Advertisement

- South Korea

- /

- Insurance

- /

- KOSE:A001450

Hyundai Marine & Fire Insurance Co., Ltd. (KRX:001450) Screens Well But There Might Be A Catch

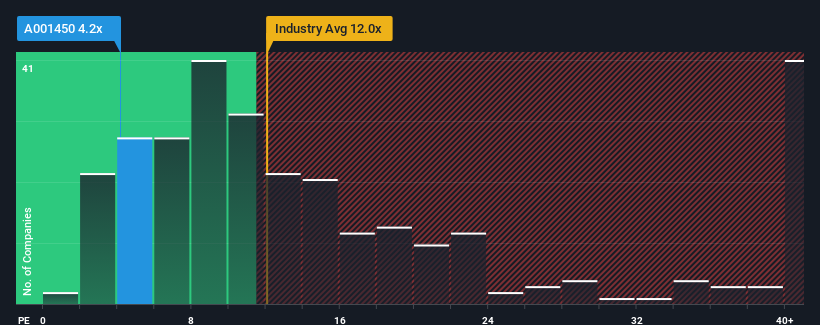

When close to half the companies in Korea have price-to-earnings ratios (or "P/E's") above 14x, you may consider Hyundai Marine & Fire Insurance Co., Ltd. (KRX:001450) as a highly attractive investment with its 4.2x P/E ratio. However, the P/E might be quite low for a reason and it requires further investigation to determine if it's justified.

Hyundai Marine & Fire Insurance has been struggling lately as its earnings have declined faster than most other companies. The P/E is probably low because investors think this poor earnings performance isn't going to improve at all. If you still like the company, you'd want its earnings trajectory to turn around before making any decisions. Or at the very least, you'd be hoping the earnings slide doesn't get any worse if your plan is to pick up some stock while it's out of favour.

Check out our latest analysis for Hyundai Marine & Fire Insurance

How Is Hyundai Marine & Fire Insurance's Growth Trending?

Hyundai Marine & Fire Insurance's P/E ratio would be typical for a company that's expected to deliver very poor growth or even falling earnings, and importantly, perform much worse than the market.

If we review the last year of earnings, dishearteningly the company's profits fell to the tune of 53%. Still, the latest three year period has seen an excellent 92% overall rise in EPS, in spite of its unsatisfying short-term performance. Although it's been a bumpy ride, it's still fair to say the earnings growth recently has been more than adequate for the company.

Looking ahead now, EPS is anticipated to climb by 24% per year during the coming three years according to the analysts following the company. That's shaping up to be materially higher than the 20% per annum growth forecast for the broader market.

In light of this, it's peculiar that Hyundai Marine & Fire Insurance's P/E sits below the majority of other companies. It looks like most investors are not convinced at all that the company can achieve future growth expectations.

The Key Takeaway

Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

We've established that Hyundai Marine & Fire Insurance currently trades on a much lower than expected P/E since its forecast growth is higher than the wider market. There could be some major unobserved threats to earnings preventing the P/E ratio from matching the positive outlook. At least price risks look to be very low, but investors seem to think future earnings could see a lot of volatility.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 3 warning signs with Hyundai Marine & Fire Insurance, and understanding them should be part of your investment process.

Of course, you might also be able to find a better stock than Hyundai Marine & Fire Insurance. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Valuation is complex, but we're here to simplify it.

Discover if Hyundai Marine & Fire Insurance might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSE:A001450

Hyundai Marine & Fire Insurance

Hyundai Marine & Fire Insurance Co., Ltd.

Undervalued with adequate balance sheet and pays a dividend.

Market Insights

Advertisement

Community Narratives

Nike's Direct-to-Consumer Focus Will Drive Future Growth

Fair Value US$87.90|18.2% undervalued

UN

Community Contributor

Novo Nordisk will dominate GLP-1 market with Ozempic and Wegovy growth

Fair Value US$89.59|12.1% undervalued

BE

Community Contributor

Rheinmetall could get 20-25% of EU-NATO 3%-GDP defence spending

Fair Value €7.57k|82.4% undervalued

NO

Community Contributor