- Taiwan

- /

- Electronic Equipment and Components

- /

- TPEX:6274

March 2025's Asian Stocks Priced Below Estimated Value

Reviewed by Simply Wall St

As global markets navigate a landscape marked by economic uncertainty and mixed signals from major economies, the Asian stock market presents intriguing opportunities for investors seeking value. In this context, identifying undervalued stocks becomes crucial, as these assets may offer potential upside when broader market conditions stabilize.

Top 10 Undervalued Stocks Based On Cash Flows In Asia

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| DIP (TSE:2379) | ¥2288.00 | ¥4572.89 | 50% |

| Chison Medical Technologies (SHSE:688358) | CN¥31.19 | CN¥61.39 | 49.2% |

| Guizhou Space Appliance (SZSE:002025) | CN¥57.74 | CN¥114.89 | 49.7% |

| RACCOON HOLDINGS (TSE:3031) | ¥963.00 | ¥1885.03 | 48.9% |

| STI (KOSDAQ:A039440) | ₩22450.00 | ₩43978.70 | 49% |

| Bide Pharmatech (SHSE:688073) | CN¥54.20 | CN¥106.91 | 49.3% |

| Takara Bio (TSE:4974) | ¥850.00 | ¥1685.20 | 49.6% |

| APAC Realty (SGX:CLN) | SGD0.43 | SGD0.85 | 49.4% |

| Siam Wellness Group (SET:SPA) | THB4.64 | THB9.12 | 49.1% |

| Yuhan (KOSE:A000100) | ₩121500.00 | ₩237586.28 | 48.9% |

Let's review some notable picks from our screened stocks.

CLASSYS (KOSDAQ:A214150)

Overview: CLASSYS Inc. is a company that provides medical aesthetics devices globally, with a market cap of ₩3.82 trillion.

Operations: Revenue Segments (in millions of ₩):

Estimated Discount To Fair Value: 39.4%

CLASSYS appears undervalued based on cash flows, trading at ₩58,400, significantly below its estimated fair value of ₩96,307.57. The company has demonstrated robust financial performance with earnings growing 31.9% last year and forecasted revenue growth of 21.8% annually, surpassing the Korean market average. Despite recent share price volatility and no buyback activity in the latest tranche update, CLASSYS's strong projected earnings growth suggests potential for future value realization.

- The analysis detailed in our CLASSYS growth report hints at robust future financial performance.

- Navigate through the intricacies of CLASSYS with our comprehensive financial health report here.

