- South Korea

- /

- Electrical

- /

- KOSE:A034020

Improved Revenues Required Before Doosan Enerbility Co., Ltd. (KRX:034020) Stock's 31% Jump Looks Justified

Doosan Enerbility Co., Ltd. (KRX:034020) shareholders have had their patience rewarded with a 31% share price jump in the last month. The last 30 days bring the annual gain to a very sharp 33%.

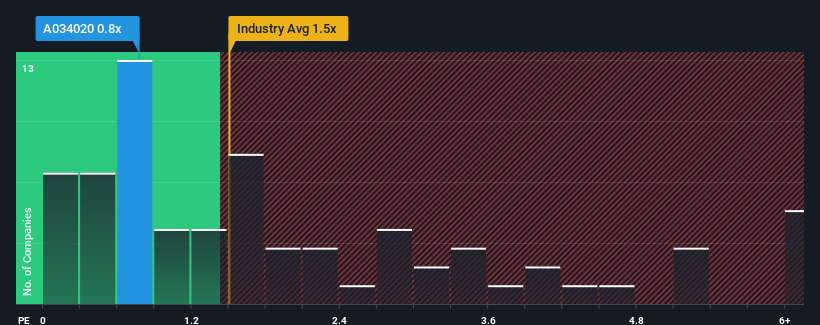

In spite of the firm bounce in price, it would still be understandable if you think Doosan Enerbility is a stock with good investment prospects with a price-to-sales ratios (or "P/S") of 0.8x, considering almost half the companies in Korea's Electrical industry have P/S ratios above 1.5x. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's limited.

View our latest analysis for Doosan Enerbility

What Does Doosan Enerbility's Recent Performance Look Like?

Doosan Enerbility could be doing better as it's been growing revenue less than most other companies lately. Perhaps the market is expecting the current trend of poor revenue growth to continue, which has kept the P/S suppressed. If you still like the company, you'd be hoping revenue doesn't get any worse and that you could pick up some stock while it's out of favour.

Want the full picture on analyst estimates for the company? Then our free report on Doosan Enerbility will help you uncover what's on the horizon.Is There Any Revenue Growth Forecasted For Doosan Enerbility?

The only time you'd be truly comfortable seeing a P/S as low as Doosan Enerbility's is when the company's growth is on track to lag the industry.

Retrospectively, the last year delivered a decent 7.2% gain to the company's revenues. This was backed up an excellent period prior to see revenue up by 105% in total over the last three years. Therefore, it's fair to say the revenue growth recently has been superb for the company.

Turning to the outlook, the next year should bring diminished returns, with revenue decreasing 5.2% as estimated by the four analysts watching the company. Meanwhile, the broader industry is forecast to expand by 5.3%, which paints a poor picture.

In light of this, it's understandable that Doosan Enerbility's P/S would sit below the majority of other companies. Nonetheless, there's no guarantee the P/S has reached a floor yet with revenue going in reverse. There's potential for the P/S to fall to even lower levels if the company doesn't improve its top-line growth.

The Bottom Line On Doosan Enerbility's P/S

Doosan Enerbility's stock price has surged recently, but its but its P/S still remains modest. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

As we suspected, our examination of Doosan Enerbility's analyst forecasts revealed that its outlook for shrinking revenue is contributing to its low P/S. Right now shareholders are accepting the low P/S as they concede future revenue probably won't provide any pleasant surprises. Unless there's material change, it's hard to envision a situation where the stock price will rise drastically.

You always need to take note of risks, for example - Doosan Enerbility has 1 warning sign we think you should be aware of.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

If you're looking to trade Doosan Enerbility, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSE:A034020

Very undervalued with excellent balance sheet.

Similar Companies

Market Insights

Community Narratives