Advertisement

- Malaysia

- /

- Oil and Gas

- /

- KLSE:HIBISCS

These 4 Measures Indicate That Hibiscus Petroleum Berhad (KLSE:HIBISCS) Is Using Debt Reasonably Well

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. As with many other companies Hibiscus Petroleum Berhad (KLSE:HIBISCS) makes use of debt. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for Hibiscus Petroleum Berhad

How Much Debt Does Hibiscus Petroleum Berhad Carry?

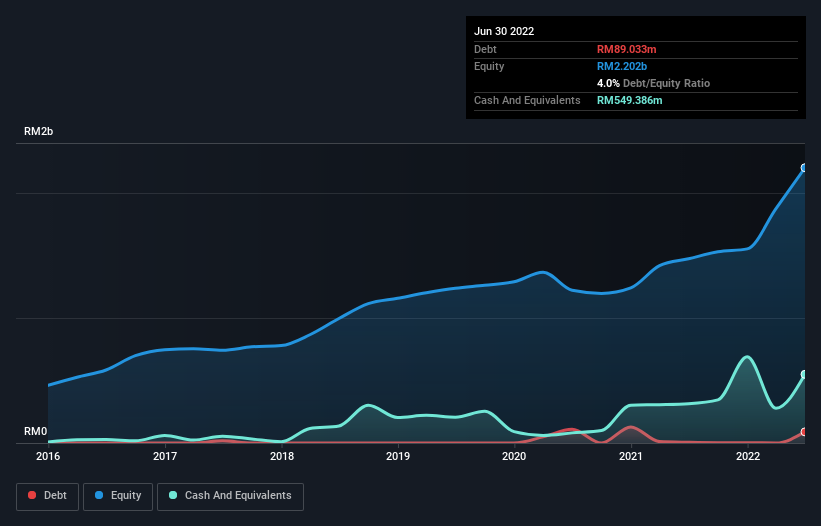

As you can see below, at the end of June 2022, Hibiscus Petroleum Berhad had RM89.0m of debt, up from RM5.90m a year ago. Click the image for more detail. But it also has RM549.4m in cash to offset that, meaning it has RM460.4m net cash.

A Look At Hibiscus Petroleum Berhad's Liabilities

According to the last reported balance sheet, Hibiscus Petroleum Berhad had liabilities of RM1.70b due within 12 months, and liabilities of RM1.61b due beyond 12 months. Offsetting this, it had RM549.4m in cash and RM808.8m in receivables that were due within 12 months. So it has liabilities totalling RM1.95b more than its cash and near-term receivables, combined.

This deficit is considerable relative to its market capitalization of RM1.99b, so it does suggest shareholders should keep an eye on Hibiscus Petroleum Berhad's use of debt. This suggests shareholders would be heavily diluted if the company needed to shore up its balance sheet in a hurry. Despite its noteworthy liabilities, Hibiscus Petroleum Berhad boasts net cash, so it's fair to say it does not have a heavy debt load!

Even more impressive was the fact that Hibiscus Petroleum Berhad grew its EBIT by 136% over twelve months. If maintained that growth will make the debt even more manageable in the years ahead. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Hibiscus Petroleum Berhad's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. While Hibiscus Petroleum Berhad has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Over the most recent three years, Hibiscus Petroleum Berhad recorded free cash flow worth 57% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Summing Up

While Hibiscus Petroleum Berhad does have more liabilities than liquid assets, it also has net cash of RM460.4m. And we liked the look of last year's 136% year-on-year EBIT growth. So we are not troubled with Hibiscus Petroleum Berhad's debt use. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. For example, we've discovered 2 warning signs for Hibiscus Petroleum Berhad (1 doesn't sit too well with us!) that you should be aware of before investing here.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

Valuation is complex, but we're here to simplify it.

Discover if Hibiscus Petroleum Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:HIBISCS

Hibiscus Petroleum Berhad

Engages in the exploration, development, and sale of oil and gas.

Undervalued with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

100% Patient Improvement in trial puts this $16M Biotech on the radar

Fair Value US$5.30|74.9% undervalued

JO

Community Contributor

PayPal's Future Growth Through Venmo and Merchant Solutions

Fair Value US$105.25|35.1% undervalued

ZW

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$26.54|1.5% undervalued

BL

Community Contributor