- South Korea

- /

- Electronic Equipment and Components

- /

- KOSE:A007660

High Growth Tech Stocks To Watch In South Korea September 2024

Reviewed by Simply Wall St

In the last week, the South Korean market has stayed flat, and over the past year, it has experienced a 3.1% drop; however, earnings are forecast to grow by 29% annually. In this context, identifying high-growth tech stocks that can capitalize on future earnings growth becomes crucial for investors looking to navigate these market conditions effectively.

Top 10 High Growth Tech Companies In South Korea

| Name | Revenue Growth | Earnings Growth | Growth Rating |

|---|---|---|---|

| Seojin SystemLtd | 33.61% | 52.05% | ★★★★★★ |

| IMLtd | 21.80% | 111.43% | ★★★★★★ |

| Bioneer | 23.53% | 97.58% | ★★★★★★ |

| FLITTO | 32.60% | 106.82% | ★★★★★★ |

| NEXON Games | 29.64% | 66.98% | ★★★★★★ |

| Park Systems | 23.64% | 35.66% | ★★★★★★ |

| ALTEOGEN | 64.22% | 99.46% | ★★★★★★ |

| Devsisters | 29.08% | 63.02% | ★★★★★★ |

| AmosenseLtd | 24.04% | 71.97% | ★★★★★★ |

| UTI | 114.97% | 134.59% | ★★★★★★ |

Click here to see the full list of 49 stocks from our KRX High Growth Tech and AI Stocks screener.

Let's review some notable picks from our screened stocks.

ALTEOGEN (KOSDAQ:A196170)

Simply Wall St Growth Rating: ★★★★★★

Overview: ALTEOGEN Inc., a bio company, focuses on developing long-acting biobetters, proprietary antibody-drug conjugates, and antibody biosimilars with a market cap of ₩16.79 billion.

Operations: ALTEOGEN derives its revenue primarily from the biotechnology segment, amounting to ₩90.79 billion. The company specializes in developing innovative biopharmaceutical products such as long-acting biobetters and proprietary antibody-drug conjugates.

Alteogen's recent MFDS approval for Tergase® highlights its innovative Hybrozyme™ Technology, offering over 99% purity compared to traditional bovine or ovine-derived hyaluronidases. This approval marks a significant milestone, transitioning Alteogen into a commercial-stage company with potential applications in eye surgery and orthopedics pain management. With forecasted revenue growth of 64.2% annually and expected earnings growth at 99.46%, the company is positioned for substantial expansion within the biotech sector in South Korea.

- Dive into the specifics of ALTEOGEN here with our thorough health report.

Assess ALTEOGEN's past performance with our detailed historical performance reports.

