Advertisement

- Malaysia

- /

- Construction

- /

- KLSE:BPURI

Bina Puri Holdings Bhd (KLSE:BPURI) Has Debt But No Earnings; Should You Worry?

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We note that Bina Puri Holdings Bhd (KLSE:BPURI) does have debt on its balance sheet. But the more important question is: how much risk is that debt creating?

What Risk Does Debt Bring?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we think about a company's use of debt, we first look at cash and debt together.

See our latest analysis for Bina Puri Holdings Bhd

How Much Debt Does Bina Puri Holdings Bhd Carry?

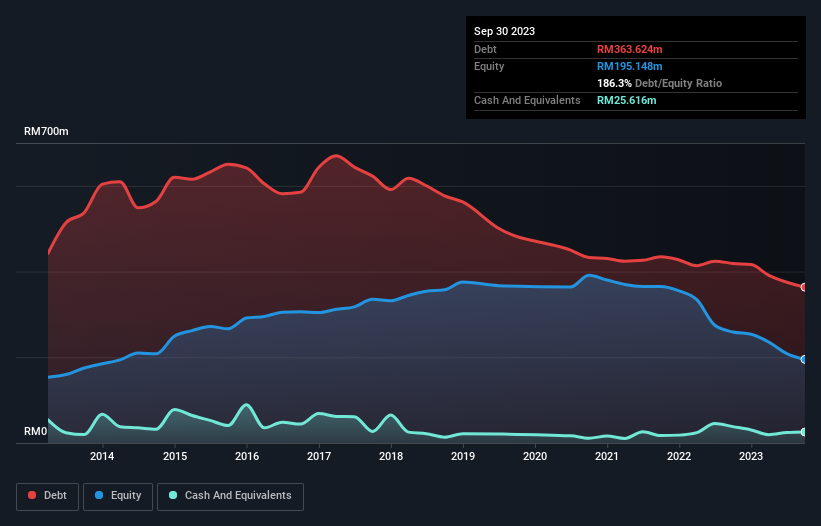

As you can see below, Bina Puri Holdings Bhd had RM363.6m of debt at September 2023, down from RM419.0m a year prior. However, it does have RM25.6m in cash offsetting this, leading to net debt of about RM338.0m.

How Healthy Is Bina Puri Holdings Bhd's Balance Sheet?

The latest balance sheet data shows that Bina Puri Holdings Bhd had liabilities of RM485.9m due within a year, and liabilities of RM293.8m falling due after that. Offsetting this, it had RM25.6m in cash and RM372.5m in receivables that were due within 12 months. So it has liabilities totalling RM381.6m more than its cash and near-term receivables, combined.

This deficit casts a shadow over the RM253.0m company, like a colossus towering over mere mortals. So we definitely think shareholders need to watch this one closely. After all, Bina Puri Holdings Bhd would likely require a major re-capitalisation if it had to pay its creditors today. There's no doubt that we learn most about debt from the balance sheet. But it is Bina Puri Holdings Bhd's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

In the last year Bina Puri Holdings Bhd had a loss before interest and tax, and actually shrunk its revenue by 55%, to RM101m. That makes us nervous, to say the least.

Caveat Emptor

Not only did Bina Puri Holdings Bhd's revenue slip over the last twelve months, but it also produced negative earnings before interest and tax (EBIT). Indeed, it lost a very considerable RM91m at the EBIT level. Considering that alongside the liabilities mentioned above make us nervous about the company. It would need to improve its operations quickly for us to be interested in it. Not least because it burned through RM18m in negative free cash flow over the last year. So suffice it to say we consider the stock to be risky. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. We've identified 5 warning signs with Bina Puri Holdings Bhd (at least 4 which can't be ignored) , and understanding them should be part of your investment process.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

Valuation is complex, but we're here to simplify it.

Discover if Bina Puri Holdings Bhd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:BPURI

Bina Puri Holdings Bhd

An investment holding company, engages in the construction and property development businesses in Malaysia and other Asian countries.

Moderate with questionable track record.

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|24.5% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|45.3% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|33.9% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|56.1% undervalued

AX

Community Contributor