As global markets navigate a complex landscape marked by interest rate adjustments and sector-specific fluctuations, the U.S. indices have shown resilience with notable performances from small-cap stocks and technology-driven sectors. In this environment, growth companies with high insider ownership stand out as they often benefit from strong internal alignment and commitment to long-term success, making them compelling considerations for investors seeking influence-driven growth potential.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| Lavvi Empreendimentos Imobiliários (BOVESPA:LAVV3) | 11.9% | 21.1% |

| Archean Chemical Industries (NSEI:ACI) | 22.9% | 34% |

| Kirloskar Pneumatic (BSE:505283) | 30.3% | 30.1% |

| People & Technology (KOSDAQ:A137400) | 16.4% | 35.6% |

| Arctech Solar Holding (SHSE:688408) | 37.8% | 29.8% |

| Laopu Gold (SEHK:6181) | 36.4% | 33.2% |

| Medley (TSE:4480) | 34% | 30.4% |

| Seojin SystemLtd (KOSDAQ:A178320) | 30.7% | 49.1% |

| HANA Micron (KOSDAQ:A067310) | 18.3% | 105.8% |

| UTI (KOSDAQ:A179900) | 33.1% | 134.6% |

Underneath we present a selection of stocks filtered out by our screen.

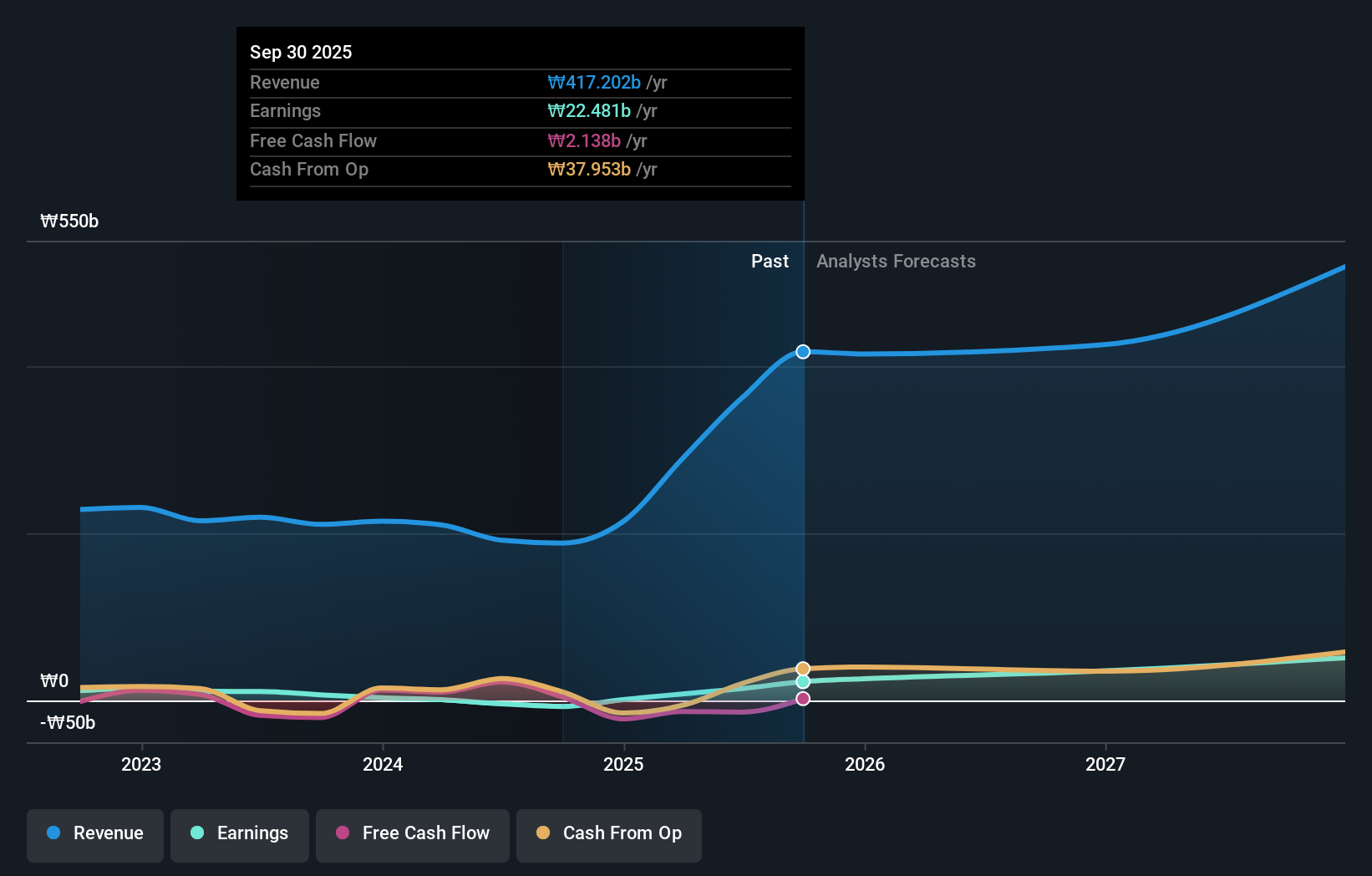

D.I (KOSE:A003160)

Simply Wall St Growth Rating: ★★★★★★

Overview: D.I Corporation manufactures and supplies semiconductor inspection equipment in South Korea and internationally, with a market cap of approximately ₩459.98 billion.

Operations: The company's revenue segments include Semiconductor Equipment at ₩137.77 billion, Audio and Video Equipment at ₩14.35 billion, Secondary Battery Equipment at ₩29.55 billion, Electronic Components Division at ₩12.90 billion, and Environmental Facilities Sector at ₩6.85 billion.

Insider Ownership: 31.8%

D.I. is poised for significant growth with earnings projected to increase by over 100% annually. Despite recent share price volatility, the company's revenue is expected to grow at a robust 47.5% per year, outpacing the broader Korean market's growth rate of 10.3%. With no substantial insider trading activity reported in the past three months, D.I.'s return on equity is forecasted to reach a high of 29.6% within three years, indicating strong potential profitability ahead.

- Navigate through the intricacies of D.I with our comprehensive analyst estimates report here.

- Our comprehensive valuation report raises the possibility that D.I is priced higher than what may be justified by its financials.