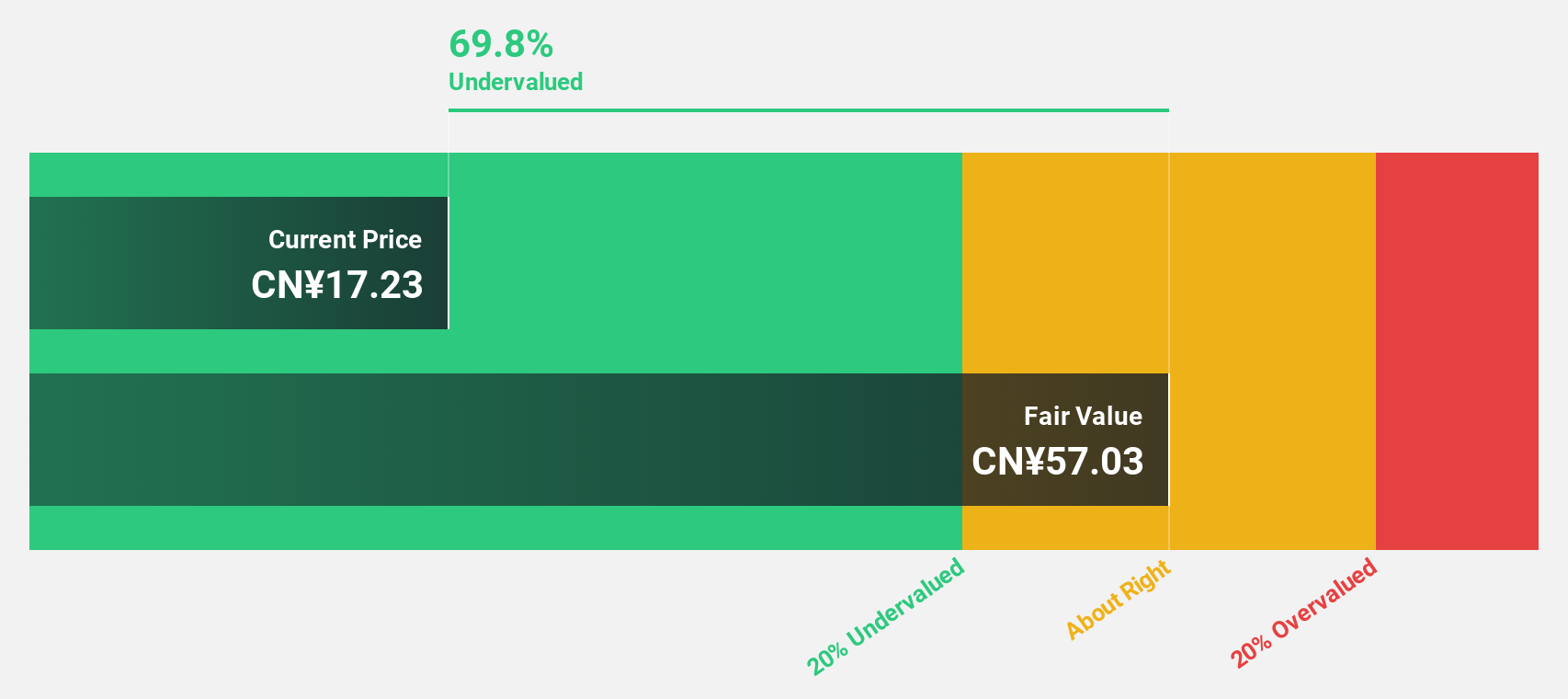

Sunstone Development (SHSE:603612)

Overview: Sunstone Development Co., Ltd. focuses on the R&D, production, and sales of prebaked carbon anodes for the aluminum industry both in China and internationally, with a market cap of CN¥8.33 billion.

Operations: The company's revenue is primarily derived from its activities in the research, development, production, and sales of prebaked carbon anodes for the aluminum industry.

Estimated Discount To Fair Value: 45.5%

Sunstone Development is trading at CN¥17.44, significantly below its estimated fair value of CN¥32.02, suggesting it may be undervalued based on cash flows. Despite a forecasted low return on equity of 11.7%, earnings are expected to grow 80.17% annually, with revenue growth projected at 23.6% per year—outpacing the Chinese market average of 13%. However, interest payments aren't well covered by earnings, which could pose financial challenges ahead.

- Upon reviewing our latest growth report, Sunstone Development's projected financial performance appears quite optimistic.

- Take a closer look at Sunstone Development's balance sheet health here in our report.

