- Malaysia

- /

- Trade Distributors

- /

- KLSE:JSB

Revenues Not Telling The Story For Jentayu Sustainables Berhad (KLSE:JSB)

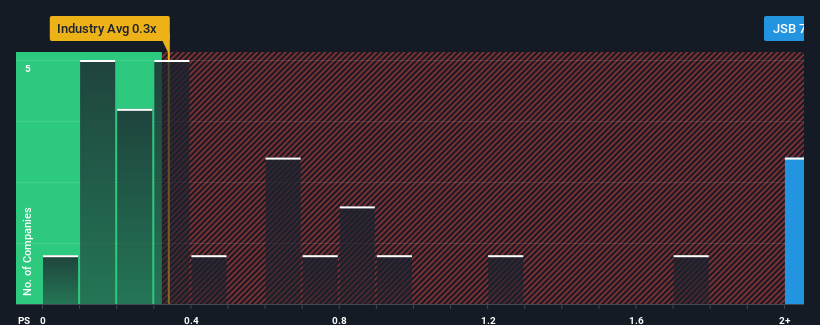

Jentayu Sustainables Berhad's (KLSE:JSB) price-to-sales (or "P/S") ratio of 7.8x may look like a poor investment opportunity when you consider close to half the companies in the Trade Distributors industry in Malaysia have P/S ratios below 0.3x. However, the P/S might be quite high for a reason and it requires further investigation to determine if it's justified.

See our latest analysis for Jentayu Sustainables Berhad

What Does Jentayu Sustainables Berhad's P/S Mean For Shareholders?

For example, consider that Jentayu Sustainables Berhad's financial performance has been poor lately as its revenue has been in decline. Perhaps the market believes the company can do enough to outperform the rest of the industry in the near future, which is keeping the P/S ratio high. If not, then existing shareholders may be quite nervous about the viability of the share price.

Want the full picture on earnings, revenue and cash flow for the company? Then our free report on Jentayu Sustainables Berhad will help you shine a light on its historical performance.Do Revenue Forecasts Match The High P/S Ratio?

The only time you'd be truly comfortable seeing a P/S as steep as Jentayu Sustainables Berhad's is when the company's growth is on track to outshine the industry decidedly.

In reviewing the last year of financials, we were disheartened to see the company's revenues fell to the tune of 32%. The last three years don't look nice either as the company has shrunk revenue by 56% in aggregate. Therefore, it's fair to say the revenue growth recently has been undesirable for the company.

This is in contrast to the rest of the industry, which is expected to decline by 0.4% over the next year, or less than the company's recent medium-term annualised revenue decline.

In light of this, it's odd that Jentayu Sustainables Berhad's P/S sits above the majority of other companies. In general, when revenue shrink rapidly the P/S premium often shrinks too, which could set up shareholders for future disappointment. There's potential for the P/S to fall to lower levels if the company doesn't improve its top-line growth, which would be difficult to do with the current industry outlook.

The Final Word

It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

We've established that Jentayu Sustainables Berhad currently trades on a much higher than expected P/S since its recent three-year revenues are even worse than the forecasts for a struggling industry. Right now we aren't comfortable with the high P/S as this revenue performance is unlikely to support such positive sentiment for long. We're also cautious about the company's ability to stay its recent medium-term course and resist even greater pain to its business from the broader industry turmoil. Unless the company's relative performance improves markedly, it's very challenging to accept these prices as being reasonable.

Plus, you should also learn about these 3 warning signs we've spotted with Jentayu Sustainables Berhad (including 1 which is significant).

It's important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:JSB

Jentayu Sustainables Berhad

An investment holding company, engages in trading and distribution of building materials, and other products in Malaysia.

Adequate balance sheet low.

Market Insights

Community Narratives