- China

- /

- Communications

- /

- SZSE:301600

3 Growth Companies With High Insider Ownership And Up To 31% Earnings Growth

Reviewed by Simply Wall St

As global markets navigate a complex landscape of economic shifts, including rate cuts by the ECB and SNB and expectations for a Fed cut, investors are witnessing mixed performances across major indices. In this environment, growth stocks have continued to outpace value stocks, with the Nasdaq Composite reaching new heights despite broader market declines. Amidst these conditions, companies with high insider ownership can be particularly appealing as they often signal strong confidence from those closest to the business.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| Archean Chemical Industries (NSEI:ACI) | 22.9% | 41.3% |

| Seojin SystemLtd (KOSDAQ:A178320) | 30.9% | 39.9% |

| Propel Holdings (TSX:PRL) | 36.9% | 37.6% |

| Medley (TSE:4480) | 34% | 31.7% |

| Laopu Gold (SEHK:6181) | 36.4% | 34.2% |

| Pharma Mar (BME:PHM) | 11.8% | 56.2% |

| Plenti Group (ASX:PLT) | 12.8% | 120.1% |

| Brightstar Resources (ASX:BTR) | 16.2% | 84.5% |

| Fine M-TecLTD (KOSDAQ:A441270) | 17.2% | 131.1% |

| Credo Technology Group Holding (NasdaqGS:CRDO) | 13.5% | 65.9% |

Let's take a closer look at a couple of our picks from the screened companies.

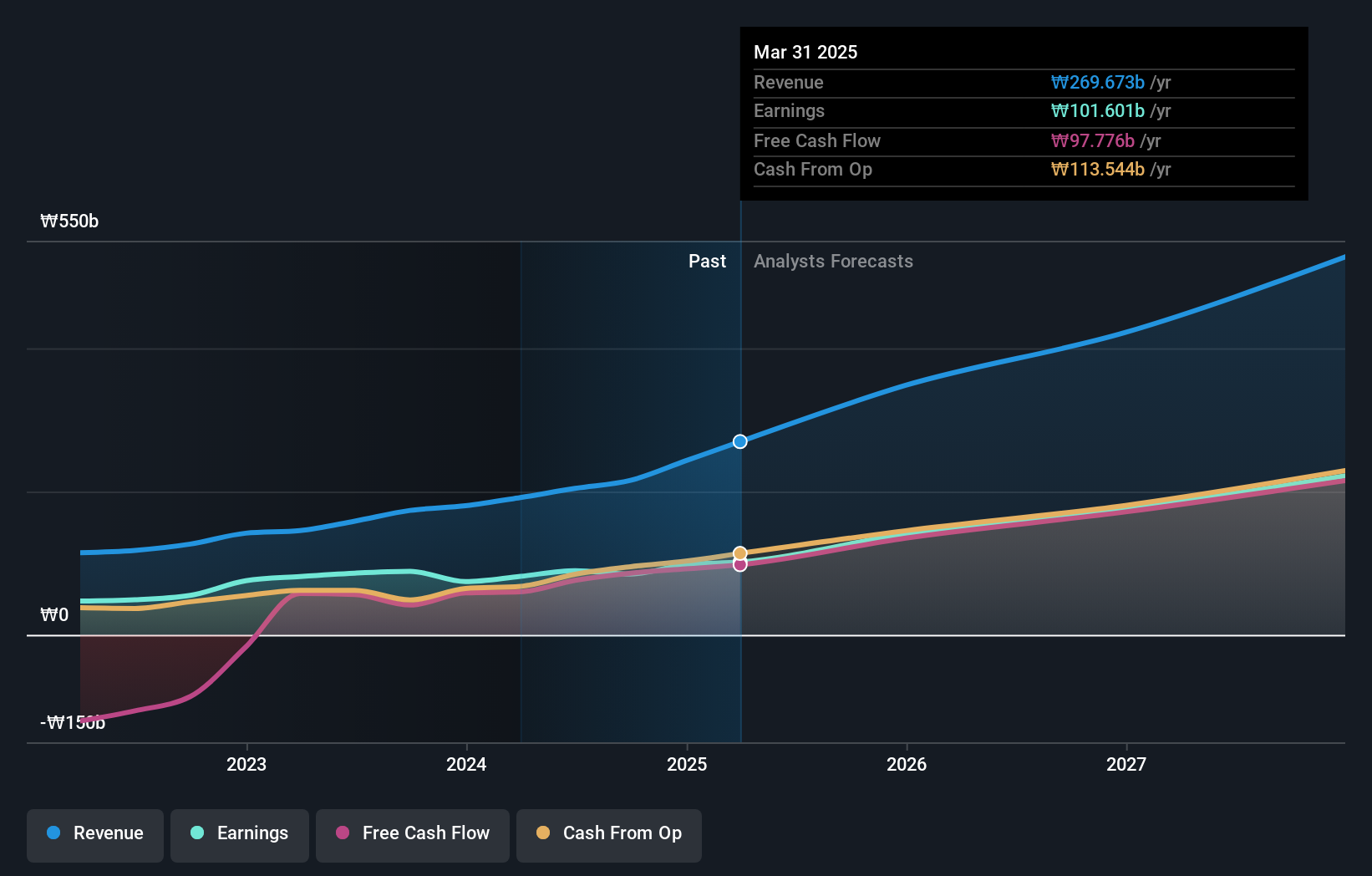

CLASSYS (KOSDAQ:A214150)

Simply Wall St Growth Rating: ★★★★★☆

Overview: CLASSYS Inc. is a global provider of medical aesthetics devices, with a market cap of ₩3.12 trillion.

