Advertisement

- South Korea

- /

- Machinery

- /

- KOSE:A329180

We Like These Underlying Return On Capital Trends At HD Hyundai Heavy IndustriesLtd (KRX:329180)

If you're not sure where to start when looking for the next multi-bagger, there are a few key trends you should keep an eye out for. Typically, we'll want to notice a trend of growing return on capital employed (ROCE) and alongside that, an expanding base of capital employed. Put simply, these types of businesses are compounding machines, meaning they are continually reinvesting their earnings at ever-higher rates of return. So when we looked at HD Hyundai Heavy IndustriesLtd (KRX:329180) and its trend of ROCE, we really liked what we saw.

Understanding Return On Capital Employed (ROCE)

Just to clarify if you're unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. The formula for this calculation on HD Hyundai Heavy IndustriesLtd is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

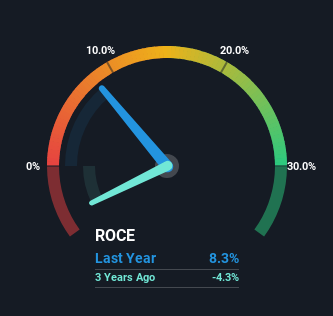

0.083 = ₩555b ÷ (₩17t - ₩10t) (Based on the trailing twelve months to September 2024).

Thus, HD Hyundai Heavy IndustriesLtd has an ROCE of 8.3%. In absolute terms, that's a low return, but it's much better than the Machinery industry average of 6.7%.

See our latest analysis for HD Hyundai Heavy IndustriesLtd

Above you can see how the current ROCE for HD Hyundai Heavy IndustriesLtd compares to its prior returns on capital, but there's only so much you can tell from the past. If you're interested, you can view the analysts predictions in our free analyst report for HD Hyundai Heavy IndustriesLtd .

So How Is HD Hyundai Heavy IndustriesLtd's ROCE Trending?

We're delighted to see that HD Hyundai Heavy IndustriesLtd is reaping rewards from its investments and has now broken into profitability. The company was generating losses three years ago, but now it's turned around, earning 8.3% which is no doubt a relief for some early shareholders. Additionally, the business is utilizing 26% less capital than it was three years ago, and taken at face value, that can mean the company needs less funds at work to get a return. This could potentially mean that the company is selling some of its assets.

On a side note, we noticed that the improvement in ROCE appears to be partly fueled by an increase in current liabilities. The current liabilities has increased to 61% of total assets, so the business is now more funded by the likes of its suppliers or short-term creditors. Given it's pretty high ratio, we'd remind investors that having current liabilities at those levels can bring about some risks in certain businesses.

The Key Takeaway

In the end, HD Hyundai Heavy IndustriesLtd has proven it's capital allocation skills are good with those higher returns from less amount of capital. And a remarkable 186% total return over the last three years tells us that investors are expecting more good things to come in the future. So given the stock has proven it has promising trends, it's worth researching the company further to see if these trends are likely to persist.

On the other side of ROCE, we have to consider valuation. That's why we have a FREE intrinsic value estimation for A329180 on our platform that is definitely worth checking out.

If you want to search for solid companies with great earnings, check out this free list of companies with good balance sheets and impressive returns on equity.

Valuation is complex, but we're here to simplify it.

Discover if HD Hyundai Heavy IndustriesLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSE:A329180

HD Hyundai Heavy IndustriesLtd

Engages in operating shipbuilding and offshore, naval and special ships, and engine and machinery business units worldwide.

Solid track record with reasonable growth potential.

Market Insights

Advertisement

Community Narratives

The Most Undervalued of the Magnificent 7

Fair Value US$237.43|36.3% undervalued

IN

Community Contributor

PVA TePla's New Strategy Aims for 22% Revenue Growth in Semiconductor Recovery

Fair Value €19.19|20.8% undervalued

MI

Community Contributor