Advertisement

- South Korea

- /

- Personal Products

- /

- KOSE:A024720

Kolmar Holdings Co.,Ltd. (KRX:024720) Stock Is Going Strong But Fundamentals Look Uncertain: What Lies Ahead ?

Kolmar HoldingsLtd (KRX:024720) has had a great run on the share market with its stock up by a significant 68% over the last three months. However, we decided to pay attention to the company's fundamentals which don't appear to give a clear sign about the company's financial health. Particularly, we will be paying attention to Kolmar HoldingsLtd's ROE today.

Return on Equity or ROE is a test of how effectively a company is growing its value and managing investors’ money. Put another way, it reveals the company's success at turning shareholder investments into profits.

How To Calculate Return On Equity?

The formula for return on equity is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Kolmar HoldingsLtd is:

3.2% = ₩26b ÷ ₩800b (Based on the trailing twelve months to March 2025).

The 'return' is the amount earned after tax over the last twelve months. That means that for every ₩1 worth of shareholders' equity, the company generated ₩0.03 in profit.

View our latest analysis for Kolmar HoldingsLtd

What Has ROE Got To Do With Earnings Growth?

We have already established that ROE serves as an efficient profit-generating gauge for a company's future earnings. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Generally speaking, other things being equal, firms with a high return on equity and profit retention, have a higher growth rate than firms that don’t share these attributes.

Kolmar HoldingsLtd's Earnings Growth And 3.2% ROE

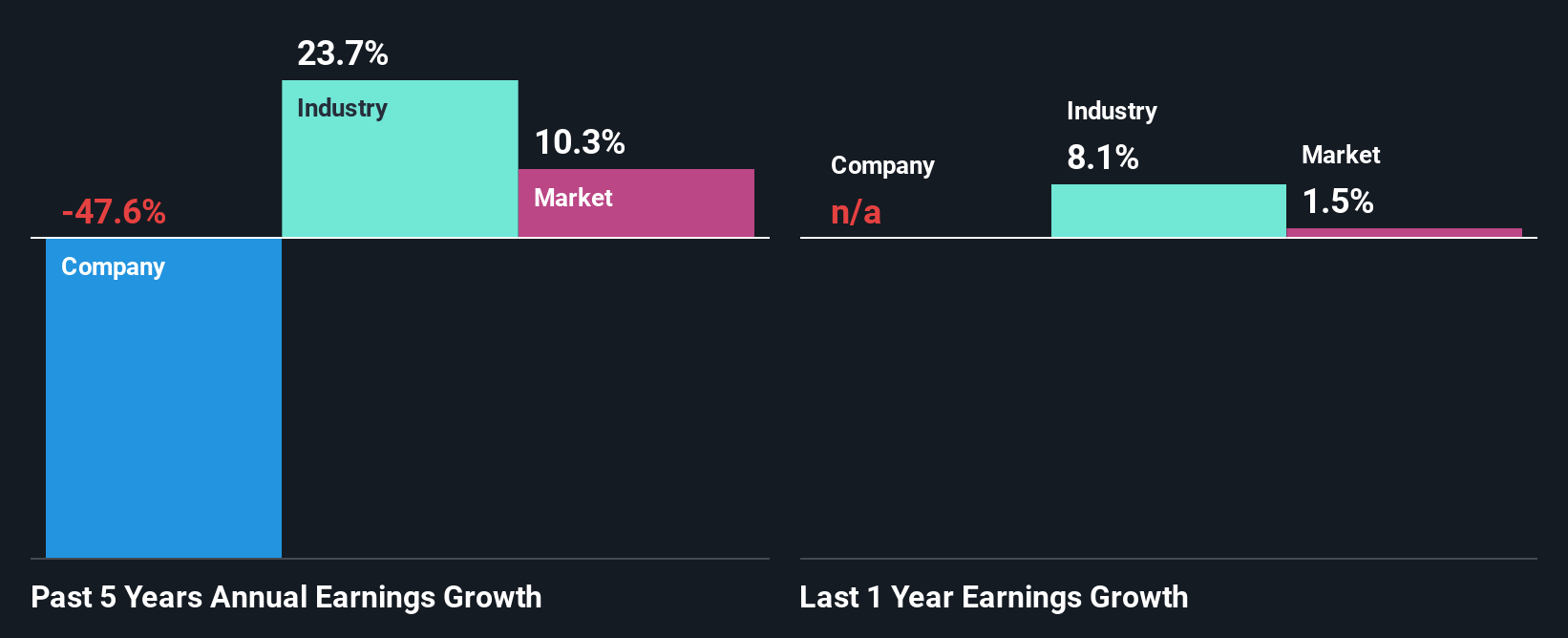

It is hard to argue that Kolmar HoldingsLtd's ROE is much good in and of itself. Even compared to the average industry ROE of 9.3%, the company's ROE is quite dismal. Given the circumstances, the significant decline in net income by 48% seen by Kolmar HoldingsLtd over the last five years is not surprising. We reckon that there could also be other factors at play here. Such as - low earnings retention or poor allocation of capital.

So, as a next step, we compared Kolmar HoldingsLtd's performance against the industry and were disappointed to discover that while the company has been shrinking its earnings, the industry has been growing its earnings at a rate of 24% over the last few years.

Earnings growth is a huge factor in stock valuation. The investor should try to establish if the expected growth or decline in earnings, whichever the case may be, is priced in. This then helps them determine if the stock is placed for a bright or bleak future. Is Kolmar HoldingsLtd fairly valued compared to other companies? These 3 valuation measures might help you decide.

Is Kolmar HoldingsLtd Using Its Retained Earnings Effectively?

In spite of a normal LTM (or last twelve month) payout ratio of 34% (that is, a retention ratio of 66%), the fact that Kolmar HoldingsLtd's earnings have shrunk is quite puzzling. So there could be some other explanations in that regard. For instance, the company's business may be deteriorating.

Moreover, Kolmar HoldingsLtd has been paying dividends for six years, which is a considerable amount of time, suggesting that management must have perceived that the shareholders prefer consistent dividends even though earnings have been shrinking.

Conclusion

Overall, we have mixed feelings about Kolmar HoldingsLtd. Even though it appears to be retaining most of its profits, given the low ROE, investors may not be benefitting from all that reinvestment after all. The low earnings growth suggests our theory correct. Wrapping up, we would proceed with caution with this company and one way of doing that would be to look at the risk profile of the business. You can see the 4 risks we have identified for Kolmar HoldingsLtd by visiting our risks dashboard for free on our platform here.

Valuation is complex, but we're here to simplify it.

Discover if Kolmar HoldingsLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSE:A024720

Kolmar HoldingsLtd

Manufactures and sells cosmetics, pharmaceuticals, and health functional foods in South Korea and internationally.

Slight risk and slightly overvalued.

Market Insights

Advertisement

Community Narratives

America Wants Homegrown Drones — Draganfly Is Ready to Deliver

Fair Value US$9.21|32.6% undervalued

JO

Community Contributor

Cheesecake Factory offers an enticing opportunity for long-term growth by leveraging new concepts

Fair Value US$73.83|25.6% undervalued

ZW

Community Contributor

Coca-Cola’s Intrinsic Value Set to Rise with Fed Rate Cut

Fair Value US$67.50|1.6% undervalued

AL

Community Contributor

Fully Permitted Gold Mine with 50 Baggers Potential

Fair Value CA$41.00|98.2% undervalued

RO

Community Contributor