Advertisement

Bank Islam Malaysia Berhad (KLSE:BIMB) Is Reducing Its Dividend To MYR0.0412

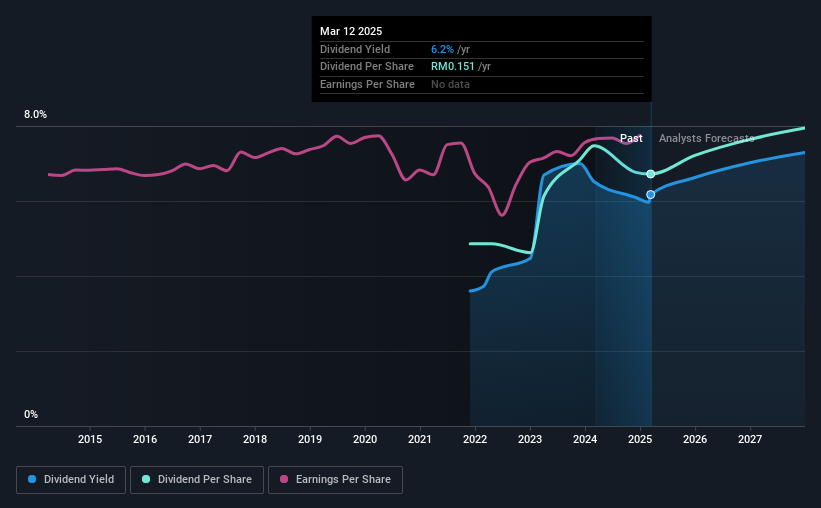

The board of Bank Islam Malaysia Berhad (KLSE:BIMB) has announced it will be reducing its dividend by 2.4% from last year's payment of MYR0.0422 on the 28th of March, with shareholders receiving MYR0.0412. However, the dividend yield of 6.2% is still a decent boost to shareholder returns.

Check out our latest analysis for Bank Islam Malaysia Berhad

Bank Islam Malaysia Berhad's Dividend Forecasted To Be Well Covered By Earnings

While it is great to have a strong dividend yield, we should also consider whether the payment is sustainable.

Having paid out dividends for only 3 years, Bank Islam Malaysia Berhad does not have much of a history being a dividend paying company. Based on Bank Islam Malaysia Berhad's last earnings report, calculating for its payout ratio equates to 60%, which means that the company covered its last dividend with comfortable room to spare.

Looking forward, EPS is forecast to rise by 18.6% over the next 3 years. Analysts forecast the future payout ratio could be 60% over the same time horizon, which is a number we think the company can maintain.

Bank Islam Malaysia Berhad Doesn't Have A Long Payment History

The dividend has been pretty stable looking back, but the company hasn't been paying one for very long. This makes it tough to judge how it would fare through a full economic cycle. The annual payment during the last 3 years was MYR0.109 in 2022, and the most recent fiscal year payment was MYR0.151. This works out to be a compound annual growth rate (CAGR) of approximately 11% a year over that time. We're not overly excited about the relatively short history of dividend payments, however the dividend is growing at a nice rate and we might take a closer look.

Bank Islam Malaysia Berhad May Find It Hard To Grow The Dividend

Investors who have held shares in the company for the past few years will be happy with the dividend income they have received. Unfortunately, Bank Islam Malaysia Berhad's earnings per share has been essentially flat over the past five years, which means the dividend may not be increased each year. Growth of 0.2% per annum is not particularly high, which might explain why the company is paying out a higher proportion of earnings. While this isn't necessarily a negative, it definitely signals that dividend growth could be constrained in the future unless earnings start to pick up again.

Our Thoughts On Bank Islam Malaysia Berhad's Dividend

Overall, while it's not great to see that the dividend has been cut, we think the company is now in a good position to make consistent payments going into the future. While the payout ratios are a good sign, we are less enthusiastic about the company's dividend record. The dividend looks okay, but there have been some issues in the past, so we would be a little bit cautious.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. Earnings growth generally bodes well for the future value of company dividend payments. See if the 9 Bank Islam Malaysia Berhad analysts we track are forecasting continued growth with our free report on analyst estimates for the company. Is Bank Islam Malaysia Berhad not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if Bank Islam Malaysia Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:BIMB

Bank Islam Malaysia Berhad

Provides Islamic banking products and services in Malaysia.

Excellent balance sheet average dividend payer.

Market Insights

Advertisement

Community Narratives

Enterprise, AI & Cloud Growth Ahead, Waiting For the Right Price 💸

Fair Value US$204.74|10.6% overvalued

FR

Community Contributor

Good foundation, but now it's all about the next steps

Fair Value US$147.87|26.4% undervalued

TO

Community Contributor

XTB's Path to 100–120 PLN by 2028 Amid Market Volatility

Fair Value zł100.96|35.4% undervalued

DZ

Community Contributor