Operations: The company generates revenue primarily from its Surgical & Medical Equipment segment, amounting to ₩215.54 billion.

Insider Ownership: 13.7%

Earnings Growth Forecast: 28.1% p.a.

CLASSYS Inc. is poised for growth with forecasted earnings and revenue increases of 28.11% and 25.5% annually, respectively, outpacing the broader Korean market in revenue growth. The company recently announced a KRW 25 billion share repurchase program to enhance shareholder value, which may stabilize stock prices. Despite past shareholder dilution, CLASSYS trades below its estimated fair value and analyst price targets suggest potential upside of 38.4%.

- Take a closer look at CLASSYS' potential here in our earnings growth report.

- In light of our recent valuation report, it seems possible that CLASSYS is trading behind its estimated value.

Quectel Wireless Solutions (SHSE:603236)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Quectel Wireless Solutions Co., Ltd. is involved in the research, design, production, and sales of wireless communication modules and solutions globally, with a market cap of CN¥16.19 billion.

Operations: Quectel Wireless Solutions Co., Ltd. generates revenue through the development, manufacturing, and distribution of wireless communication modules and solutions on a global scale.

Insider Ownership: 23.3%

Earnings Growth Forecast: 31.6% p.a.

Quectel Wireless Solutions shows promising growth potential, with earnings expected to rise significantly at 31.6% annually, surpassing the Chinese market's average. Recent product launches, including advanced IoT modules and antennas, highlight its innovative edge in connectivity solutions. Despite trading well below estimated fair value, Quectel maintains a solid position within the industry. The company's revenue is anticipated to grow at 19% per year. However, insider trading activity remains minimal over the past three months.

- Click to explore a detailed breakdown of our findings in Quectel Wireless Solutions' earnings growth report.

- The valuation report we've compiled suggests that Quectel Wireless Solutions' current price could be quite moderate.