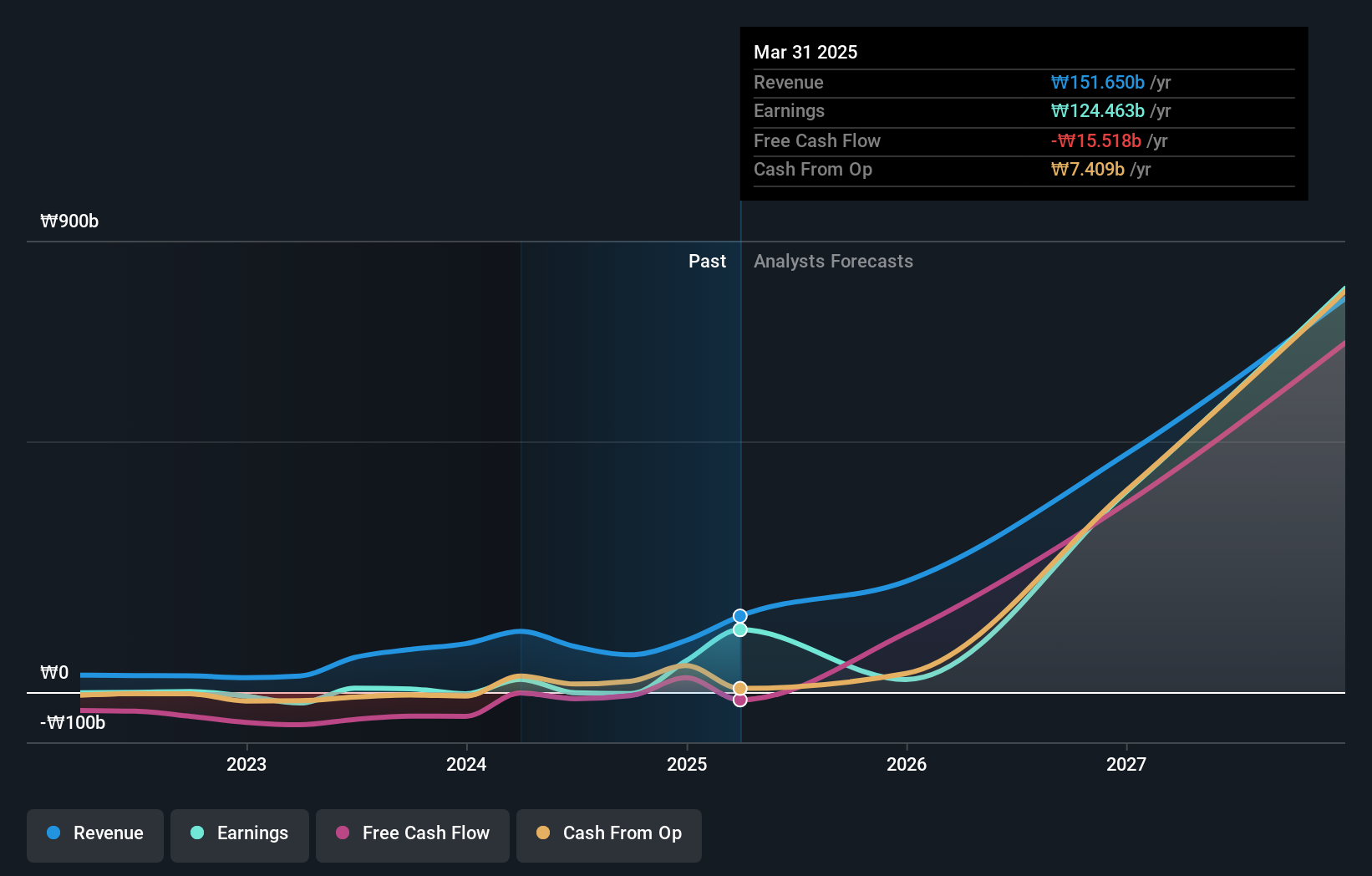

ISU Petasys (KOSE:A007660)

Simply Wall St Growth Rating: ★★★★★☆

Overview: ISU Petasys Co., Ltd. manufactures and sells printed circuit boards (PCBs) worldwide, with a market cap of ₩2.32 trillion.

Operations: ISU Petasys generates revenue primarily from the manufacture and sale of printed circuit boards (PCBs), amounting to ₩743.88 billion. The company operates on a global scale, serving various markets with its PCB products.

ISU Petasys, a prominent player in the tech sector, has shown promising growth prospects with an expected annual profit growth rate of 44.5%. Despite a recent 7.3% decline in profit margins to 7.5%, the company is forecasted to achieve significant earnings expansion over the next three years. Notably, ISU Petasys' revenue is projected to grow at 19% annually, outpacing the South Korean market's average of 10.4%. The company's strategic investments in R&D have been substantial; for instance, R&D expenses accounted for ₩60 billion last year, underscoring its commitment to innovation and technological advancement.

- Click here to discover the nuances of ISU Petasys with our detailed analytical health report.

Gain insights into ISU Petasys' historical performance by reviewing our past performance report.

Celltrion (KOSE:A068270)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Celltrion, Inc., along with its subsidiaries, develops and produces protein-based drugs for oncology treatment in South Korea and has a market cap of ₩39.35 trillion.

Operations: Celltrion, Inc. generates revenue primarily from its Bio Medical Supply segment (₩3.54 trillion) and Chemical Drugs segment (₩507.02 billion). The company focuses on developing and producing protein-based oncology drugs in South Korea.

Celltrion's revenue is projected to grow at 25.4% annually, significantly outpacing the South Korean market's average of 10.4%. The company's earnings are expected to surge by 59.4% per year, despite a recent drop in net profit margins from 23.8% to 12.1%. Celltrion has invested heavily in R&D, with expenses reaching ₩60 billion last year, highlighting its commitment to innovation and technological advancement. Recent agreements with Cigna Healthcare and Express Scripts for ZYMFENTRA® could further bolster its market position and drive future growth prospects.

Summing It All Up

- Unlock our comprehensive list of 49 KRX High Growth Tech and AI Stocks by clicking here.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About KOSE:A007660

ISU Petasys

Manufactures and sells printed circuit boards (PCBs) worldwide.

High growth potential with excellent balance sheet.