- Malaysia

- /

- Consumer Durables

- /

- KLSE:MILUX

Optimistic Investors Push Milux Corporation Berhad (KLSE:MILUX) Shares Up 26% But Growth Is Lacking

Milux Corporation Berhad (KLSE:MILUX) shares have had a really impressive month, gaining 26% after a shaky period beforehand. But the gains over the last month weren't enough to make shareholders whole, as the share price is still down 7.7% in the last twelve months.

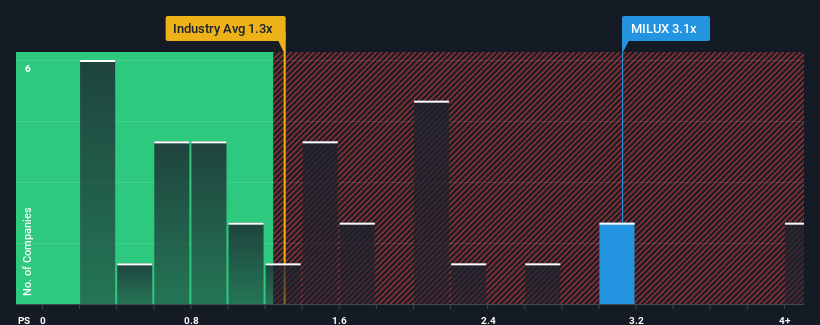

Since its price has surged higher, when almost half of the companies in Malaysia's Consumer Durables industry have price-to-sales ratios (or "P/S") below 1.3x, you may consider Milux Corporation Berhad as a stock probably not worth researching with its 3.1x P/S ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the elevated P/S.

See our latest analysis for Milux Corporation Berhad

What Does Milux Corporation Berhad's P/S Mean For Shareholders?

For example, consider that Milux Corporation Berhad's financial performance has been poor lately as its revenue has been in decline. One possibility is that the P/S is high because investors think the company will still do enough to outperform the broader industry in the near future. However, if this isn't the case, investors might get caught out paying too much for the stock.

We don't have analyst forecasts, but you can see how recent trends are setting up the company for the future by checking out our free report on Milux Corporation Berhad's earnings, revenue and cash flow.Is There Enough Revenue Growth Forecasted For Milux Corporation Berhad?

The only time you'd be truly comfortable seeing a P/S as high as Milux Corporation Berhad's is when the company's growth is on track to outshine the industry.

In reviewing the last year of financials, we were disheartened to see the company's revenues fell to the tune of 22%. This means it has also seen a slide in revenue over the longer-term as revenue is down 16% in total over the last three years. Therefore, it's fair to say the revenue growth recently has been undesirable for the company.

In contrast to the company, the rest of the industry is expected to grow by 9.7% over the next year, which really puts the company's recent medium-term revenue decline into perspective.

In light of this, it's alarming that Milux Corporation Berhad's P/S sits above the majority of other companies. It seems most investors are ignoring the recent poor growth rate and are hoping for a turnaround in the company's business prospects. There's a very good chance existing shareholders are setting themselves up for future disappointment if the P/S falls to levels more in line with the recent negative growth rates.

The Bottom Line On Milux Corporation Berhad's P/S

The large bounce in Milux Corporation Berhad's shares has lifted the company's P/S handsomely. While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

Our examination of Milux Corporation Berhad revealed its shrinking revenue over the medium-term isn't resulting in a P/S as low as we expected, given the industry is set to grow. When we see revenue heading backwards and underperforming the industry forecasts, we feel the possibility of the share price declining is very real, bringing the P/S back into the realm of reasonability. If recent medium-term revenue trends continue, it will place shareholders' investments at significant risk and potential investors in danger of paying an excessive premium.

Before you take the next step, you should know about the 4 warning signs for Milux Corporation Berhad that we have uncovered.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:MILUX

Milux Corporation Berhad

An investment holding company, manufactures, sales, trades, and deals in a range of gas cookers, electrical household appliances, and related products in Malaysia and the rest of Asia.

Flawless balance sheet very low.

Market Insights

Community Narratives