Advertisement

- Malaysia

- /

- Construction

- /

- KLSE:EDGENTA

UEM Edgenta Berhad (KLSE:EDGENTA) Stock's On A Decline: Are Poor Fundamentals The Cause?

With its stock down 19% over the past three months, it is easy to disregard UEM Edgenta Berhad (KLSE:EDGENTA). We decided to study the company's financials to determine if the downtrend will continue as the long-term performance of a company usually dictates market outcomes. Specifically, we decided to study UEM Edgenta Berhad's ROE in this article.

ROE or return on equity is a useful tool to assess how effectively a company can generate returns on the investment it received from its shareholders. In short, ROE shows the profit each dollar generates with respect to its shareholder investments.

View our latest analysis for UEM Edgenta Berhad

How Is ROE Calculated?

The formula for ROE is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for UEM Edgenta Berhad is:

4.6% = RM68m ÷ RM1.5b (Based on the trailing twelve months to September 2020).

The 'return' is the yearly profit. So, this means that for every MYR1 of its shareholder's investments, the company generates a profit of MYR0.05.

What Has ROE Got To Do With Earnings Growth?

Thus far, we have learned that ROE measures how efficiently a company is generating its profits. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Assuming everything else remains unchanged, the higher the ROE and profit retention, the higher the growth rate of a company compared to companies that don't necessarily bear these characteristics.

UEM Edgenta Berhad's Earnings Growth And 4.6% ROE

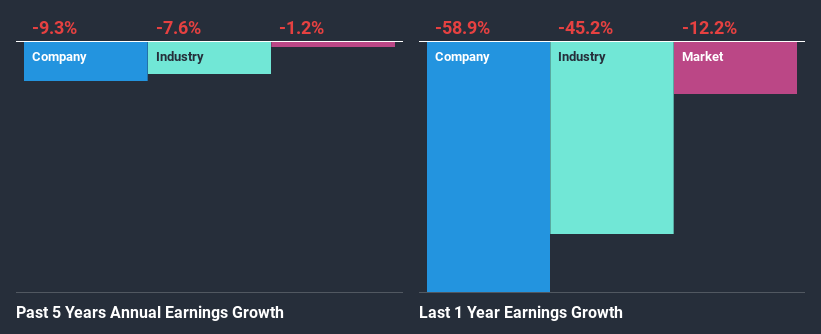

It is hard to argue that UEM Edgenta Berhad's ROE is much good in and of itself. An industry comparison shows that the company's ROE is not much different from the industry average of 4.7% either. Given the low ROE UEM Edgenta Berhad's five year net income decline of 9.3% is not surprising.

As a next step, we compared UEM Edgenta Berhad's performance with the industry and found thatUEM Edgenta Berhad's performance is depressing even when compared with the industry, which has shrunk its earnings at a rate of 7.6% in the same period, which is a slower than the company.

Earnings growth is a huge factor in stock valuation. What investors need to determine next is if the expected earnings growth, or the lack of it, is already built into the share price. By doing so, they will have an idea if the stock is headed into clear blue waters or if swampy waters await. Is EDGENTA fairly valued? This infographic on the company's intrinsic value has everything you need to know.

Is UEM Edgenta Berhad Making Efficient Use Of Its Profits?

UEM Edgenta Berhad's declining earnings is not surprising given how the company is spending most of its profits in paying dividends, judging by its three-year median payout ratio of 76% (or a retention ratio of 24%). With only a little being reinvested into the business, earnings growth would obviously be low or non-existent. To know the 3 risks we have identified for UEM Edgenta Berhad visit our risks dashboard for free.

In addition, UEM Edgenta Berhad has been paying dividends over a period of at least ten years suggesting that keeping up dividend payments is way more important to the management even if it comes at the cost of business growth. Based on the latest analysts' estimates, we found that the company's future payout ratio over the next three years is expected to hold steady at 73%. However, UEM Edgenta Berhad's ROE is predicted to rise to 6.9% despite there being no anticipated change in its payout ratio.

Conclusion

In total, we would have a hard think before deciding on any investment action concerning UEM Edgenta Berhad. As a result of its low ROE and lack of mich reinvestment into the business, the company has seen a disappointing earnings growth rate. That being so, the latest industry analyst forecasts show that the analysts are expecting to see a huge improvement in the company's earnings growth rate. Are these analysts expectations based on the broad expectations for the industry, or on the company's fundamentals? Click here to be taken to our analyst's forecasts page for the company.

If you’re looking to trade UEM Edgenta Berhad, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KLSE:EDGENTA

UEM Edgenta Berhad

An investment holding company, provides asset management and infrastructure solutions in Malaysia, the Middle East, Indonesia, Singapore, Taiwan, and India.

Flawless balance sheet with low risk.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|0.7% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|14.9% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.1% undervalued

TR

Community Contributor