Advertisement

- Mexico

- /

- Food and Staples Retail

- /

- BMV:WALMEX *

Some Confidence Is Lacking In Wal-Mart de México, S.A.B. de C.V.'s (BMV:WALMEX) P/E

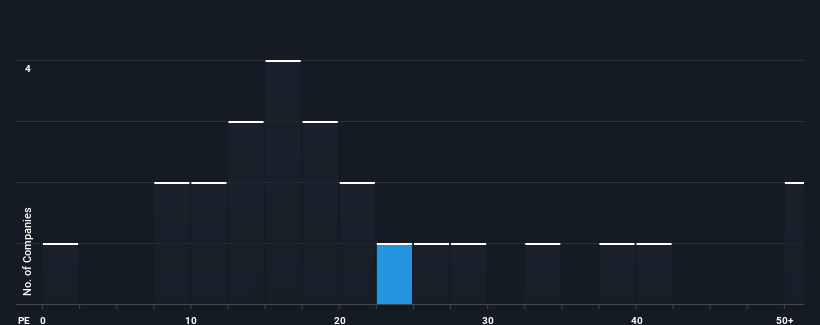

Wal-Mart de México, S.A.B. de C.V.'s (BMV:WALMEX) price-to-earnings (or "P/E") ratio of 22.5x might make it look like a strong sell right now compared to the market in Mexico, where around half of the companies have P/E ratios below 13x and even P/E's below 8x are quite common. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/E.

Wal-Mart de México. de could be doing better as it's been growing earnings less than most other companies lately. One possibility is that the P/E is high because investors think this lacklustre earnings performance will improve markedly. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Check out our latest analysis for Wal-Mart de México. de

How Is Wal-Mart de México. de's Growth Trending?

In order to justify its P/E ratio, Wal-Mart de México. de would need to produce outstanding growth well in excess of the market.

Retrospectively, the last year delivered a decent 5.5% gain to the company's bottom line. Pleasingly, EPS has also lifted 54% in aggregate from three years ago, partly thanks to the last 12 months of growth. So we can start by confirming that the company has done a great job of growing earnings over that time.

Looking ahead now, EPS is anticipated to climb by 9.6% each year during the coming three years according to the twelve analysts following the company. With the market predicted to deliver 9.7% growth each year, the company is positioned for a comparable earnings result.

In light of this, it's curious that Wal-Mart de México. de's P/E sits above the majority of other companies. Apparently many investors in the company are more bullish than analysts indicate and aren't willing to let go of their stock right now. Although, additional gains will be difficult to achieve as this level of earnings growth is likely to weigh down the share price eventually.

The Final Word

Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

We've established that Wal-Mart de México. de currently trades on a higher than expected P/E since its forecast growth is only in line with the wider market. When we see an average earnings outlook with market-like growth, we suspect the share price is at risk of declining, sending the high P/E lower. This places shareholders' investments at risk and potential investors in danger of paying an unnecessary premium.

Having said that, be aware Wal-Mart de México. de is showing 1 warning sign in our investment analysis, you should know about.

If you're unsure about the strength of Wal-Mart de México. de's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're here to simplify it.

Discover if Wal-Mart de México. de might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BMV:WALMEX *

Wal-Mart de México. de

Owns and operates self-service stores in Mexico and Central America.

Excellent balance sheet with acceptable track record.

Market Insights

Advertisement

Community Narratives

Kodiak AI - a potential 100 bagger opportunity?

Fair Value US$14.00|44.7% undervalued

DA

Community Contributor

A Fair Price for a Great Business Facing Real Threats

Fair Value US$383.06|13.0% undervalued

IM

Community Contributor

AXON And Shopify Integration Will Unlock Global Mobile Advertising

Fair Value US$646.30|0% overvalued

AN

Based on Analyst Price Targets