Advertisement

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, Borneo Oil Berhad (KLSE:BORNOIL) does carry debt. But should shareholders be worried about its use of debt?

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we think about a company's use of debt, we first look at cash and debt together.

View our latest analysis for Borneo Oil Berhad

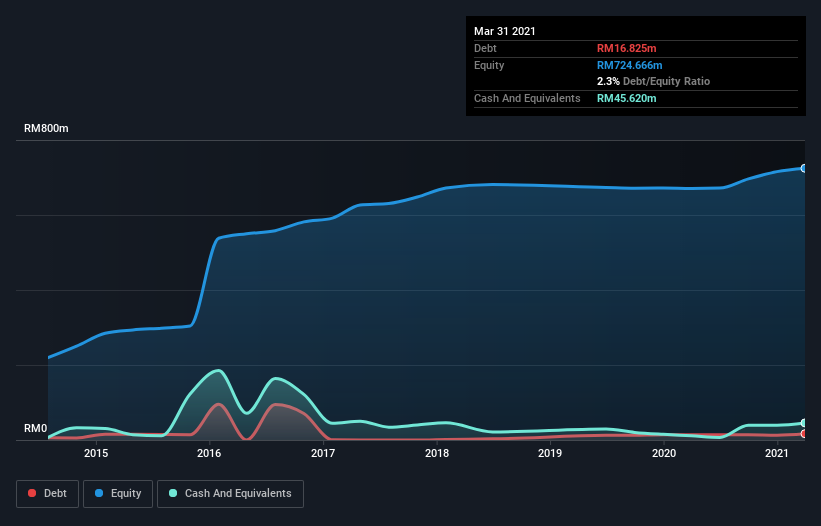

How Much Debt Does Borneo Oil Berhad Carry?

You can click the graphic below for the historical numbers, but it shows that as of March 2021 Borneo Oil Berhad had RM16.8m of debt, an increase on RM14.3m, over one year. But it also has RM45.6m in cash to offset that, meaning it has RM28.8m net cash.

How Healthy Is Borneo Oil Berhad's Balance Sheet?

We can see from the most recent balance sheet that Borneo Oil Berhad had liabilities of RM19.0m falling due within a year, and liabilities of RM36.9m due beyond that. Offsetting this, it had RM45.6m in cash and RM41.3m in receivables that were due within 12 months. So it actually has RM31.0m more liquid assets than total liabilities.

This short term liquidity is a sign that Borneo Oil Berhad could probably pay off its debt with ease, as its balance sheet is far from stretched. Succinctly put, Borneo Oil Berhad boasts net cash, so it's fair to say it does not have a heavy debt load! When analysing debt levels, the balance sheet is the obvious place to start. But you can't view debt in total isolation; since Borneo Oil Berhad will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Over 12 months, Borneo Oil Berhad made a loss at the EBIT level, and saw its revenue drop to RM52m, which is a fall of 47%. That makes us nervous, to say the least.

So How Risky Is Borneo Oil Berhad?

By their very nature companies that are losing money are more risky than those with a long history of profitability. And the fact is that over the last twelve months Borneo Oil Berhad lost money at the earnings before interest and tax (EBIT) line. Indeed, in that time it burnt through RM30m of cash and made a loss of RM5.7m. Given it only has net cash of RM28.8m, the company may need to raise more capital if it doesn't reach break-even soon. Overall, its balance sheet doesn't seem overly risky, at the moment, but we're always cautious until we see the positive free cash flow. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. Be aware that Borneo Oil Berhad is showing 3 warning signs in our investment analysis , and 1 of those is a bit unpleasant...

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

If you're looking for stocks to buy, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Borneo Oil Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KLSE:BORNOIL

Borneo Oil Berhad

An investment holding company, operates and franchises fast food restaurants in Malaysia and Australia.

Slight with imperfect balance sheet.

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|19.2% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|86.0% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|14.3% undervalued

CH

Community Contributor