Advertisement

- South Korea

- /

- Industrials

- /

- KOSE:A001040

Don't Race Out To Buy CJ Corporation (KRX:001040) Just Because It's Going Ex-Dividend

Regular readers will know that we love our dividends at Simply Wall St, which is why it's exciting to see CJ Corporation (KRX:001040) is about to trade ex-dividend in the next 3 days. Typically, the ex-dividend date is two business days before the record date, which is the date on which a company determines the shareholders eligible to receive a dividend. The ex-dividend date is important as the process of settlement involves at least two full business days. So if you miss that date, you would not show up on the company's books on the record date. In other words, investors can purchase CJ's shares before the 3rd of April in order to be eligible for the dividend, which will be paid on the 1st of January.

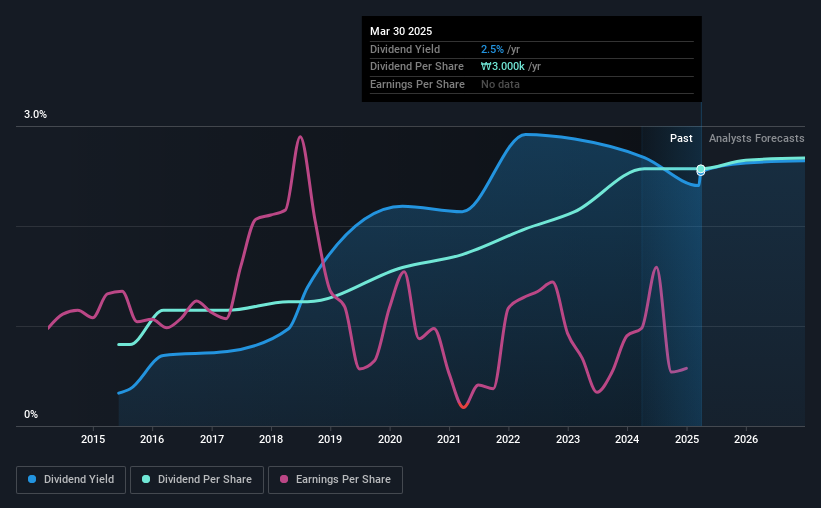

The company's next dividend payment will be ₩3000.00 per share, and in the last 12 months, the company paid a total of ₩3,000 per share. Based on the last year's worth of payments, CJ stock has a trailing yield of around 2.5% on the current share price of ₩117900.00. If you buy this business for its dividend, you should have an idea of whether CJ's dividend is reliable and sustainable. As a result, readers should always check whether CJ has been able to grow its dividends, or if the dividend might be cut.

If a company pays out more in dividends than it earned, then the dividend might become unsustainable - hardly an ideal situation. Last year, CJ paid out 100% of its income as dividends, which is above a level that we're comfortable with, especially if the company needs to reinvest in its business. That said, even highly profitable companies sometimes might not generate enough cash to pay the dividend, which is why we should always check if the dividend is covered by cash flow. Luckily it paid out just 12% of its free cash flow last year.

It's good to see that while CJ's dividends were not covered by profits, at least they are affordable from a cash perspective. If executives were to continue paying more in dividends than the company reported in profits, we'd view this as a warning sign. Extraordinarily few companies are capable of persistently paying a dividend that is greater than their profits.

See our latest analysis for CJ

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Businesses with shrinking earnings are tricky from a dividend perspective. If earnings decline and the company is forced to cut its dividend, investors could watch the value of their investment go up in smoke. With that in mind, we're discomforted by CJ's 18% per annum decline in earnings in the past five years. Such a sharp decline casts doubt on the future sustainability of the dividend.

Many investors will assess a company's dividend performance by evaluating how much the dividend payments have changed over time. CJ has delivered 12% dividend growth per year on average over the past 10 years. That's intriguing, but the combination of growing dividends despite declining earnings can typically only be achieved by paying out a larger percentage of profits. CJ is already paying out a high percentage of its income, so without earnings growth, we're doubtful of whether this dividend will grow much in the future.

Final Takeaway

Should investors buy CJ for the upcoming dividend? It's not a great combination to see a company with earnings in decline and paying out 100% of its profits, which could imply the dividend may be at risk of being cut in the future. Yet cashflow was much stronger, which makes us wonder if there are some large timing issues in CJ's cash flows, or perhaps the company has written down some assets aggressively, reducing its income. It's not an attractive combination from a dividend perspective, and we're inclined to pass on this one for the time being.

Although, if you're still interested in CJ and want to know more, you'll find it very useful to know what risks this stock faces. Every company has risks, and we've spotted 4 warning signs for CJ you should know about.

A common investing mistake is buying the first interesting stock you see. Here you can find a full list of high-yield dividend stocks.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSE:A001040

CJ

Engages in the food and food services, bio, logistics and retail, and entertainment and media businesses worldwide.

Adequate balance sheet average dividend payer.

Market Insights

Advertisement

Community Narratives

Rocket Lab USA Will Ignite a 30% Revenue Growth Journey

Fair Value US$31.72|41.3% undervalued

KI

Community Contributor

EasyJet weirdly unloved by investors in spite of relatively attractive metrics

Fair Value UK£6.95|33.9% undervalued

PI

Community Contributor

HEXPOL AB: Sustained Long Term Growth, Stable Margins, and Strategic M&A

Fair Value SEK 122.27|27.0% undervalued

MA

Community Contributor