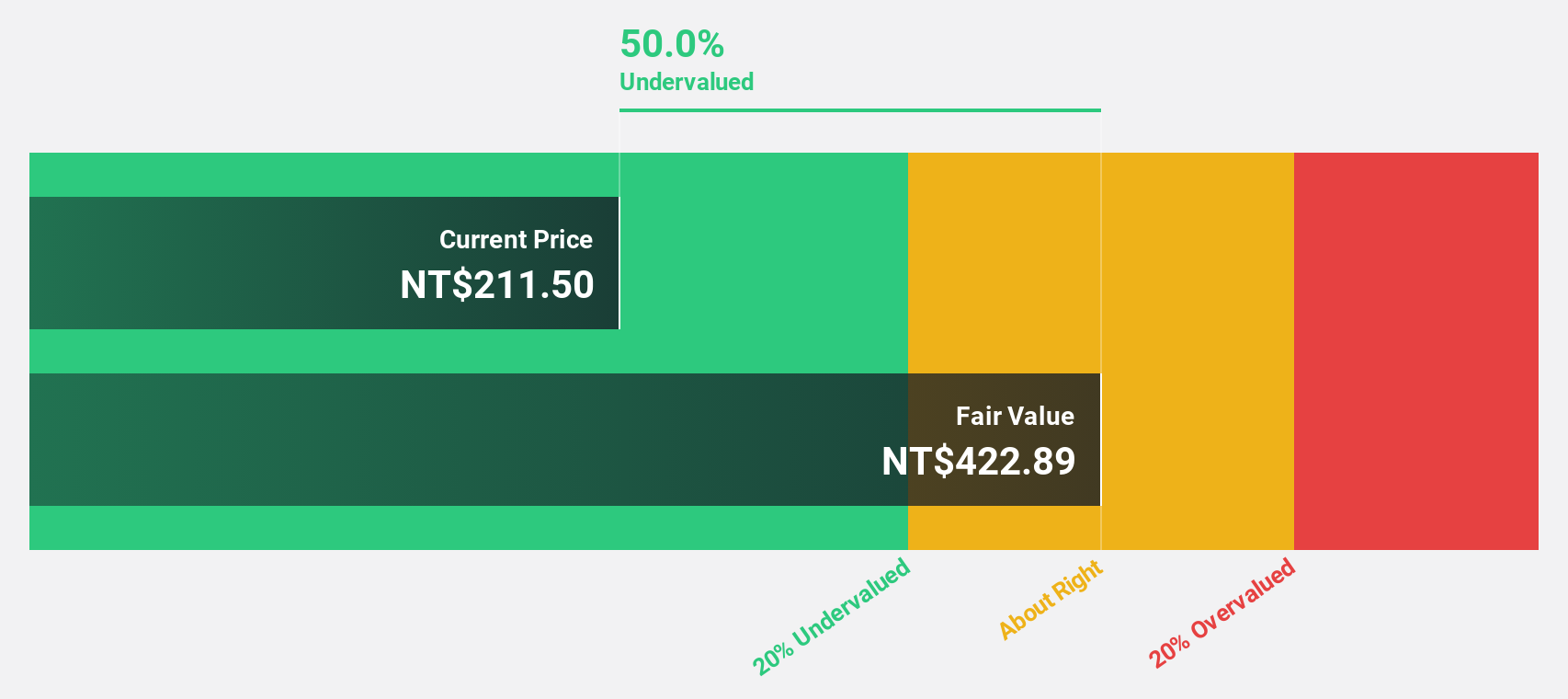

Taiwan Union Technology (TPEX:6274)

Overview: Taiwan Union Technology Corporation manufactures and sells copper foil substrates, adhesive sheets, and multi-layer laminated boards both in Taiwan and internationally, with a market cap of NT$47.74 billion.

Operations: The company generates revenue through the production and distribution of copper foil substrates, adhesive sheets, and multi-layer laminated boards in both domestic and international markets.

Estimated Discount To Fair Value: 48.8%

Taiwan Union Technology is trading at NT$173.5, well below its fair value of NT$338.81, highlighting potential undervaluation based on cash flows. Earnings grew substantially last year and are forecast to continue growing significantly at 23% annually, outpacing the TW market's 15.6%. Despite strong earnings growth, revenue is expected to grow more modestly at 15.4% per year. The dividend yield of 2.31% isn't fully covered by free cash flows, indicating potential sustainability concerns.

- The growth report we've compiled suggests that Taiwan Union Technology's future prospects could be on the up.

- Click here and access our complete balance sheet health report to understand the dynamics of Taiwan Union Technology.

Where To Now?

- Delve into our full catalog of 277 Undervalued Asian Stocks Based On Cash Flows here.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Taiwan Union Technology might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TPEX:6274

Taiwan Union Technology

Engages in the manufacture and sale of copper foil substrates, adhesive sheets, and multi-layer laminated boards in Taiwan and internationally.

Very undervalued with high growth potential.

Similar Companies

Market Insights

Community Narratives