- South Korea

- /

- Pharma

- /

- KOSE:A249420

Revenues Not Telling The Story For Ildong Pharmaceutical Co., Ltd. (KRX:249420) After Shares Rise 33%

Ildong Pharmaceutical Co., Ltd. (KRX:249420) shareholders would be excited to see that the share price has had a great month, posting a 33% gain and recovering from prior weakness. Taking a wider view, although not as strong as the last month, the full year gain of 11% is also fairly reasonable.

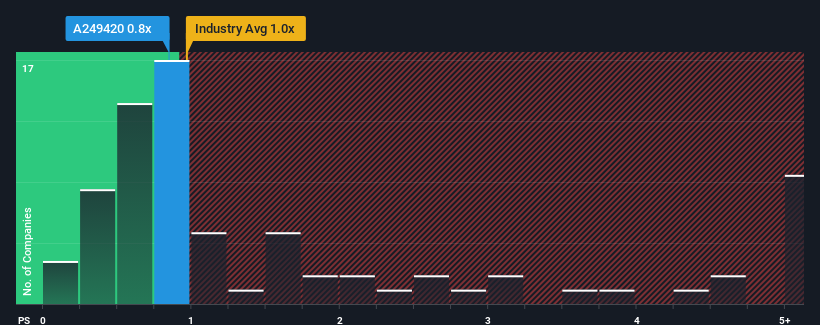

Even after such a large jump in price, it's still not a stretch to say that Ildong Pharmaceutical's price-to-sales (or "P/S") ratio of 0.8x right now seems quite "middle-of-the-road" compared to the Pharmaceuticals industry in Korea, where the median P/S ratio is around 1x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/S.

Check out our latest analysis for Ildong Pharmaceutical

How Ildong Pharmaceutical Has Been Performing

While the industry has experienced revenue growth lately, Ildong Pharmaceutical's revenue has gone into reverse gear, which is not great. It might be that many expect the dour revenue performance to strengthen positively, which has kept the P/S from falling. If not, then existing shareholders may be a little nervous about the viability of the share price.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Ildong Pharmaceutical.How Is Ildong Pharmaceutical's Revenue Growth Trending?

The only time you'd be comfortable seeing a P/S like Ildong Pharmaceutical's is when the company's growth is tracking the industry closely.

Taking a look back first, the company's revenue growth last year wasn't something to get excited about as it posted a disappointing decline of 2.9%. This has soured the latest three-year period, which nevertheless managed to deliver a decent 8.9% overall rise in revenue. So we can start by confirming that the company has generally done a good job of growing revenue over that time, even though it had some hiccups along the way.

Looking ahead now, revenue is anticipated to climb by 5.8% during the coming year according to the only analyst following the company. That's shaping up to be materially lower than the 59% growth forecast for the broader industry.

With this in mind, we find it intriguing that Ildong Pharmaceutical's P/S is closely matching its industry peers. Apparently many investors in the company are less bearish than analysts indicate and aren't willing to let go of their stock right now. Maintaining these prices will be difficult to achieve as this level of revenue growth is likely to weigh down the shares eventually.

What Does Ildong Pharmaceutical's P/S Mean For Investors?

Ildong Pharmaceutical appears to be back in favour with a solid price jump bringing its P/S back in line with other companies in the industry Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

When you consider that Ildong Pharmaceutical's revenue growth estimates are fairly muted compared to the broader industry, it's easy to see why we consider it unexpected to be trading at its current P/S ratio. At present, we aren't confident in the P/S as the predicted future revenues aren't likely to support a more positive sentiment for long. Circumstances like this present a risk to current and prospective investors who may see share prices fall if the low revenue growth impacts the sentiment.

Before you settle on your opinion, we've discovered 1 warning sign for Ildong Pharmaceutical that you should be aware of.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSE:A249420

Ildong Pharmaceutical

Develops, manufactures, and sells pharmaceutical products in South Korea.

Good value with mediocre balance sheet.

Market Insights

Community Narratives