Advertisement

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that Mitrajaya Holdings Berhad (KLSE:MITRA) does use debt in its business. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

Check out our latest analysis for Mitrajaya Holdings Berhad

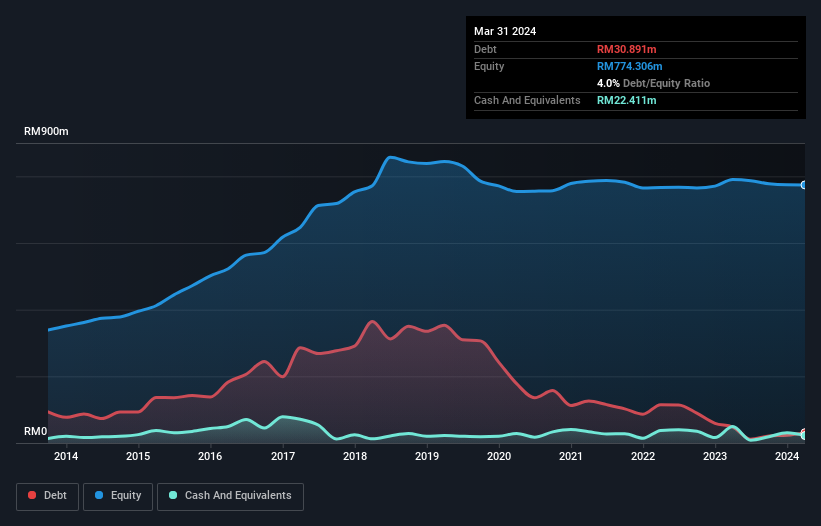

What Is Mitrajaya Holdings Berhad's Debt?

The image below, which you can click on for greater detail, shows that Mitrajaya Holdings Berhad had debt of RM30.9m at the end of March 2024, a reduction from RM47.9m over a year. On the flip side, it has RM22.4m in cash leading to net debt of about RM8.48m.

How Healthy Is Mitrajaya Holdings Berhad's Balance Sheet?

The latest balance sheet data shows that Mitrajaya Holdings Berhad had liabilities of RM156.1m due within a year, and liabilities of RM2.87m falling due after that. On the other hand, it had cash of RM22.4m and RM179.3m worth of receivables due within a year. So it actually has RM42.8m more liquid assets than total liabilities.

This excess liquidity suggests that Mitrajaya Holdings Berhad is taking a careful approach to debt. Given it has easily adequate short term liquidity, we don't think it will have any issues with its lenders. The balance sheet is clearly the area to focus on when you are analysing debt. But you can't view debt in total isolation; since Mitrajaya Holdings Berhad will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

In the last year Mitrajaya Holdings Berhad had a loss before interest and tax, and actually shrunk its revenue by 33%, to RM217m. That makes us nervous, to say the least.

Caveat Emptor

While Mitrajaya Holdings Berhad's falling revenue is about as heartwarming as a wet blanket, arguably its earnings before interest and tax (EBIT) loss is even less appealing. To be specific the EBIT loss came in at RM6.2m. Looking on the brighter side, the business has adequate liquid assets, which give it time to grow and develop before its debt becomes a near-term issue. Still, we'd be more encouraged to study the business in depth if it already had some free cash flow. So it seems too risky for our taste. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. Case in point: We've spotted 3 warning signs for Mitrajaya Holdings Berhad you should be aware of, and 1 of them is significant.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About KLSE:MITRA

Mitrajaya Holdings Berhad

An investment holding company, engages construction and property development businesses in Malaysia and South Africa.

Flawless balance sheet with acceptable track record.

Market Insights

Advertisement

Community Narratives

America Wants Homegrown Drones — Draganfly Is Ready to Deliver

Fair Value US$9.21|33.9% undervalued

JO

Community Contributor

Cheesecake Factory offers an enticing opportunity for long-term growth by leveraging new concepts

Fair Value US$73.83|26.5% undervalued

ZW

Community Contributor

Coca-Cola’s Intrinsic Value Set to Rise with Fed Rate Cut

Fair Value US$67.50|2.3% undervalued

AL

Community Contributor

Fully Permitted Gold Mine with 50 Baggers Potential

Fair Value CA$41.00|98.0% undervalued

RO

Community Contributor