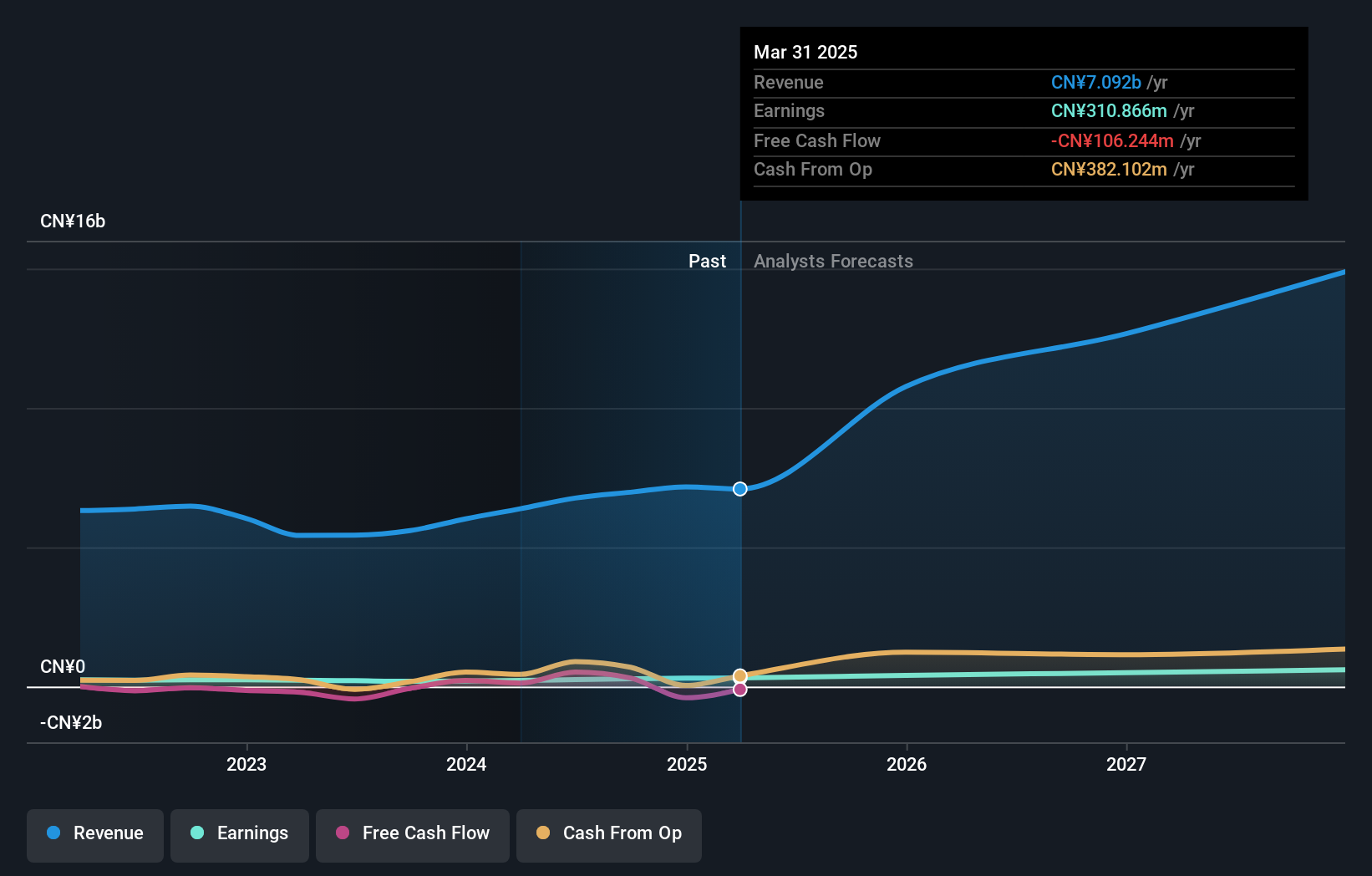

Hangzhou Juheshun New MaterialLTD (SHSE:605166)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Hangzhou Juheshun New Material Co., LTD specializes in the research, development, manufacture, and sale of nylon 6 chips and has a market cap of CN¥3.35 billion.

Operations: The company's revenue primarily comes from the production and sale of nylon chips, amounting to CN¥6.76 billion.

Insider Ownership: 24.5%

Hangzhou Juheshun New Material is set for substantial growth, with earnings forecasted to increase by 27.2% annually, outpacing the Chinese market's 23.8%. Revenue is projected to grow at 22.4% per year, surpassing market expectations of 13.4%. Recent half-year results show a significant rise in net income to CNY 152.79 million from CNY 100.25 million last year, indicating strong operational performance despite an unstable dividend history and low future return on equity forecasts.

- Take a closer look at Hangzhou Juheshun New MaterialLTD's potential here in our earnings growth report.

- Insights from our recent valuation report point to the potential undervaluation of Hangzhou Juheshun New MaterialLTD shares in the market.

