Advertisement

- South Korea

- /

- Metals and Mining

- /

- KOSE:A008970

Is There More Growth In Store For Dong Yang Steel Pipe's (KRX:008970) Returns On Capital?

If you're not sure where to start when looking for the next multi-bagger, there are a few key trends you should keep an eye out for. Amongst other things, we'll want to see two things; firstly, a growing return on capital employed (ROCE) and secondly, an expansion in the company's amount of capital employed. Basically this means that a company has profitable initiatives that it can continue to reinvest in, which is a trait of a compounding machine. With that in mind, we've noticed some promising trends at Dong Yang Steel Pipe (KRX:008970) so let's look a bit deeper.

What is Return On Capital Employed (ROCE)?

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. To calculate this metric for Dong Yang Steel Pipe, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

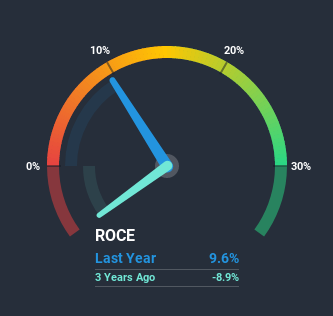

0.096 = ₩9.3b ÷ (₩168b - ₩71b) (Based on the trailing twelve months to September 2020).

Thus, Dong Yang Steel Pipe has an ROCE of 9.6%. In absolute terms, that's a low return, but it's much better than the Metals and Mining industry average of 4.1%.

View our latest analysis for Dong Yang Steel Pipe

While the past is not representative of the future, it can be helpful to know how a company has performed historically, which is why we have this chart above. If you want to delve into the historical earnings, revenue and cash flow of Dong Yang Steel Pipe, check out these free graphs here.

How Are Returns Trending?

Dong Yang Steel Pipe is showing promise given that its ROCE is trending up and to the right. The figures show that over the last five years, ROCE has grown 647% whilst employing roughly the same amount of capital. Basically the business is generating higher returns from the same amount of capital and that is proof that there are improvements in the company's efficiencies. On that front, things are looking good so it's worth exploring what management has said about growth plans going forward.

On a separate but related note, it's important to know that Dong Yang Steel Pipe has a current liabilities to total assets ratio of 42%, which we'd consider pretty high. This effectively means that suppliers (or short-term creditors) are funding a large portion of the business, so just be aware that this can introduce some elements of risk. Ideally we'd like to see this reduce as that would mean fewer obligations bearing risks.

The Bottom Line

To sum it up, Dong Yang Steel Pipe is collecting higher returns from the same amount of capital, and that's impressive. Investors may not be impressed by the favorable underlying trends yet because over the last five years the stock has only returned 9.4% to shareholders. So exploring more about this stock could uncover a good opportunity, if the valuation and other metrics stack up.

While Dong Yang Steel Pipe looks impressive, no company is worth an infinite price. The intrinsic value infographic in our free research report helps visualize whether A008970 is currently trading for a fair price.

If you want to search for solid companies with great earnings, check out this free list of companies with good balance sheets and impressive returns on equity.

When trading Dong Yang Steel Pipe or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Kbi Dong Yang Steel PipeLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KOSE:A008970

Kbi Dong Yang Steel PipeLtd

Manufactures and sells steel pipes in South Korea, the United States, rest of Asia, Europe, the Middle East, and internationally.

Adequate balance sheet with questionable track record.

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|3.1% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|11.6% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|39.4% undervalued

TR

Community Contributor