- South Korea

- /

- Medical Equipment

- /

- KOSDAQ:A228850

Income Investors Should Know That Rayence Co., Ltd. (KOSDAQ:228850) Goes Ex-Dividend Soon

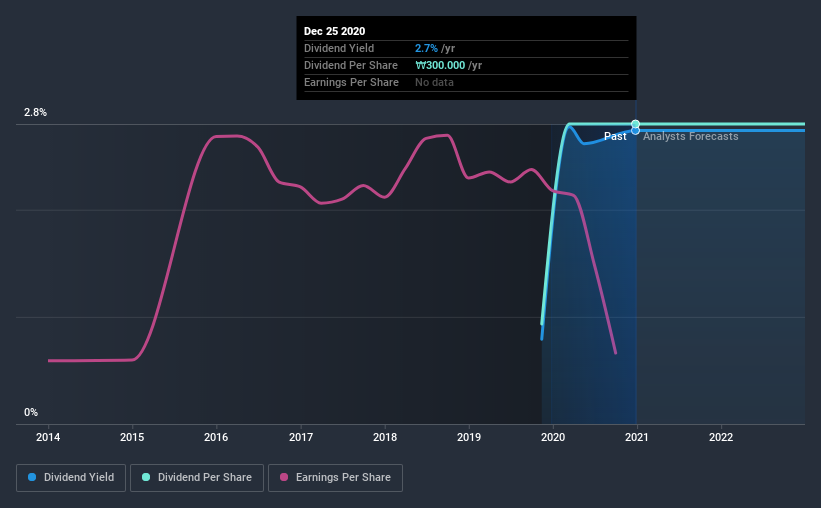

Rayence Co., Ltd. (KOSDAQ:228850) stock is about to trade ex-dividend in 3 days. This means that investors who purchase shares on or after the 29th of December will not receive the dividend, which will be paid on the 10th of April.

Rayence's upcoming dividend is ₩300 a share, following on from the last 12 months, when the company distributed a total of ₩300 per share to shareholders. Calculating the last year's worth of payments shows that Rayence has a trailing yield of 2.7% on the current share price of ₩10950. Dividends are an important source of income to many shareholders, but the health of the business is crucial to maintaining those dividends. So we need to check whether the dividend payments are covered, and if earnings are growing.

See our latest analysis for Rayence

Dividends are typically paid from company earnings. If a company pays more in dividends than it earned in profit, then the dividend could be unsustainable. Last year, Rayence paid out 106% of its income as dividends, which is above a level that we're comfortable with, especially if the company needs to reinvest in its business. Yet cash flow is typically more important than profit for assessing dividend sustainability, so we should always check if the company generated enough cash to afford its dividend. Thankfully its dividend payments took up just 26% of the free cash flow it generated, which is a comfortable payout ratio.

It's good to see that while Rayence's dividends were not covered by profits, at least they are affordable from a cash perspective. If executives were to continue paying more in dividends than the company reported in profits, we'd view this as a warning sign. Very few companies are able to sustainably pay dividends larger than their reported earnings.

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Businesses with strong growth prospects usually make the best dividend payers, because it's easier to grow dividends when earnings per share are improving. If business enters a downturn and the dividend is cut, the company could see its value fall precipitously. This is why it's a relief to see Rayence earnings per share are up 2.1% per annum over the last five years.

Given that Rayence has only been paying a dividend for a year, there's not much of a past history to draw insight from.

The Bottom Line

Has Rayence got what it takes to maintain its dividend payments? Rayence has been steadily growing its earnings per share, and it is paying out just 26% of its cash flow but an uncomfortably high 106% of its income. Overall, it's not a bad combination, but we feel that there are likely more attractive dividend prospects out there.

With that being said, if dividends aren't your biggest concern with Rayence, you should know about the other risks facing this business. For example, we've found 3 warning signs for Rayence that we recommend you consider before investing in the business.

A common investment mistake is buying the first interesting stock you see. Here you can find a list of promising dividend stocks with a greater than 2% yield and an upcoming dividend.

If you’re looking to trade Rayence, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

If you're looking to trade Rayence, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KOSDAQ:A228850

Rayence

Engages in the development, manufacture, and sale of digital X-ray detector products for dental, medical, veterinary, and industrial sectors in South Korea, the United States, Mexico, China, and internationally.

Flawless balance sheet second-rate dividend payer.