Advertisement

- South Korea

- /

- Consumer Services

- /

- KOSDAQ:A440320

We Don’t Think OpenknowlLtd's (KOSDAQ:440320) Earnings Should Make Shareholders Too Comfortable

Openknowl Co.,Ltd. (KOSDAQ:440320) posted some decent earnings, but shareholders didn't react strongly. Our analysis has found some concerning factors which weaken the profit's foundation.

See our latest analysis for OpenknowlLtd

Zooming In On OpenknowlLtd's Earnings

Many investors haven't heard of the accrual ratio from cashflow, but it is actually a useful measure of how well a company's profit is backed up by free cash flow (FCF) during a given period. In plain english, this ratio subtracts FCF from net profit, and divides that number by the company's average operating assets over that period. The ratio shows us how much a company's profit exceeds its FCF.

Therefore, it's actually considered a good thing when a company has a negative accrual ratio, but a bad thing if its accrual ratio is positive. While it's not a problem to have a positive accrual ratio, indicating a certain level of non-cash profits, a high accrual ratio is arguably a bad thing, because it indicates paper profits are not matched by cash flow. That's because some academic studies have suggested that high accruals ratios tend to lead to lower profit or less profit growth.

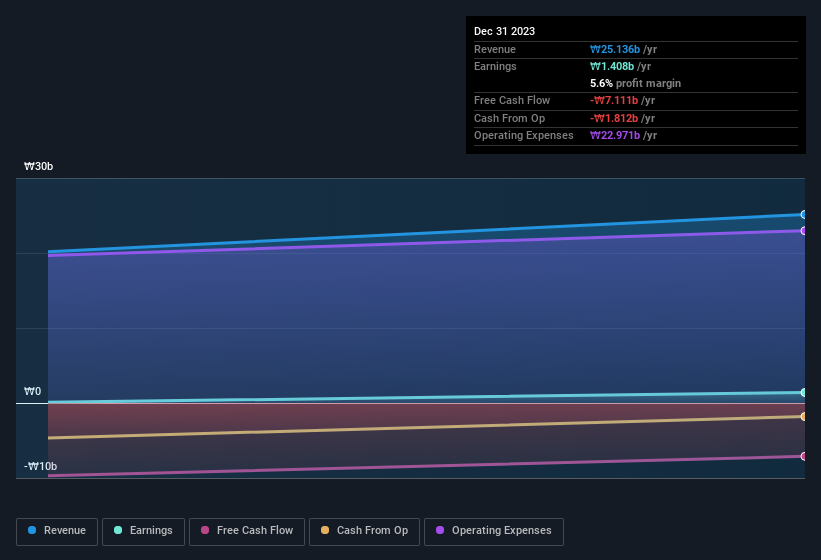

For the year to December 2023, OpenknowlLtd had an accrual ratio of 0.69. As a general rule, that bodes poorly for future profitability. And indeed, during the period the company didn't produce any free cash flow whatsoever. Even though it reported a profit of ₩1.41b, a look at free cash flow indicates it actually burnt through ₩7.1b in the last year. Unfortunately, we don't have data on OpenknowlLtd's free cash flow for the prior year; that's not necessarily a bad thing, though we do generally prefer to be able to see a bit of a company's history. However, that's not all there is to consider. We can see that unusual items have impacted its statutory profit, and therefore the accrual ratio.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of OpenknowlLtd.

How Do Unusual Items Influence Profit?

Given the accrual ratio, it's not overly surprising that OpenknowlLtd's profit was boosted by unusual items worth ₩177m in the last twelve months. While we like to see profit increases, we tend to be a little more cautious when unusual items have made a big contribution. When we crunched the numbers on thousands of publicly listed companies, we found that a boost from unusual items in a given year is often not repeated the next year. Which is hardly surprising, given the name. Assuming those unusual items don't show up again in the current year, we'd thus expect profit to be weaker next year (in the absence of business growth, that is).

Our Take On OpenknowlLtd's Profit Performance

OpenknowlLtd had a weak accrual ratio, but its profit did receive a boost from unusual items. Considering all this we'd argue OpenknowlLtd's profits probably give an overly generous impression of its sustainable level of profitability. With this in mind, we wouldn't consider investing in a stock unless we had a thorough understanding of the risks. Our analysis shows 4 warning signs for OpenknowlLtd (1 is a bit concerning!) and we strongly recommend you look at these before investing.

Our examination of OpenknowlLtd has focussed on certain factors that can make its earnings look better than they are. And, on that basis, we are somewhat skeptical. But there are plenty of other ways to inform your opinion of a company. Some people consider a high return on equity to be a good sign of a quality business. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSDAQ:A440320

OpenknowlLtd

Engages in the planning, developing, operating, and selling a number of camps and mentoring programs.

Adequate balance sheet and slightly overvalued.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.4% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.0% undervalued

EA

Community Contributor