Advertisement

- South Korea

- /

- IT

- /

- KOSDAQ:A242040

Namu Tech Co.,Ltd.'s (KOSDAQ:242040) Price Is Out Of Tune With Revenues

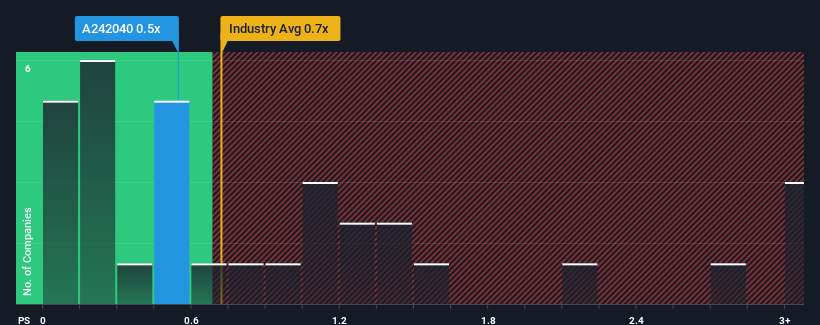

With a median price-to-sales (or "P/S") ratio of close to 0.7x in the IT industry in Korea, you could be forgiven for feeling indifferent about Namu Tech Co.,Ltd.'s (KOSDAQ:242040) P/S ratio of 0.5x. Although, it's not wise to simply ignore the P/S without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

View our latest analysis for Namu TechLtd

How Has Namu TechLtd Performed Recently?

For example, consider that Namu TechLtd's financial performance has been poor lately as its revenue has been in decline. Perhaps investors believe the recent revenue performance is enough to keep in line with the industry, which is keeping the P/S from dropping off. If you like the company, you'd at least be hoping this is the case so that you could potentially pick up some stock while it's not quite in favour.

We don't have analyst forecasts, but you can see how recent trends are setting up the company for the future by checking out our free report on Namu TechLtd's earnings, revenue and cash flow.Do Revenue Forecasts Match The P/S Ratio?

The only time you'd be comfortable seeing a P/S like Namu TechLtd's is when the company's growth is tracking the industry closely.

Retrospectively, the last year delivered a frustrating 6.7% decrease to the company's top line. The last three years don't look nice either as the company has shrunk revenue by 5.2% in aggregate. Therefore, it's fair to say the revenue growth recently has been undesirable for the company.

Comparing that to the industry, which is predicted to deliver 5.0% growth in the next 12 months, the company's downward momentum based on recent medium-term revenue results is a sobering picture.

With this in mind, we find it worrying that Namu TechLtd's P/S exceeds that of its industry peers. Apparently many investors in the company are way less bearish than recent times would indicate and aren't willing to let go of their stock right now. Only the boldest would assume these prices are sustainable as a continuation of recent revenue trends is likely to weigh on the share price eventually.

What We Can Learn From Namu TechLtd's P/S?

Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

Our look at Namu TechLtd revealed its shrinking revenues over the medium-term haven't impacted the P/S as much as we anticipated, given the industry is set to grow. When we see revenue heading backwards in the context of growing industry forecasts, it'd make sense to expect a possible share price decline on the horizon, sending the moderate P/S lower. Unless the the circumstances surrounding the recent medium-term improve, it wouldn't be wrong to expect a a difficult period ahead for the company's shareholders.

You should always think about risks. Case in point, we've spotted 2 warning signs for Namu TechLtd you should be aware of, and 1 of them doesn't sit too well with us.

It's important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

Valuation is complex, but we're here to simplify it.

Discover if Namu TechLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSDAQ:A242040

Namu TechLtd

Engages in the provision of consulting, construction, and maintenance services for IT infrastructure and cloud computing environment in high-tech, manufacturing, telecommunications, finance, public sector, and service industries.

Excellent balance sheet and slightly overvalued.

Market Insights

Advertisement

Community Narratives

America Wants Homegrown Drones — Draganfly Is Ready to Deliver

Fair Value US$9.21|32.6% undervalued

JO

Community Contributor

Cheesecake Factory offers an enticing opportunity for long-term growth by leveraging new concepts

Fair Value US$73.83|25.6% undervalued

ZW

Community Contributor

Coca-Cola’s Intrinsic Value Set to Rise with Fed Rate Cut

Fair Value US$67.50|1.6% undervalued

AL

Community Contributor

Fully Permitted Gold Mine with 50 Baggers Potential

Fair Value CA$41.00|98.2% undervalued

RO

Community Contributor