Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies RGB International Bhd. (KLSE:RGB) makes use of debt. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

Check out our latest analysis for RGB International Bhd

How Much Debt Does RGB International Bhd Carry?

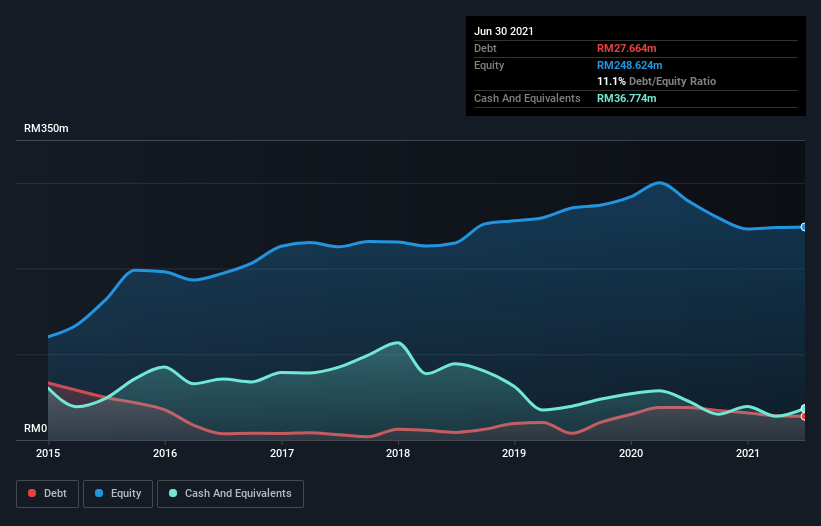

As you can see below, RGB International Bhd had RM27.7m of debt at June 2021, down from RM37.8m a year prior. But on the other hand it also has RM36.8m in cash, leading to a RM9.11m net cash position.

How Strong Is RGB International Bhd's Balance Sheet?

We can see from the most recent balance sheet that RGB International Bhd had liabilities of RM129.0m falling due within a year, and liabilities of RM24.9m due beyond that. On the other hand, it had cash of RM36.8m and RM124.8m worth of receivables due within a year. So it actually has RM7.70m more liquid assets than total liabilities.

This surplus suggests that RGB International Bhd has a conservative balance sheet, and could probably eliminate its debt without much difficulty. Simply put, the fact that RGB International Bhd has more cash than debt is arguably a good indication that it can manage its debt safely. The balance sheet is clearly the area to focus on when you are analysing debt. But you can't view debt in total isolation; since RGB International Bhd will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

In the last year RGB International Bhd had a loss before interest and tax, and actually shrunk its revenue by 44%, to RM189m. That makes us nervous, to say the least.

So How Risky Is RGB International Bhd?

While RGB International Bhd lost money on an earnings before interest and tax (EBIT) level, it actually generated positive free cash flow RM6.4m. So although it is loss-making, it doesn't seem to have too much near-term balance sheet risk, keeping in mind the net cash. We'll feel more comfortable with the stock once EBIT is positive, given the lacklustre revenue growth. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. For example, we've discovered 2 warning signs for RGB International Bhd (1 can't be ignored!) that you should be aware of before investing here.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KLSE:RGB

RGB International Bhd

An investment holding company, engages in the manufacturing, marketing, trading, and sale of electronic gaming machines (EGM) and equipment under the RGBGames brand.

Flawless balance sheet with moderate growth potential.

Market Insights

Community Narratives