Advertisement

- South Korea

- /

- Machinery

- /

- KOSE:A064350

Hyundai Rotem (KRX:064350) Is Experiencing Growth In Returns On Capital

There are a few key trends to look for if we want to identify the next multi-bagger. Amongst other things, we'll want to see two things; firstly, a growing return on capital employed (ROCE) and secondly, an expansion in the company's amount of capital employed. Basically this means that a company has profitable initiatives that it can continue to reinvest in, which is a trait of a compounding machine. So on that note, Hyundai Rotem (KRX:064350) looks quite promising in regards to its trends of return on capital.

Understanding Return On Capital Employed (ROCE)

Just to clarify if you're unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. The formula for this calculation on Hyundai Rotem is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

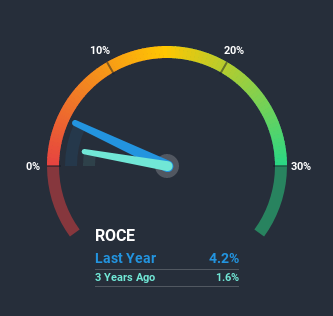

0.042 = ₩82b ÷ (₩4.2t - ₩2.2t) (Based on the trailing twelve months to December 2020).

Thus, Hyundai Rotem has an ROCE of 4.2%. In absolute terms, that's a low return and it also under-performs the Machinery industry average of 5.3%.

See our latest analysis for Hyundai Rotem

In the above chart we have measured Hyundai Rotem's prior ROCE against its prior performance, but the future is arguably more important. If you'd like to see what analysts are forecasting going forward, you should check out our free report for Hyundai Rotem.

The Trend Of ROCE

It's great to see that Hyundai Rotem has started to generate some pre-tax earnings from prior investments. The company was generating losses five years ago, but now it's turned around, earning 4.2% which is no doubt a relief for some early shareholders. Additionally, the business is utilizing 36% less capital than it was five years ago, and taken at face value, that can mean the company needs less funds at work to get a return. Hyundai Rotem could be selling under-performing assets since the ROCE is improving.

On a side note, we noticed that the improvement in ROCE appears to be partly fueled by an increase in current liabilities. Essentially the business now has suppliers or short-term creditors funding about 53% of its operations, which isn't ideal. And with current liabilities at those levels, that's pretty high.

The Bottom Line

In a nutshell, we're pleased to see that Hyundai Rotem has been able to generate higher returns from less capital. Considering the stock has delivered 10% to its stockholders over the last five years, it may be fair to think that investors aren't fully aware of the promising trends yet. So exploring more about this stock could uncover a good opportunity, if the valuation and other metrics stack up.

Hyundai Rotem does come with some risks though, we found 3 warning signs in our investment analysis, and 1 of those makes us a bit uncomfortable...

While Hyundai Rotem may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

If you’re looking to trade Hyundai Rotem, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Hyundai Rotem might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KOSE:A064350

Hyundai Rotem

Manufactures and sells railway vehicles, defense systems, and plants and machinery in South Korea and internationally.

Outstanding track record with flawless balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Enterprise, AI & Cloud Growth Ahead, Waiting For the Right Price 💸

Fair Value US$204.74|5.4% overvalued

FR

Community Contributor

Good foundation, but now it's all about the next steps

Fair Value US$147.87|28.9% undervalued

TO

Community Contributor

XTB's Path to 100–120 PLN by 2028 Amid Market Volatility

Fair Value zł100.96|36.6% undervalued

DZ

Community Contributor