trend of the last few years continues, EPS will grow by 29.2% over the next 12 months. If the dividend continues along recent trends, we estimate the payout ratio will be 41%, which is in the range that makes us comfortable with the sustainability of the dividend.

C.I. Holdings Berhad's Dividend Has Lacked Consistency

C.I. Holdings Berhad has been paying dividends for a while, but the track record isn't stellar. Due to this, we are a little bit cautious about the dividend consistency over a full economic cycle. The dividend has gone from an annual total of MYR0.05 in 2016 to the most recent total annual payment of MYR0.15. This implies that the company grew its distributions at a yearly rate of about 15% over that duration. C.I. Holdings Berhad has grown distributions at a rapid rate despite cutting the dividend at least once in the past. Companies that cut once often cut again, so we would be cautious about buying this stock solely for the dividend income.

The Dividend Looks Likely To Grow

With a relatively unstable dividend, it's even more important to evaluate if earnings per share is growing, which could point to a growing dividend in the future. C.I. Holdings Berhad has impressed us by growing EPS at 29% per year over the past five years. A low payout ratio gives the company a lot of flexibility, and growing earnings also make it very easy for it to grow the dividend.

We Really Like C.I. Holdings Berhad's Dividend

Overall, a dividend increase is always good, and we think that C.I. Holdings Berhad is a strong income stock thanks to its track record and growing earnings. Distributions are quite easily covered by earnings, which are also being converted to cash flows. Taking this all into consideration, this looks like it could be a good dividend opportunity.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. As an example, we've identified 1 warning sign for C.I. Holdings Berhad that you should be aware of before investing. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:CIHLDG

C.I. Holdings Berhad

An investment holding company, engages in manufacturing, selling, and packing various types of edible oils in Malaysia, Africa, Asia, and internationally.

Flawless balance sheet, good value and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

Nike's Direct-to-Consumer Focus Will Drive Future Growth

Fair Value US$87.90|18.2% undervalued

UN

Community Contributor

Novo Nordisk will dominate GLP-1 market with Ozempic and Wegovy growth

Fair Value US$89.59|12.1% undervalued

BE

Community Contributor

Rheinmetall could get 20-25% of EU-NATO 3%-GDP defence spending

Fair Value €7.57k|82.4% undervalued

NO

Community Contributor