Is UWC Berhad's (KLSE:UWC) Stock's Recent Performance Being Led By Its Attractive Financial Prospects?

UWC Berhad's (KLSE:UWC) stock is up by a considerable 22% over the past three months. Given that the market rewards strong financials in the long-term, we wonder if that is the case in this instance. In this article, we decided to focus on UWC Berhad's ROE.

ROE or return on equity is a useful tool to assess how effectively a company can generate returns on the investment it received from its shareholders. Put another way, it reveals the company's success at turning shareholder investments into profits.

See our latest analysis for UWC Berhad

How To Calculate Return On Equity?

The formula for ROE is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for UWC Berhad is:

26% = RM58m ÷ RM223m (Based on the trailing twelve months to July 2020).

The 'return' is the profit over the last twelve months. Another way to think of that is that for every MYR1 worth of equity, the company was able to earn MYR0.26 in profit.

What Has ROE Got To Do With Earnings Growth?

We have already established that ROE serves as an efficient profit-generating gauge for a company's future earnings. Based on how much of its profits the company chooses to reinvest or "retain", we are then able to evaluate a company's future ability to generate profits. Assuming everything else remains unchanged, the higher the ROE and profit retention, the higher the growth rate of a company compared to companies that don't necessarily bear these characteristics.

UWC Berhad's Earnings Growth And 26% ROE

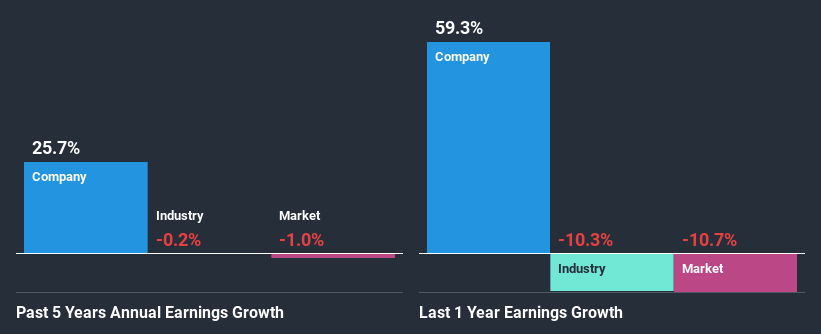

To begin with, UWC Berhad has a pretty high ROE which is interesting. Secondly, even when compared to the industry average of 8.4% the company's ROE is quite impressive. As a result, UWC Berhad's exceptional 26% net income growth seen over the past five years, doesn't come as a surprise.

Given that the industry shrunk its earnings at a rate of 0.2% in the same period, the net income growth of the company is quite impressive.

The basis for attaching value to a company is, to a great extent, tied to its earnings growth. The investor should try to establish if the expected growth or decline in earnings, whichever the case may be, is priced in. By doing so, they will have an idea if the stock is headed into clear blue waters or if swampy waters await. Is UWC Berhad fairly valued compared to other companies? These 3 valuation measures might help you decide.

Is UWC Berhad Using Its Retained Earnings Effectively?

UWC Berhad's three-year median payout ratio to shareholders is 25%, which is quite low. This implies that the company is retaining 75% of its profits. So it seems like the management is reinvesting profits heavily to grow its business and this reflects in its earnings growth number.

While UWC Berhad has been growing its earnings, it only recently started to pay dividends which likely means that the company decided to impress new and existing shareholders with a dividend. Our latest analyst data shows that the future payout ratio of the company is expected to drop to 19% over the next three years. The fact that the company's ROE is expected to rise to 37% over the same period is explained by the drop in the payout ratio.

Conclusion

Overall, we are quite pleased with UWC Berhad's performance. Specifically, we like that the company is reinvesting a huge chunk of its profits at a high rate of return. This of course has caused the company to see substantial growth in its earnings. That being so, the latest analyst forecasts show that the company will continue to see an expansion in its earnings. Are these analysts expectations based on the broad expectations for the industry, or on the company's fundamentals? Click here to be taken to our analyst's forecasts page for the company.

If you decide to trade UWC Berhad, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About KLSE:UWC

UWC Berhad

An investment holding company, engages in the provision of precision sheet metal fabrication, precision machined components, and value-added assembly services in Malaysia, the United States, Singapore, Thailand, India, France, the Netherlands, Australia, China, Canada, Denmark, Germany, Japan, Mexico, Spain, South Korea, and Vietnam.

Flawless balance sheet with high growth potential.