David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, Ahmad Zaki Resources Berhad (KLSE:AZRB) does carry debt. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we examine debt levels, we first consider both cash and debt levels, together.

See our latest analysis for Ahmad Zaki Resources Berhad

What Is Ahmad Zaki Resources Berhad's Net Debt?

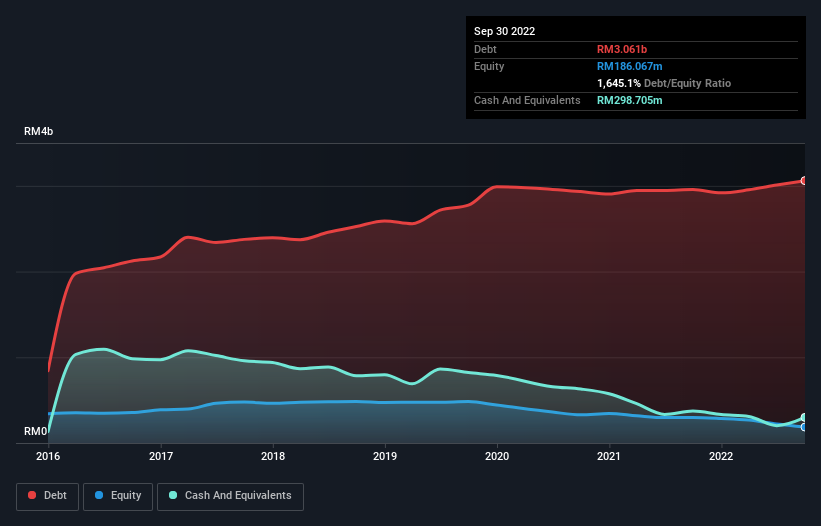

As you can see below, Ahmad Zaki Resources Berhad had RM3.06b of debt, at September 2022, which is about the same as the year before. You can click the chart for greater detail. On the flip side, it has RM298.7m in cash leading to net debt of about RM2.76b.

A Look At Ahmad Zaki Resources Berhad's Liabilities

According to the last reported balance sheet, Ahmad Zaki Resources Berhad had liabilities of RM1.39b due within 12 months, and liabilities of RM2.93b due beyond 12 months. On the other hand, it had cash of RM298.7m and RM461.6m worth of receivables due within a year. So it has liabilities totalling RM3.56b more than its cash and near-term receivables, combined.

This deficit casts a shadow over the RM95.4m company, like a colossus towering over mere mortals. So we definitely think shareholders need to watch this one closely. At the end of the day, Ahmad Zaki Resources Berhad would probably need a major re-capitalization if its creditors were to demand repayment. The balance sheet is clearly the area to focus on when you are analysing debt. But you can't view debt in total isolation; since Ahmad Zaki Resources Berhad will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Over 12 months, Ahmad Zaki Resources Berhad made a loss at the EBIT level, and saw its revenue drop to RM595m, which is a fall of 31%. That makes us nervous, to say the least.

Caveat Emptor

While Ahmad Zaki Resources Berhad's falling revenue is about as heartwarming as a wet blanket, arguably its earnings before interest and tax (EBIT) loss is even less appealing. Indeed, it lost a very considerable RM93m at the EBIT level. When you combine this with the very significant balance sheet liabilities mentioned above, we are so wary of it that we are basically at a loss for the right words. Sure, the company might have a nice story about how they are going on to a brighter future. But the reality is that it is low on liquid assets relative to liabilities, and it lost RM97m in the last year. So we're not very excited about owning this stock. Its too risky for us. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. Be aware that Ahmad Zaki Resources Berhad is showing 2 warning signs in our investment analysis , and 1 of those is concerning...

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:AZRB

Ahmad Zaki Resources Berhad

Ahmad Zaki Resources Berhad, and investment holding company, provides management services and acts as a contractor of civil and structural works in Malaysia, Indonesia, India, and the Kingdom of Saudi Arabia.

Fair value with low risk.

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

A case for USD $14.81 per share based on book value. Be warned, this is a micro-cap dependent on a single mine.

Occidental Petroleum to Become Fairly Priced at $68.29 According to Future Projections

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)