Advertisement

- Malaysia

- /

- Construction

- /

- KLSE:KIMLUN

Improved Revenues Required Before Kimlun Corporation Berhad (KLSE:KIMLUN) Stock's 27% Jump Looks Justified

Despite an already strong run, Kimlun Corporation Berhad (KLSE:KIMLUN) shares have been powering on, with a gain of 27% in the last thirty days. Not all shareholders will be feeling jubilant, since the share price is still down a very disappointing 17% in the last twelve months.

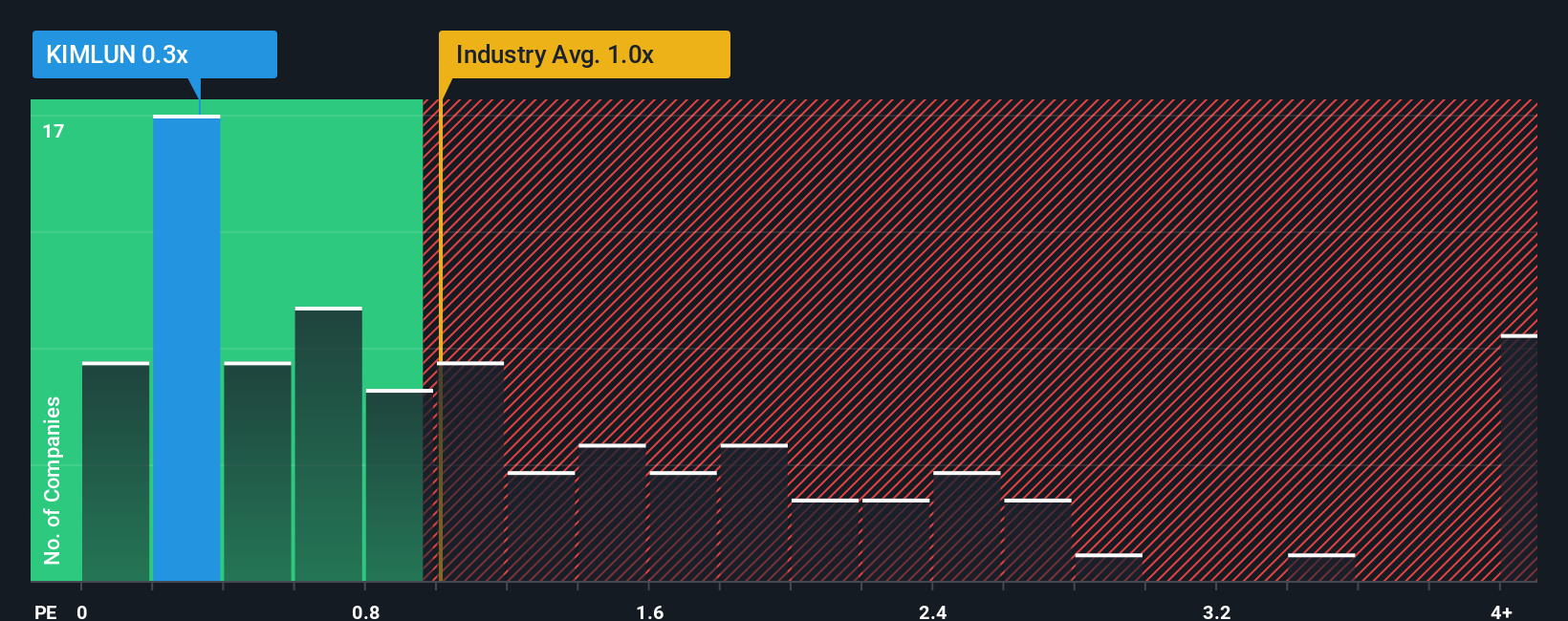

Even after such a large jump in price, given about half the companies operating in Malaysia's Construction industry have price-to-sales ratios (or "P/S") above 1x, you may still consider Kimlun Corporation Berhad as an attractive investment with its 0.3x P/S ratio. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's limited.

See our latest analysis for Kimlun Corporation Berhad

How Kimlun Corporation Berhad Has Been Performing

With revenue growth that's superior to most other companies of late, Kimlun Corporation Berhad has been doing relatively well. Perhaps the market is expecting future revenue performance to dive, which has kept the P/S suppressed. If the company manages to stay the course, then investors should be rewarded with a share price that matches its revenue figures.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Kimlun Corporation Berhad.Do Revenue Forecasts Match The Low P/S Ratio?

In order to justify its P/S ratio, Kimlun Corporation Berhad would need to produce sluggish growth that's trailing the industry.

Retrospectively, the last year delivered an exceptional 65% gain to the company's top line. Pleasingly, revenue has also lifted 123% in aggregate from three years ago, thanks to the last 12 months of growth. Accordingly, shareholders would have definitely welcomed those medium-term rates of revenue growth.

Looking ahead now, revenue is anticipated to climb by 0.9% during the coming year according to the dual analysts following the company. Meanwhile, the rest of the industry is forecast to expand by 24%, which is noticeably more attractive.

With this information, we can see why Kimlun Corporation Berhad is trading at a P/S lower than the industry. Apparently many shareholders weren't comfortable holding on while the company is potentially eyeing a less prosperous future.

The Bottom Line On Kimlun Corporation Berhad's P/S

The latest share price surge wasn't enough to lift Kimlun Corporation Berhad's P/S close to the industry median. Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've established that Kimlun Corporation Berhad maintains its low P/S on the weakness of its forecast growth being lower than the wider industry, as expected. At this stage investors feel the potential for an improvement in revenue isn't great enough to justify a higher P/S ratio. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

Before you settle on your opinion, we've discovered 1 warning sign for Kimlun Corporation Berhad that you should be aware of.

If these risks are making you reconsider your opinion on Kimlun Corporation Berhad, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're here to simplify it.

Discover if Kimlun Corporation Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:KIMLUN

Kimlun Corporation Berhad

An investment holding company, provides engineering and construction services in Malaysia and Singapore.

Solid track record and fair value.

Market Insights

Advertisement

Community Narratives

Pole position to benefit from GENIUS Act

Fair Value US$233.04|59.7% undervalued

CH

Community Contributor

IREN will transform from bitcoin miner to leader in AI infrastructure

Fair Value US$21.48|13.5% undervalued

KA

Community Contributor

Behind the Assay: XRF Scientific’s Role in Modern Mining Economics

Fair Value AU$2.10|1.4% undervalued

RO

Community Contributor