- South Korea

- /

- Food

- /

- KOSE:A003230

3 KRX Growth Stocks With Insider Ownership Up To 34%

Reviewed by Simply Wall St

Over the last 7 days, the South Korean market has dropped 5.4%, driven by losses in every sector, and in the last 12 months, it is down 3.8%. Despite this downturn, earnings are forecast to grow by 29% annually, making growth companies with high insider ownership particularly appealing as they often signal confidence from those closest to the business.

Top 10 Growth Companies With High Insider Ownership In South Korea

| Name | Insider Ownership | Earnings Growth |

| People & Technology (KOSDAQ:A137400) | 16.5% | 35.6% |

| Seojin SystemLtd (KOSDAQ:A178320) | 30.5% | 52.1% |

| Bioneer (KOSDAQ:A064550) | 17.5% | 97.6% |

| ALTEOGEN (KOSDAQ:A196170) | 26.6% | 99.5% |

| Oscotec (KOSDAQ:A039200) | 26.3% | 122% |

| Vuno (KOSDAQ:A338220) | 19.5% | 110.9% |

| HANA Micron (KOSDAQ:A067310) | 21.3% | 106.2% |

| INTEKPLUS (KOSDAQ:A064290) | 16.3% | 96.7% |

| UTI (KOSDAQ:A179900) | 33.1% | 134.6% |

| Techwing (KOSDAQ:A089030) | 18.7% | 83.6% |

Here's a peek at a few of the choices from the screener.

CLASSYS (KOSDAQ:A214150)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: CLASSYS Inc. is a global provider of medical aesthetics devices with a market cap of ₩3.49 billion.

Operations: The company's revenue segment includes Surgical & Medical Equipment, generating ₩204.37 million.

Insider Ownership: 10.1%

CLASSYS Inc. is trading at 15.1% below its estimated fair value and has substantial insider ownership, which can align management's interests with shareholders. The company's earnings have grown 24.7% annually over the past five years and are forecast to grow significantly at 22.52% per year, although this is slower than the broader Korean market's expected growth of 28.6%. Recent presentations at major investor forums indicate active engagement with the investment community.

- Get an in-depth perspective on CLASSYS' performance by reading our analyst estimates report here.

- Our comprehensive valuation report raises the possibility that CLASSYS is priced higher than what may be justified by its financials.

