Advertisement

- South Korea

- /

- Chemicals

- /

- KOSE:A004430

Can Songwon Industrial (KRX:004430) Continue To Grow Its Returns On Capital?

If we want to find a potential multi-bagger, often there are underlying trends that can provide clues. One common approach is to try and find a company with returns on capital employed (ROCE) that are increasing, in conjunction with a growing amount of capital employed. If you see this, it typically means it's a company with a great business model and plenty of profitable reinvestment opportunities. With that in mind, we've noticed some promising trends at Songwon Industrial (KRX:004430) so let's look a bit deeper.

Return On Capital Employed (ROCE): What is it?

Just to clarify if you're unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. Analysts use this formula to calculate it for Songwon Industrial:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

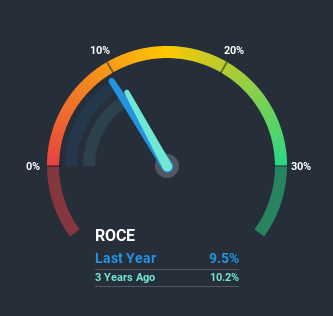

0.095 = ₩58b ÷ (₩907b - ₩293b) (Based on the trailing twelve months to September 2020).

Thus, Songwon Industrial has an ROCE of 9.5%. On its own, that's a low figure but it's around the 8.0% average generated by the Chemicals industry.

Check out our latest analysis for Songwon Industrial

In the above chart we have measured Songwon Industrial's prior ROCE against its prior performance, but the future is arguably more important. If you'd like, you can check out the forecasts from the analysts covering Songwon Industrial here for free.

What The Trend Of ROCE Can Tell Us

While in absolute terms it isn't a high ROCE, it's promising to see that it has been moving in the right direction. The data shows that returns on capital have increased substantially over the last five years to 9.5%. The company is effectively making more money per dollar of capital used, and it's worth noting that the amount of capital has increased too, by 37%. This can indicate that there's plenty of opportunities to invest capital internally and at ever higher rates, a combination that's common among multi-baggers.

In another part of our analysis, we noticed that the company's ratio of current liabilities to total assets decreased to 32%, which broadly means the business is relying less on its suppliers or short-term creditors to fund its operations. Therefore we can rest assured that the growth in ROCE is a result of the business' fundamental improvements, rather than a cooking class featuring this company's books.

What We Can Learn From Songwon Industrial's ROCE

All in all, it's terrific to see that Songwon Industrial is reaping the rewards from prior investments and is growing its capital base. Investors may not be impressed by the favorable underlying trends yet because over the last five years the stock has only returned 14% to shareholders. So exploring more about this stock could uncover a good opportunity, if the valuation and other metrics stack up.

If you want to continue researching Songwon Industrial, you might be interested to know about the 2 warning signs that our analysis has discovered.

While Songwon Industrial isn't earning the highest return, check out this free list of companies that are earning high returns on equity with solid balance sheets.

If you’re looking to trade Songwon Industrial, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KOSE:A004430

Songwon Industrial

Manufactures and sells polymer stabilizers, tin intermediates, PVC stabilizers, and specialty chemicals in South Korea, Rest of Asia, Europe, North and South America, Australia, the Middle East, and Africa.

Flawless balance sheet with solid track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

Pole position to benefit from GENIUS Act

Fair Value US$233.04|58.8% undervalued

CH

Community Contributor

IREN will transform from bitcoin miner to leader in AI infrastructure

Fair Value US$21.48|17.5% undervalued

KA

Community Contributor

Behind the Assay: XRF Scientific’s Role in Modern Mining Economics

Fair Value AU$2.10|2.4% undervalued

RO

Community Contributor