Advertisement

- South Korea

- /

- Machinery

- /

- KOSE:A145210

Dynamic Design (KRX:145210) Has Debt But No Earnings; Should You Worry?

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We note that Dynamic Design Co., LTD. (KRX:145210) does have debt on its balance sheet. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we examine debt levels, we first consider both cash and debt levels, together.

Check out our latest analysis for Dynamic Design

How Much Debt Does Dynamic Design Carry?

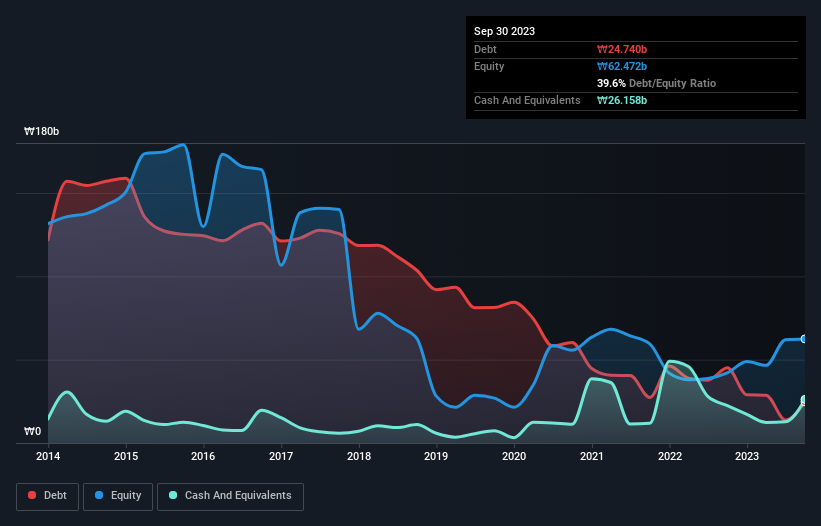

As you can see below, Dynamic Design had ₩24.7b of debt at September 2023, down from ₩45.1b a year prior. But it also has ₩26.2b in cash to offset that, meaning it has ₩1.42b net cash.

How Strong Is Dynamic Design's Balance Sheet?

According to the last reported balance sheet, Dynamic Design had liabilities of ₩34.1b due within 12 months, and liabilities of ₩8.94b due beyond 12 months. Offsetting this, it had ₩26.2b in cash and ₩21.5b in receivables that were due within 12 months. So it actually has ₩4.64b more liquid assets than total liabilities.

This short term liquidity is a sign that Dynamic Design could probably pay off its debt with ease, as its balance sheet is far from stretched. Simply put, the fact that Dynamic Design has more cash than debt is arguably a good indication that it can manage its debt safely. When analysing debt levels, the balance sheet is the obvious place to start. But it is Dynamic Design's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

In the last year Dynamic Design wasn't profitable at an EBIT level, but managed to grow its revenue by 31%, to ₩71b. With any luck the company will be able to grow its way to profitability.

So How Risky Is Dynamic Design?

We have no doubt that loss making companies are, in general, riskier than profitable ones. And in the last year Dynamic Design had an earnings before interest and tax (EBIT) loss, truth be told. Indeed, in that time it burnt through ₩12b of cash and made a loss of ₩73b. But at least it has ₩1.42b on the balance sheet to spend on growth, near-term. With very solid revenue growth in the last year, Dynamic Design may be on a path to profitability. Pre-profit companies are often risky, but they can also offer great rewards. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. These risks can be hard to spot. Every company has them, and we've spotted 4 warning signs for Dynamic Design (of which 1 is a bit unpleasant!) you should know about.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSE:A145210

Dynamic Design

Primarily engages in the manufacture and sale of tire molds forming machines in Korea, China, the Americas, Europe, and Indonesia.

Mediocre balance sheet with very low risk.

Market Insights

Advertisement

Community Narratives

America Wants Homegrown Drones — Draganfly Is Ready to Deliver

Fair Value US$9.21|32.6% undervalued

JO

Community Contributor

Cheesecake Factory offers an enticing opportunity for long-term growth by leveraging new concepts

Fair Value US$73.83|25.6% undervalued

ZW

Community Contributor

Coca-Cola’s Intrinsic Value Set to Rise with Fed Rate Cut

Fair Value US$67.50|1.6% undervalued

AL

Community Contributor

Fully Permitted Gold Mine with 50 Baggers Potential

Fair Value CA$41.00|98.2% undervalued

RO

Community Contributor