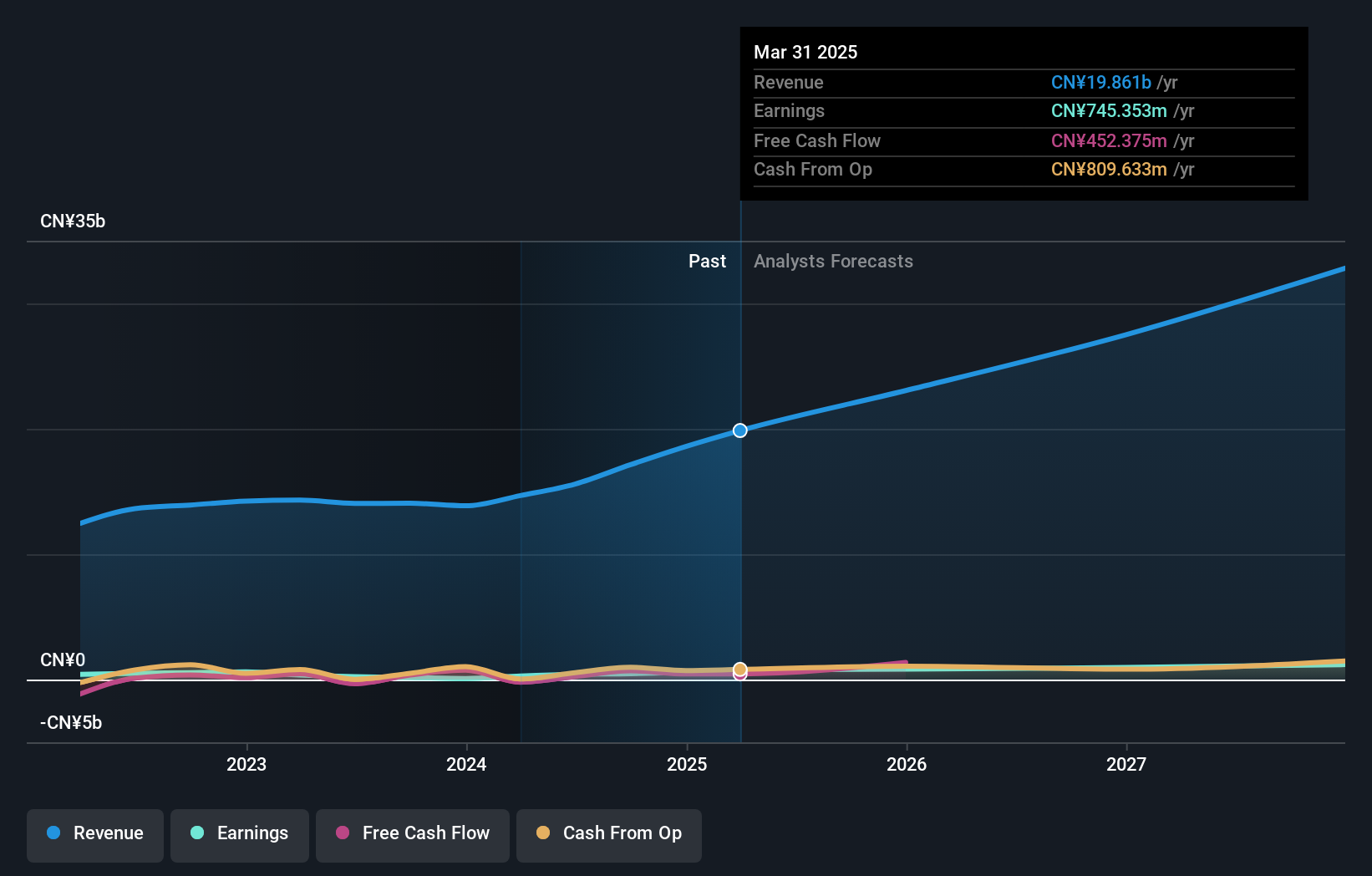

Flaircomm Microelectronics (SZSE:301600)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Flaircomm Microelectronics, Inc. develops and sells wireless communication modules, embedded software, and turnkey system solutions for automotive and M2M applications in China with a market cap of CN¥8.91 billion.

Operations: The company's revenue from Wireless Communications Equipment is CN¥995.17 million.

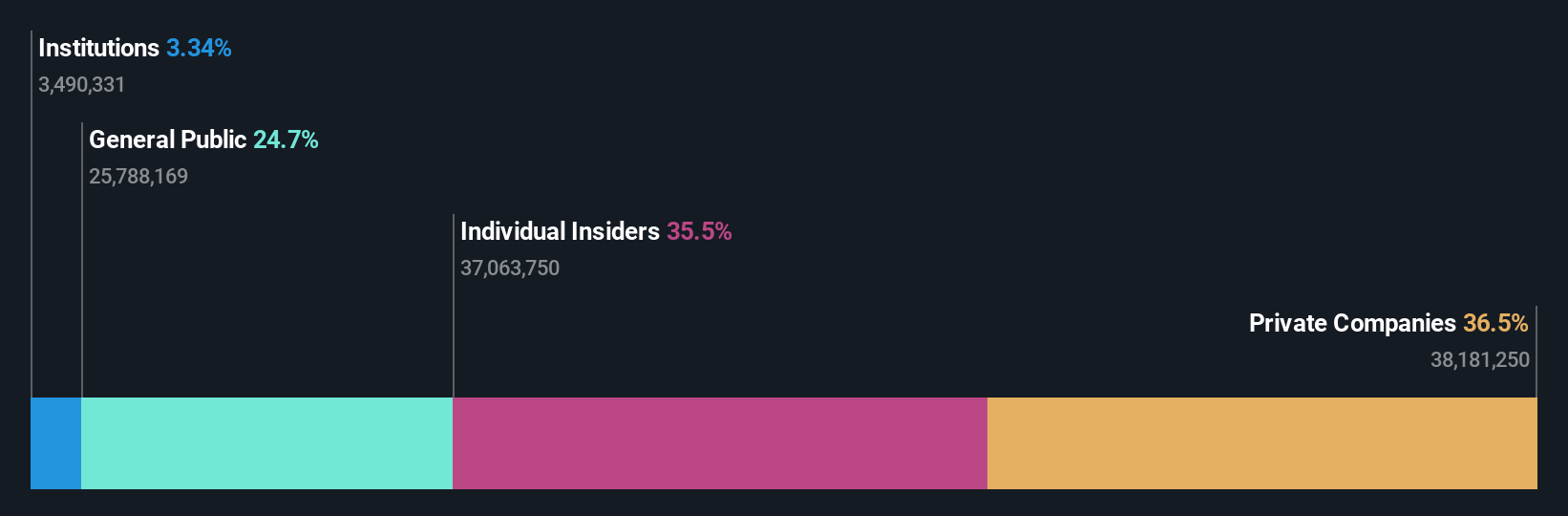

Insider Ownership: 35.5%

Earnings Growth Forecast: 28.0% p.a.

Flaircomm Microelectronics demonstrates strong growth potential, with earnings expected to grow significantly at 28% annually, outpacing the Chinese market. Revenue is also forecasted to rise by 22.5% per year. Recent results show sales increased to CNY 734.85 million and net income rose to CNY 134.87 million over nine months. Despite a high price-to-earnings ratio of 52.6x, it remains below the industry average, while insider trading activity has been minimal recently.

- Click here to discover the nuances of Flaircomm Microelectronics with our detailed analytical future growth report.

- The valuation report we've compiled suggests that Flaircomm Microelectronics' current price could be inflated.

Summing It All Up

- Take a closer look at our Fast Growing Companies With High Insider Ownership list of 1522 companies by clicking here.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:301600

Flaircomm Microelectronics

Develops and sells wireless communication modules, embedded software, and turnkey system solutions for automotive and M2M applications in China.

Flawless balance sheet with high growth potential.