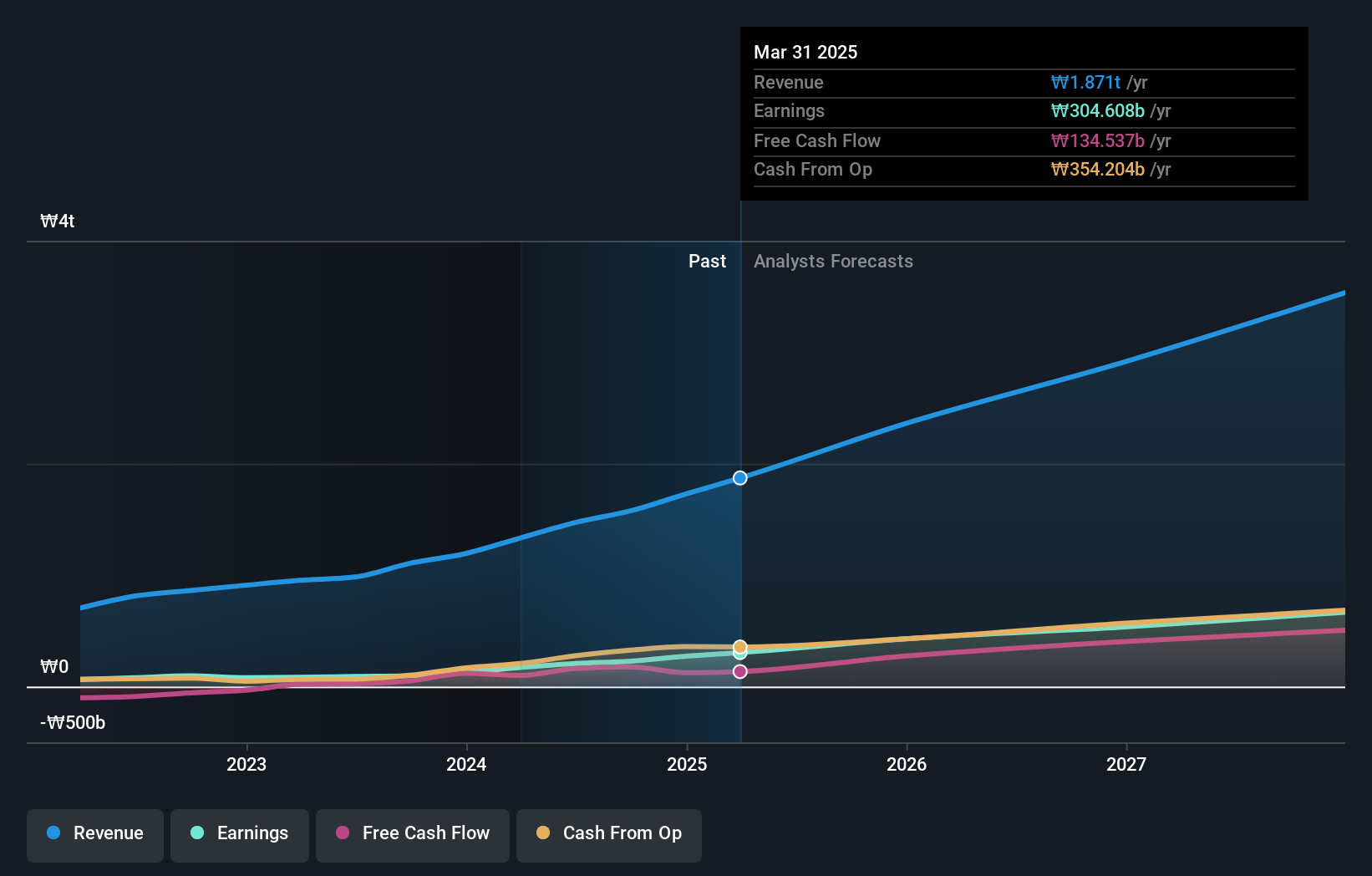

Samyang Foods (KOSE:A003230)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Samyang Foods Co., Ltd., along with its subsidiaries, operates in the food industry both in South Korea and internationally, with a market cap of ₩35.05 billion.

Operations: Samyang Foods generates revenue primarily from its food business operations in South Korea and international markets.

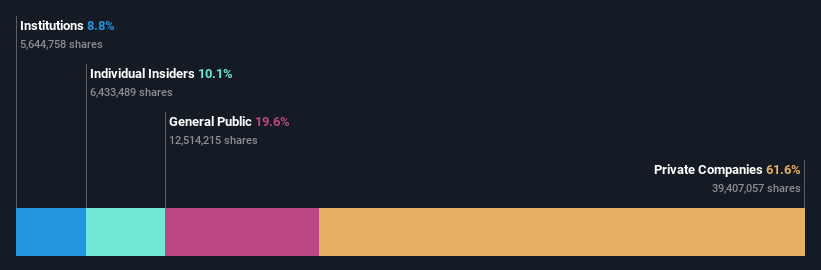

Insider Ownership: 11.6%

Samyang Foods exhibits strong growth characteristics with high insider ownership. Its earnings grew by 127.9% over the past year and are forecast to grow at 21.08% annually, though this is slower than the broader Korean market's expected growth of 28.6%. Revenue is projected to increase by 17.8% per year, outpacing the market's 10.3%. Trading at 64.7% below its estimated fair value, analysts predict a potential price rise of 41.7%.

- Click here to discover the nuances of Samyang Foods with our detailed analytical future growth report.

- Our expertly prepared valuation report Samyang Foods implies its share price may be lower than expected.

APR (KOSE:A278470)

Simply Wall St Growth Rating: ★★★★★☆

Overview: APR Co., Ltd manufactures and sells cosmetic products for men and women, with a market cap of ₩2.20 trillion.

Operations: The company's revenue segments include ₩614.77 billion from cosmetics and ₩64.46 billion from apparel fashion.

Insider Ownership: 34.4%

APR demonstrates strong growth potential with high insider ownership. Its revenue is forecast to grow at 22.2% per year, outpacing the Korean market's 10.3%. Earnings are expected to increase by 25.6% annually, though slightly below the market's 28.6%. The company trades at a significant discount of 44.2% below estimated fair value, with analysts predicting a price rise of 41.4%. Recently, APR announced a KRW60 billion share repurchase program aimed at stabilizing stock price and enhancing shareholder value.

- Dive into the specifics of APR here with our thorough growth forecast report.

- Our comprehensive valuation report raises the possibility that APR is priced lower than what may be justified by its financials.

Key Takeaways

- Click through to start exploring the rest of the 86 Fast Growing KRX Companies With High Insider Ownership now.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About KOSE:A003230

Samyang Foods

Engages in the food business in South Korea and internationally.

Outstanding track record with excellent balance sheet.