Advertisement

- Malaysia

- /

- Consumer Durables

- /

- KLSE:RKI

Why It Might Not Make Sense To Buy Rhong Khen International Berhad (KLSE:RKI) For Its Upcoming Dividend

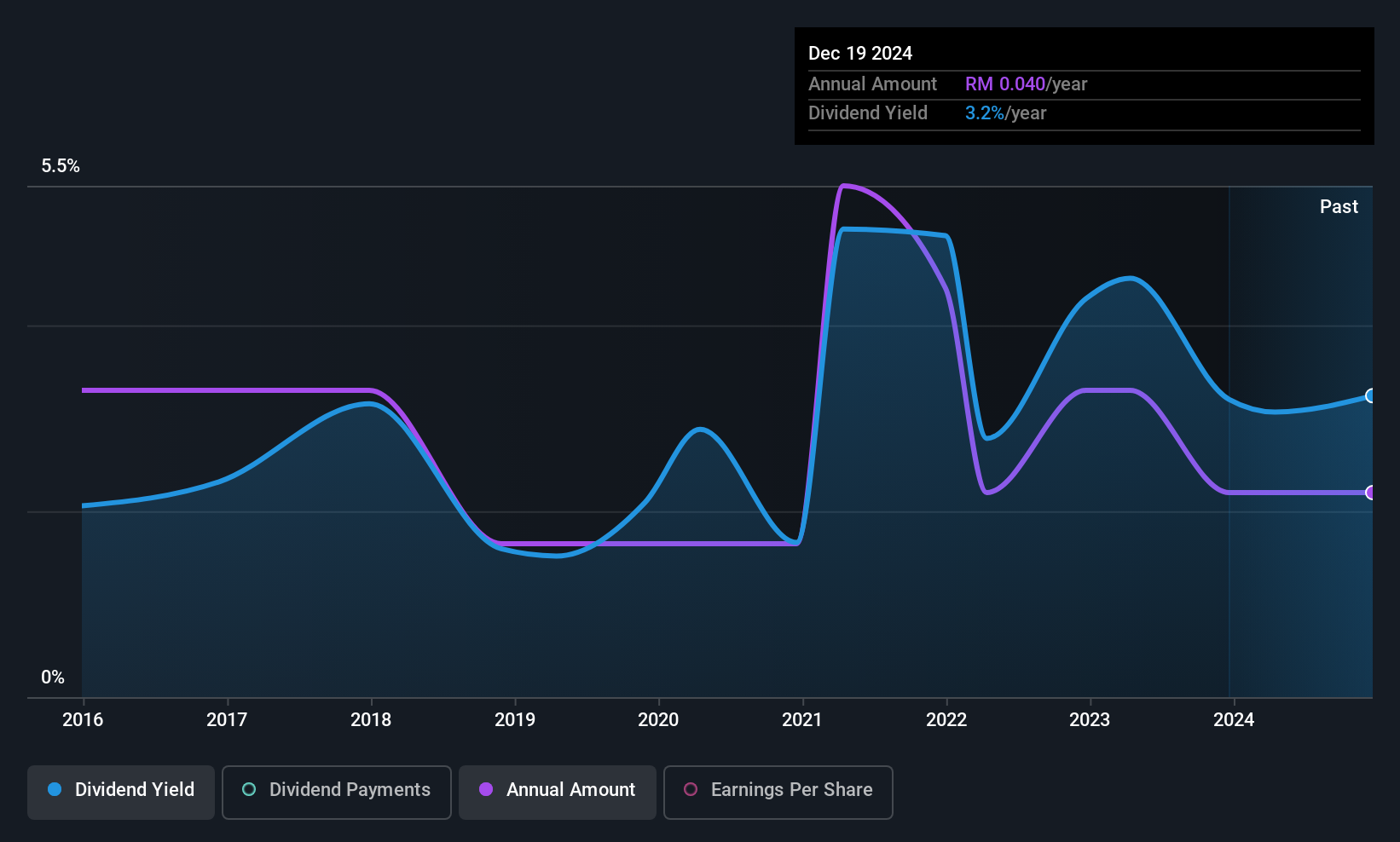

Regular readers will know that we love our dividends at Simply Wall St, which is why it's exciting to see Rhong Khen International Berhad (KLSE:RKI) is about to trade ex-dividend in the next 3 days. The ex-dividend date is usually set to be two business days before the record date, which is the cut-off date on which you must be present on the company's books as a shareholder in order to receive the dividend. The ex-dividend date is of consequence because whenever a stock is bought or sold, the trade can take two business days or more to settle. Meaning, you will need to purchase Rhong Khen International Berhad's shares before the 4th of December to receive the dividend, which will be paid on the 12th of December.

The company's next dividend payment will be RM00.04 per share, on the back of last year when the company paid a total of RM0.04 to shareholders. Based on the last year's worth of payments, Rhong Khen International Berhad has a trailing yield of 3.8% on the current stock price of RM01.05. We love seeing companies pay a dividend, but it's also important to be sure that laying the golden eggs isn't going to kill our golden goose! That's why we should always check whether the dividend payments appear sustainable, and if the company is growing.

Dividends are usually paid out of company profits, so if a company pays out more than it earned then its dividend is usually at greater risk of being cut. Rhong Khen International Berhad is paying out just 12% of its profit after tax, which is comfortably low and leaves plenty of breathing room in the case of adverse events. A useful secondary check can be to evaluate whether Rhong Khen International Berhad generated enough free cash flow to afford its dividend. It paid out 95% of its free cash flow in the form of dividends last year, which is outside the comfort zone for most businesses. Cash flows are usually much more volatile than earnings, so this could be a temporary effect - but we'd generally want to look more closely here.

Rhong Khen International Berhad paid out less in dividends than it reported in profits, but unfortunately it didn't generate enough cash to cover the dividend. Cash is king, as they say, and were Rhong Khen International Berhad to repeatedly pay dividends that aren't well covered by cashflow, we would consider this a warning sign.

