- South Korea

- /

- Insurance

- /

- KOSE:A000810

There's Reason For Concern Over Samsung Fire & Marine Insurance Co., Ltd.'s (KRX:000810) Massive 26% Price Jump

Samsung Fire & Marine Insurance Co., Ltd. (KRX:000810) shares have had a really impressive month, gaining 26% after a shaky period beforehand. Looking back a bit further, it's encouraging to see the stock is up 67% in the last year.

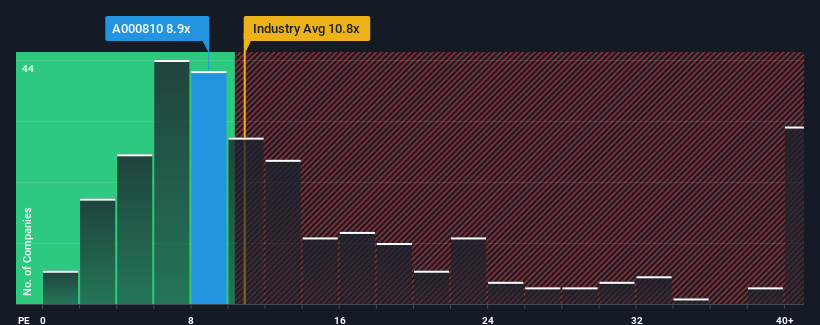

Although its price has surged higher, there still wouldn't be many who think Samsung Fire & Marine Insurance's price-to-earnings (or "P/E") ratio of 9x is worth a mention when the median P/E in Korea is similar at about 11x. Although, it's not wise to simply ignore the P/E without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

Recent times have been advantageous for Samsung Fire & Marine Insurance as its earnings have been rising faster than most other companies. It might be that many expect the strong earnings performance to wane, which has kept the P/E from rising. If not, then existing shareholders have reason to be feeling optimistic about the future direction of the share price.

See our latest analysis for Samsung Fire & Marine Insurance

What Are Growth Metrics Telling Us About The P/E?

The only time you'd be comfortable seeing a P/E like Samsung Fire & Marine Insurance's is when the company's growth is tracking the market closely.

Retrospectively, the last year delivered a decent 3.0% gain to the company's bottom line. The latest three year period has also seen an excellent 76% overall rise in EPS, aided somewhat by its short-term performance. Therefore, it's fair to say the earnings growth recently has been superb for the company.

Shifting to the future, estimates from the eleven analysts covering the company suggest earnings should grow by 15% over the next year. That's shaping up to be materially lower than the 36% growth forecast for the broader market.

With this information, we find it interesting that Samsung Fire & Marine Insurance is trading at a fairly similar P/E to the market. Apparently many investors in the company are less bearish than analysts indicate and aren't willing to let go of their stock right now. These shareholders may be setting themselves up for future disappointment if the P/E falls to levels more in line with the growth outlook.

The Final Word

Samsung Fire & Marine Insurance appears to be back in favour with a solid price jump getting its P/E back in line with most other companies. While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

We've established that Samsung Fire & Marine Insurance currently trades on a higher than expected P/E since its forecast growth is lower than the wider market. When we see a weak earnings outlook with slower than market growth, we suspect the share price is at risk of declining, sending the moderate P/E lower. Unless these conditions improve, it's challenging to accept these prices as being reasonable.

Don't forget that there may be other risks. For instance, we've identified 1 warning sign for Samsung Fire & Marine Insurance that you should be aware of.

It's important to make sure you look for a great company, not just the first idea you come across. So take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSE:A000810

Samsung Fire & Marine Insurance

Engages in the provision of non-life insurance products and services in Korea, China, the United States, Indonesia, Vietnam, Singapore, and the United Kingdom.

Undervalued established dividend payer.

Market Insights

Community Narratives