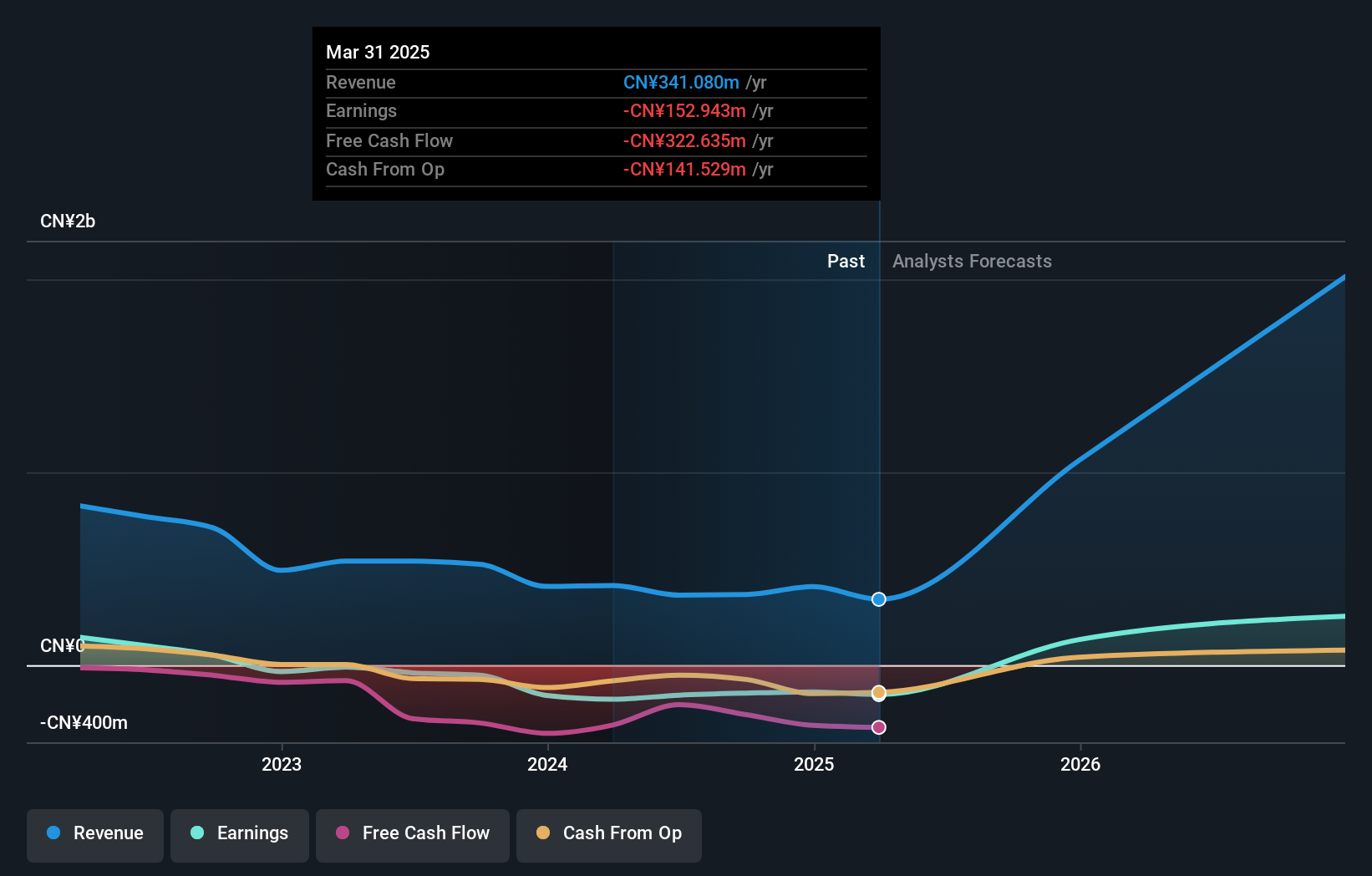

Jilin University Zhengyuan Information Technologies (SZSE:003029)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Jilin University Zhengyuan Information Technologies Co., Ltd. operates in the information technology sector, focusing on software development and IT services, with a market cap of CN¥4.04 billion.

Operations: The company generates revenue primarily from the Information Security Industry, amounting to CN¥362.90 million.

Insider Ownership: 12.6%

Jilin University Zhengyuan Information Technologies is poised for significant growth, with revenue expected to rise 46.7% annually, surpassing the Chinese market's average. Despite a volatile share price and recent shareholder dilution, the company is forecasted to become profitable within three years, outpacing market growth expectations. Recent half-year results showed a slight reduction in net loss to CNY 31.19 million from CNY 32.15 million last year, indicating gradual financial improvement amidst no recent insider trading activity.

- Click here to discover the nuances of Jilin University Zhengyuan Information Technologies with our detailed analytical future growth report.

- The analysis detailed in our Jilin University Zhengyuan Information Technologies valuation report hints at an inflated share price compared to its estimated value.

Seize The Opportunity

- Unlock more gems! Our Fast Growing Companies With High Insider Ownership screener has unearthed 1486 more companies for you to explore.Click here to unveil our expertly curated list of 1489 Fast Growing Companies With High Insider Ownership.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:003029

Jilin University Zhengyuan Information Technologies

Jilin University Zhengyuan Information Technologies Co., Ltd.

Flawless balance sheet with high growth potential.