- South Korea

- /

- Biotech

- /

- KOSDAQ:A226950

It's Down 36% But OliX Pharmaceuticals, Inc (KOSDAQ:226950) Could Be Riskier Than It Looks

Unfortunately for some shareholders, the OliX Pharmaceuticals, Inc (KOSDAQ:226950) share price has dived 36% in the last thirty days, prolonging recent pain. The drop over the last 30 days has capped off a tough year for shareholders, with the share price down 44% in that time.

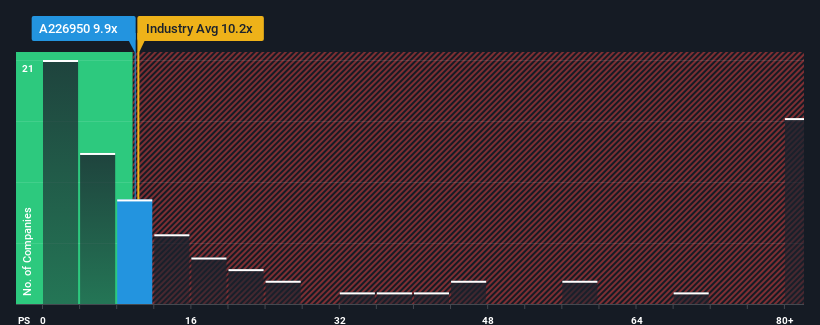

In spite of the heavy fall in price, there still wouldn't be many who think OliX Pharmaceuticals' price-to-sales (or "P/S") ratio of 9.9x is worth a mention when the median P/S in Korea's Biotechs industry is similar at about 10.2x. Although, it's not wise to simply ignore the P/S without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

View our latest analysis for OliX Pharmaceuticals

How Has OliX Pharmaceuticals Performed Recently?

OliX Pharmaceuticals certainly has been doing a great job lately as it's been growing its revenue at a really rapid pace. Perhaps the market is expecting future revenue performance to taper off, which has kept the P/S from rising. Those who are bullish on OliX Pharmaceuticals will be hoping that this isn't the case, so that they can pick up the stock at a lower valuation.

Want the full picture on earnings, revenue and cash flow for the company? Then our free report on OliX Pharmaceuticals will help you shine a light on its historical performance.How Is OliX Pharmaceuticals' Revenue Growth Trending?

In order to justify its P/S ratio, OliX Pharmaceuticals would need to produce growth that's similar to the industry.

Taking a look back first, we see that the company grew revenue by an impressive 68% last year. The latest three year period has also seen an incredible overall rise in revenue, aided by its incredible short-term performance. Therefore, it's fair to say the revenue growth recently has been superb for the company.

Comparing that to the industry, which is only predicted to deliver 30% growth in the next 12 months, the company's momentum is stronger based on recent medium-term annualised revenue results.

With this information, we find it interesting that OliX Pharmaceuticals is trading at a fairly similar P/S compared to the industry. Apparently some shareholders believe the recent performance is at its limits and have been accepting lower selling prices.

What We Can Learn From OliX Pharmaceuticals' P/S?

With its share price dropping off a cliff, the P/S for OliX Pharmaceuticals looks to be in line with the rest of the Biotechs industry. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

To our surprise, OliX Pharmaceuticals revealed its three-year revenue trends aren't contributing to its P/S as much as we would have predicted, given they look better than current industry expectations. There could be some unobserved threats to revenue preventing the P/S ratio from matching this positive performance. While recent revenue trends over the past medium-term suggest that the risk of a price decline is low, investors appear to see the likelihood of revenue fluctuations in the future.

You need to take note of risks, for example - OliX Pharmaceuticals has 3 warning signs (and 1 which shouldn't be ignored) we think you should know about.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About KOSDAQ:A226950

OliX Pharmaceuticals

A clinical stage pharmaceutical company, focuses on developing RNA interference (RNAi) therapeutics for dermal, ophthalmic, and pulmonary diseases.

Low with weak fundamentals.

Market Insights

Community Narratives