View our latest analysis for Rhong Khen International Berhad

Click here to see how much of its profit Rhong Khen International Berhad paid out over the last 12 months.

Have Earnings And Dividends Been Growing?

Companies that aren't growing their earnings can still be valuable, but it is even more important to assess the sustainability of the dividend if it looks like the company will struggle to grow. If earnings fall far enough, the company could be forced to cut its dividend. With that in mind, we're not enthused to see that Rhong Khen International Berhad's earnings per share have remained effectively flat over the past five years. It's better than seeing them drop, certainly, but over the long term, all of the best dividend stocks are able to meaningfully grow their earnings per share.

Another key way to measure a company's dividend prospects is by measuring its historical rate of dividend growth. Rhong Khen International Berhad's dividend payments per share have declined at 4.0% per year on average over the past 10 years, which is uninspiring.

Final Takeaway

Is Rhong Khen International Berhad worth buying for its dividend? It's disappointing to see earnings per share have fallen slightly, even though Rhong Khen International Berhad is paying out less than half its income as dividends. It's also paying out an uncomfortably high percentage of its cash flow, which makes us wonder just how sustainable the dividend really is. With the way things are shaping up from a dividend perspective, we'd be inclined to steer clear of Rhong Khen International Berhad.

Having said that, if you're looking at this stock without much concern for the dividend, you should still be familiar of the risks involved with Rhong Khen International Berhad. For example, Rhong Khen International Berhad has 3 warning signs (and 1 which is a bit unpleasant) we think you should know about.

A common investing mistake is buying the first interesting stock you see. Here you can find a full list of high-yield dividend stocks.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:RKI

Rhong Khen International Berhad

An investment holding company, manufactures and sells wooden household furniture and components in Malaysia, Vietnam, and Thailand.

Flawless balance sheet with proven track record.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

932 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

139 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative