- Malaysia

- /

- Electrical

- /

- KLSE:SLVEST

We Wouldn't Rely On Solarvest Holdings Berhad's (KLSE:SLVEST) Statutory Earnings As A Guide

As a general rule, we think profitable companies are less risky than companies that lose money. That said, the current statutory profit is not always a good guide to a company's underlying profitability. Today we'll focus on whether this year's statutory profits are a good guide to understanding Solarvest Holdings Berhad (KLSE:SLVEST).

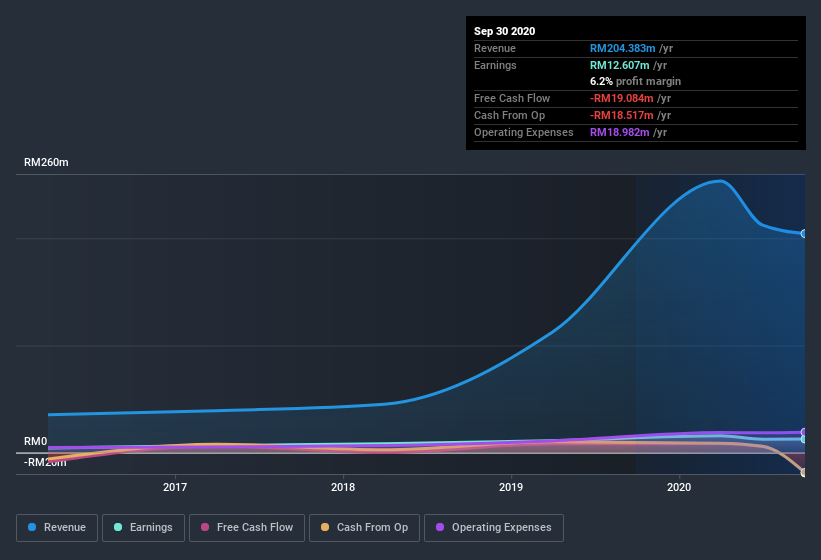

It's good to see that over the last twelve months Solarvest Holdings Berhad made a profit of RM12.6m on revenue of RM204.4m. Happily, it has grown both its profit and revenue over the last three years (though we note its profit is down over the last year).

See our latest analysis for Solarvest Holdings Berhad

Importantly, statutory profits are not always the best tool for understanding a company's true earnings power, so it's well worth examining profits in a little more detail. So this article aims to better understand Solarvest Holdings Berhad's underlying earnings power by taking a look at how dilution, and unusual items are impacting it, and considering how well those paper profits are being converted into cash flow. That might leave you wondering what analysts are forecasting in terms of future profitability. Luckily, you can click here to see an interactive graph depicting future profitability, based on their estimates.

Examining Cashflow Against Solarvest Holdings Berhad's Earnings

As finance nerds would already know, the accrual ratio from cashflow is a key measure for assessing how well a company's free cash flow (FCF) matches its profit. The accrual ratio subtracts the FCF from the profit for a given period, and divides the result by the average operating assets of the company over that time. You could think of the accrual ratio from cashflow as the 'non-FCF profit ratio'.

As a result, a negative accrual ratio is a positive for the company, and a positive accrual ratio is a negative. While having an accrual ratio above zero is of little concern, we do think it's worth noting when a company has a relatively high accrual ratio. Notably, there is some academic evidence that suggests that a high accrual ratio is a bad sign for near-term profits, generally speaking.

For the year to September 2020, Solarvest Holdings Berhad had an accrual ratio of 0.56. Statistically speaking, that's a real negative for future earnings. And indeed, during the period the company didn't produce any free cash flow whatsoever. In the last twelve months it actually had negative free cash flow, with an outflow of RM19m despite its profit of RM12.6m, mentioned above. It's worth noting that Solarvest Holdings Berhad generated positive FCF of RM8.4m a year ago, so at least they've done it in the past. Having said that, there is more to consider. We must also consider the impact of unusual items on statutory profit (and thus the accrual ratio), as well as note the ramifications of the company issuing new shares.

In order to understand the potential for per share returns, it is essential to consider how much a company is diluting shareholders. As it happens, Solarvest Holdings Berhad issued 8.2% more new shares over the last year. Therefore, each share now receives a smaller portion of profit. To celebrate net income while ignoring dilution is like rejoicing because you have a single slice of a larger pizza, but ignoring the fact that the pizza is now cut into many more slices. You can see a chart of Solarvest Holdings Berhad's EPS by clicking here.

A Look At The Impact Of Solarvest Holdings Berhad's Dilution on Its Earnings Per Share (EPS).

As you can see above, Solarvest Holdings Berhad has been growing its net income over the last few years, with an annualized gain of 71% over three years. In contrast, earnings per share were actually down by 99% per year, in the exact same period. Net income was down 6.0% over the last twelve months. But the EPS result was even worth, with the company recording a decline of 99%. So you can see that the dilution has had a bit of an impact on shareholders. Therefore, the dilution is having a noteworthy influence on shareholder returns. And so, you can see quite clearly that dilution is influencing shareholder earnings.

In the long term, if Solarvest Holdings Berhad's earnings per share can increase, then the share price should too. But on the other hand, we'd be far less excited to learn profit (but not EPS) was improving. For that reason, you could say that EPS is more important that net income in the long run, assuming the goal is to assess whether a company's share price might grow.

The Impact Of Unusual Items On Profit

Unfortunately (in the short term) Solarvest Holdings Berhad saw its profit reduced by unusual items worth RM1.7m. In the case where this was a non-cash charge it would have made it easier to have high cash conversion, so it's surprising that the accrual ratio tells a different story. It's never great to see unusual items costing the company profits, but on the upside, things might improve sooner rather than later. When we analysed the vast majority of listed companies worldwide, we found that significant unusual items are often not repeated. And that's hardly a surprise given these line items are considered unusual. If Solarvest Holdings Berhad doesn't see those unusual expenses repeat, then all else being equal we'd expect its profit to increase over the coming year.

Our Take On Solarvest Holdings Berhad's Profit Performance

In conclusion, Solarvest Holdings Berhad's accrual ratio suggests that its statutory earnings are not backed by cash flow; but the fact unusual items actually weighed on profit may create upside if those unusual items to not recur. On top of that, the dilution means that shareholders now own less of the company. For the reasons mentioned above, we think that a perfunctory glance at Solarvest Holdings Berhad's statutory profits might make it look better than it really is on an underlying level. In light of this, if you'd like to do more analysis on the company, it's vital to be informed of the risks involved. Our analysis shows 3 warning signs for Solarvest Holdings Berhad (1 can't be ignored!) and we strongly recommend you look at these before investing.

Our examination of Solarvest Holdings Berhad has focussed on certain factors that can make its earnings look better than they are. And, on that basis, we are somewhat skeptical. But there are plenty of other ways to inform your opinion of a company. Some people consider a high return on equity to be a good sign of a quality business. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying to be useful.

When trading Solarvest Holdings Berhad or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About KLSE:SLVEST

Solarvest Holdings Berhad

An investment holding company, provides engineering, procurement, construction, and commissioning solutions for solar photovoltaic systems to residential, commercial, and industrial properties in Malaysia, the Philippines, Taiwan, Vietnam, Singapore, Indonesia, and Thailand.

High growth potential with proven track record.

Similar Companies

Market Insights

Community Narratives