Advertisement

- South Korea

- /

- Consumer Durables

- /

- KOSE:A021240

COWAY Co., Ltd.'s (KRX:021240) Stock Has Been Sliding But Fundamentals Look Strong: Is The Market Wrong?

It is hard to get excited after looking at COWAY's (KRX:021240) recent performance, when its stock has declined 11% over the past three months. However, a closer look at its sound financials might cause you to think again. Given that fundamentals usually drive long-term market outcomes, the company is worth looking at. In this article, we decided to focus on COWAY's ROE.

Return on equity or ROE is a key measure used to assess how efficiently a company's management is utilizing the company's capital. Put another way, it reveals the company's success at turning shareholder investments into profits.

View our latest analysis for COWAY

How Do You Calculate Return On Equity?

ROE can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for COWAY is:

25% = ₩357b ÷ ₩1.4t (Based on the trailing twelve months to September 2020).

The 'return' is the income the business earned over the last year. One way to conceptualize this is that for each ₩1 of shareholders' capital it has, the company made ₩0.25 in profit.

What Is The Relationship Between ROE And Earnings Growth?

Thus far, we have learned that ROE measures how efficiently a company is generating its profits. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Assuming everything else remains unchanged, the higher the ROE and profit retention, the higher the growth rate of a company compared to companies that don't necessarily bear these characteristics.

COWAY's Earnings Growth And 25% ROE

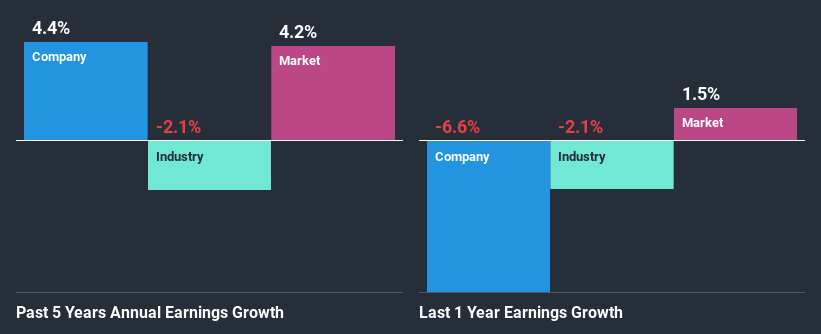

To begin with, COWAY has a pretty high ROE which is interesting. Second, a comparison with the average ROE reported by the industry of 6.6% also doesn't go unnoticed by us. Yet, COWAY has posted measly growth of 4.4% over the past five years. This is generally not the case as when a company has a high rate of return it should usually also have a high earnings growth rate. We reckon that a low growth, when returns are quite high could be the result of certain circumstances like low earnings retention or or poor allocation of capital.

Next, on comparing with the industry net income growth, we found that the growth figure reported by COWAY compares quite favourably to the industry average, which shows a decline of 2.1% in the same period.

Earnings growth is a huge factor in stock valuation. It’s important for an investor to know whether the market has priced in the company's expected earnings growth (or decline). This then helps them determine if the stock is placed for a bright or bleak future. Is A021240 fairly valued? This infographic on the company's intrinsic value has everything you need to know.

Is COWAY Making Efficient Use Of Its Profits?

While the company did pay out a portion of its dividend in the past, it currently doesn't pay a dividend. We infer that the company has been reinvesting all of its profits to grow its business.

Existing analyst estimates suggest that the company's future payout ratio is expected to drop to 21% over the next three years. Despite the lower expected payout ratio, the company's ROE is not expected to change by much.

Conclusion

Overall, we are quite pleased with COWAY's performance. We are particularly impressed by the considerable earnings growth posted by the company, which was likely backed by its high ROE. While the company is paying out most of its earnings as dividends, it has been able to grow its earnings in spite of it, so that's probably a good sign. That being so, the latest analyst forecasts show that the company will continue to see an expansion in its earnings. To know more about the latest analysts predictions for the company, check out this visualization of analyst forecasts for the company.

If you decide to trade COWAY, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About KOSE:A021240

COWAY

Engages in the production and sale of environmental home appliances in South Korea and internationally.

Proven track record with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Quality at a Premium. A time to watch, not to buy?

Fair Value US$154.56|29.3% undervalued

DA

Community Contributor

GRAB: The Super-App at the Heart of Southeast Asia’s Digital Boom

Fair Value US$6.60|7.0% undervalued

BL

Community Contributor

Verve Group to Surge with 51.61% Revenue Growth

Fair Value €6.00|65.0% undervalued

ME

Community Contributor