The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that Y&G Corporation Bhd. (KLSE:Y&G) does use debt in its business. But is this debt a concern to shareholders?

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we think about a company's use of debt, we first look at cash and debt together.

Check out our latest analysis for Y&G Corporation Bhd

What Is Y&G Corporation Bhd's Net Debt?

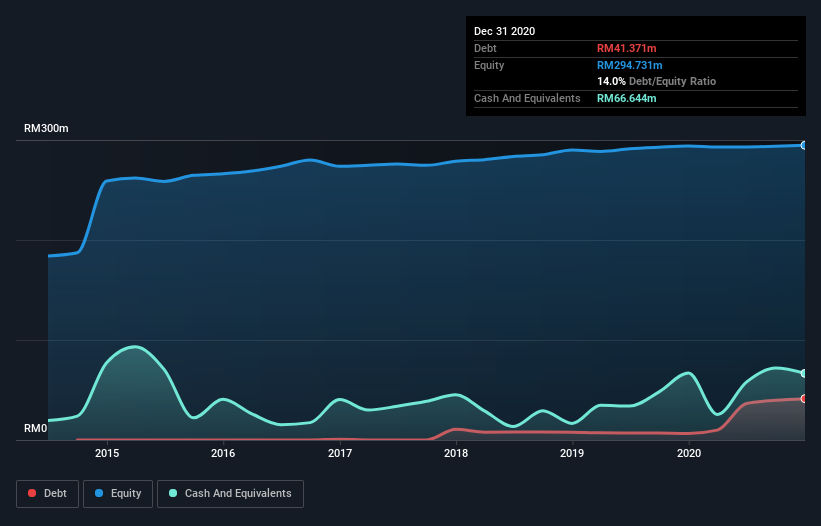

As you can see below, at the end of December 2020, Y&G Corporation Bhd had RM41.4m of debt, up from RM6.59m a year ago. Click the image for more detail. But it also has RM66.6m in cash to offset that, meaning it has RM25.3m net cash.

A Look At Y&G Corporation Bhd's Liabilities

Zooming in on the latest balance sheet data, we can see that Y&G Corporation Bhd had liabilities of RM48.7m due within 12 months and liabilities of RM43.6m due beyond that. On the other hand, it had cash of RM66.6m and RM37.0m worth of receivables due within a year. So it can boast RM11.3m more liquid assets than total liabilities.

This surplus suggests that Y&G Corporation Bhd has a conservative balance sheet, and could probably eliminate its debt without much difficulty. Simply put, the fact that Y&G Corporation Bhd has more cash than debt is arguably a good indication that it can manage its debt safely.

The modesty of its debt load may become crucial for Y&G Corporation Bhd if management cannot prevent a repeat of the 55% cut to EBIT over the last year. When it comes to paying off debt, falling earnings are no more useful than sugary sodas are for your health. There's no doubt that we learn most about debt from the balance sheet. But it is Y&G Corporation Bhd's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. While Y&G Corporation Bhd has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Happily for any shareholders, Y&G Corporation Bhd actually produced more free cash flow than EBIT over the last three years. There's nothing better than incoming cash when it comes to staying in your lenders' good graces.

Summing up

While it is always sensible to investigate a company's debt, in this case Y&G Corporation Bhd has RM25.3m in net cash and a decent-looking balance sheet. And it impressed us with free cash flow of -RM25m, being 231% of its EBIT. So we are not troubled with Y&G Corporation Bhd's debt use. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. We've identified 4 warning signs with Y&G Corporation Bhd (at least 2 which are a bit unpleasant) , and understanding them should be part of your investment process.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

If you're looking for stocks to buy, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KLSE:Y&G

Y&G Corporation Bhd

An investment holding company, provides property construction and management services in Malaysia.

Adequate balance sheet slight.

Market Insights

Community Narratives