Advertisement

- South Korea

- /

- Basic Materials

- /

- KOSDAQ:A075970

Dongkuk Refractories & Steel Co., Ltd.'s (KOSDAQ:075970) Stock Has Seen Strong Momentum: Does That Call For Deeper Study Of Its Financial Prospects?

Most readers would already be aware that Dongkuk Refractories & Steel's (KOSDAQ:075970) stock increased significantly by 21% over the past three months. Given that stock prices are usually aligned with a company's financial performance in the long-term, we decided to study its financial indicators more closely to see if they had a hand to play in the recent price move. Specifically, we decided to study Dongkuk Refractories & Steel's ROE in this article.

Return on equity or ROE is an important factor to be considered by a shareholder because it tells them how effectively their capital is being reinvested. In simpler terms, it measures the profitability of a company in relation to shareholder's equity.

Check out our latest analysis for Dongkuk Refractories & Steel

How Is ROE Calculated?

ROE can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Dongkuk Refractories & Steel is:

3.4% = ₩2.7b ÷ ₩81b (Based on the trailing twelve months to September 2020).

The 'return' is the income the business earned over the last year. Another way to think of that is that for every ₩1 worth of equity, the company was able to earn ₩0.03 in profit.

What Is The Relationship Between ROE And Earnings Growth?

We have already established that ROE serves as an efficient profit-generating gauge for a company's future earnings. We now need to evaluate how much profit the company reinvests or "retains" for future growth which then gives us an idea about the growth potential of the company. Generally speaking, other things being equal, firms with a high return on equity and profit retention, have a higher growth rate than firms that don’t share these attributes.

A Side By Side comparison of Dongkuk Refractories & Steel's Earnings Growth And 3.4% ROE

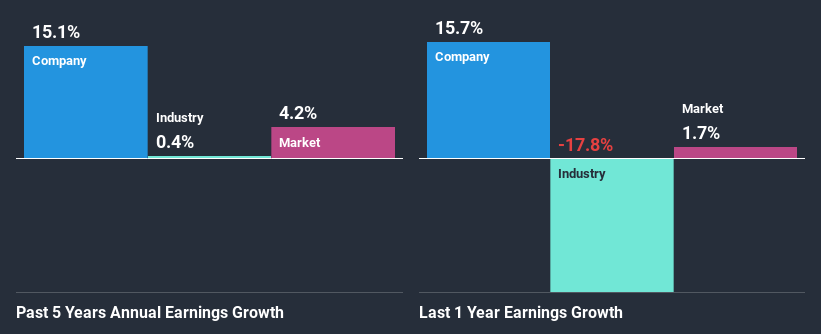

It is hard to argue that Dongkuk Refractories & Steel's ROE is much good in and of itself. Further, we noted that the company's ROE is similar to the industry average of 3.1%. However, the modest 15% net income growth seen by Dongkuk Refractories & Steel over the past five years is a positive sign. Given the low ROE, it is likely that there could be some other aspects that are driving this growth as well. Such as - high earnings retention or an efficient management in place.

Next, on comparing with the industry net income growth, we found that Dongkuk Refractories & Steel's growth is quite high when compared to the industry average growth of 0.4% in the same period, which is great to see.

Earnings growth is an important metric to consider when valuing a stock. The investor should try to establish if the expected growth or decline in earnings, whichever the case may be, is priced in. Doing so will help them establish if the stock's future looks promising or ominous. One good indicator of expected earnings growth is the P/E ratio which determines the price the market is willing to pay for a stock based on its earnings prospects. So, you may want to check if Dongkuk Refractories & Steel is trading on a high P/E or a low P/E, relative to its industry.

Is Dongkuk Refractories & Steel Efficiently Re-investing Its Profits?

Dongkuk Refractories & Steel has a significant three-year median payout ratio of 59%, meaning that it is left with only 41% to reinvest into its business. This implies that the company has been able to achieve decent earnings growth despite returning most of its profits to shareholders.

Along with seeing a growth in earnings, Dongkuk Refractories & Steel only recently started paying dividends. Its quite possible that the company was looking to impress its shareholders.

Conclusion

In total, it does look like Dongkuk Refractories & Steel has some positive aspects to its business. That is, quite an impressive growth in earnings. However, the low profit retention means that the company's earnings growth could have been higher, had it been reinvesting a higher portion of its profits. Until now, we have only just grazed the surface of the company's past performance by looking at the company's fundamentals. So it may be worth checking this free detailed graph of Dongkuk Refractories & Steel's past earnings, as well as revenue and cash flows to get a deeper insight into the company's performance.

When trading Dongkuk Refractories & Steel or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KOSDAQ:A075970

Dongkuk Refractories & Steel

Manufactures and sells refractories and ceramics in South Korea and internationally.

Proven track record with mediocre balance sheet.

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|24.5% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|45.3% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|33.9% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|57.0% undervalued

AX

Community Contributor