Advertisement

- Malaysia

- /

- Consumer Durables

- /

- KLSE:RKI

Rhong Khen International Berhad (KLSE:RKI) Will Pay A Smaller Dividend Than Last Year

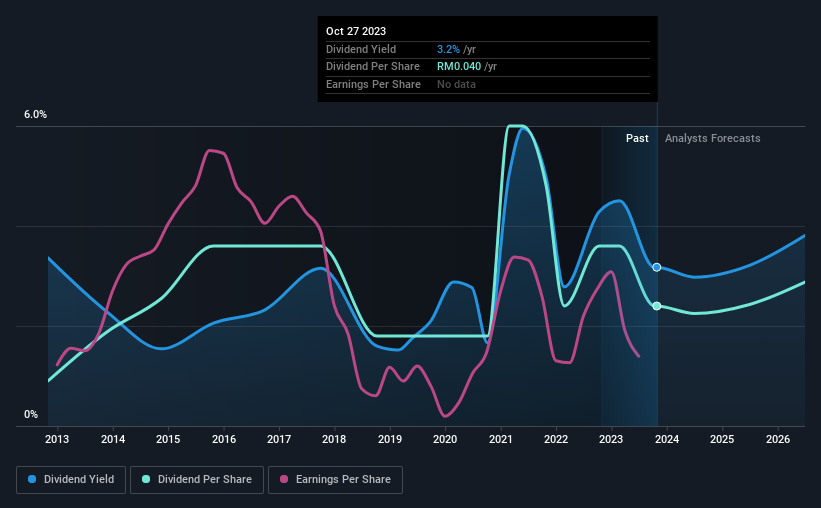

Rhong Khen International Berhad (KLSE:RKI) has announced that on 12th of January, it will be paying a dividend ofMYR0.03, which a reduction from last year's comparable dividend. This means that the annual payment is 3.2% of the current stock price, which is lower than what the rest of the industry is paying.

Check out our latest analysis for Rhong Khen International Berhad

Rhong Khen International Berhad's Dividend Is Well Covered By Earnings

Even a low dividend yield can be attractive if it is sustained for years on end. However, Rhong Khen International Berhad's earnings easily cover the dividend. As a result, a large proportion of what it earned was being reinvested back into the business.

Looking forward, earnings per share is forecast to rise by 7.9% over the next year. Assuming the dividend continues along recent trends, we think the payout ratio could be 33% by next year, which is in a pretty sustainable range.

Dividend Volatility

Although the company has a long dividend history, it has been cut at least once in the last 10 years. Since 2013, the annual payment back then was MYR0.015, compared to the most recent full-year payment of MYR0.04. This means that it has been growing its distributions at 10% per annum over that time. Despite the rapid growth in the dividend over the past number of years, we have seen the payments go down the past as well, so that makes us cautious.

The Dividend Looks Likely To Grow

With a relatively unstable dividend, it's even more important to evaluate if earnings per share is growing, which could point to a growing dividend in the future. Rhong Khen International Berhad has impressed us by growing EPS at 13% per year over the past five years. Growth in EPS bodes well for the dividend, as does the low payout ratio that the company is currently reporting.

We Really Like Rhong Khen International Berhad's Dividend

It is generally not great to see the dividend being cut, but we don't think this should happen much if at all in the future given that Rhong Khen International Berhad has the makings of a solid income stock moving forward. Reducing the amount it is paying as a dividend can protect the company's balance sheet, keeping the dividend sustainable for longer. All of these factors considered, we think this has solid potential as a dividend stock.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. As an example, we've identified 2 warning signs for Rhong Khen International Berhad that you should be aware of before investing. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:RKI

Rhong Khen International Berhad

An investment holding company, manufactures and sells wooden household furniture and components in Malaysia, Vietnam, and Thailand.

Flawless balance sheet with moderate growth potential.

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|44.5% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|46.1% undervalued

TO

Community Contributor