Advertisement

- South Korea

- /

- Construction

- /

- KOSDAQ:A319400

Undiscovered Gems to Explore in January 2025

Simply Wall St

Reviewed by Simply Wall St

As we step into January 2025, the global markets are navigating a complex landscape marked by mixed performances across major indices and economic indicators. While U.S. equities wrapped up a strong year despite recent slumps, small-cap stocks have shown resilience with the S&P MidCap 400 and Russell 2000 posting gains, highlighting potential opportunities in less prominent sectors. In this environment, identifying promising stocks involves looking for companies that can thrive amidst economic uncertainties and capitalize on emerging trends within their industries.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Omega Flex | NA | 0.39% | 2.57% | ★★★★★★ |

| Wilson Bank Holding | NA | 7.87% | 8.22% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Parker Drilling | 46.05% | 0.86% | 52.25% | ★★★★★★ |

| Teekay | NA | -3.71% | 60.91% | ★★★★★★ |

| Aesler Grup Internasional | NA | -17.61% | -40.21% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| Pure Cycle | 5.31% | -4.44% | -5.74% | ★★★★★☆ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

| Practic | NA | 3.63% | 6.85% | ★★★★☆☆ |

We're going to check out a few of the best picks from our screener tool.

Baskent Dogalgaz Dagitim Gayrimenkul Yatirim Ortakligi (IBSE:BASGZ)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Baskent Dogalgaz Dagitim Gayrimenkul Yatirim Ortakligi A.S. operates in the natural gas distribution sector and has a market capitalization of TRY21.76 billion.

Operations: Baskent Dogalgaz generates revenue primarily through natural gas sales, amounting to TRY21.61 billion. The company's financial performance can be assessed by examining its net profit margin, which provides insight into its profitability relative to total revenue.

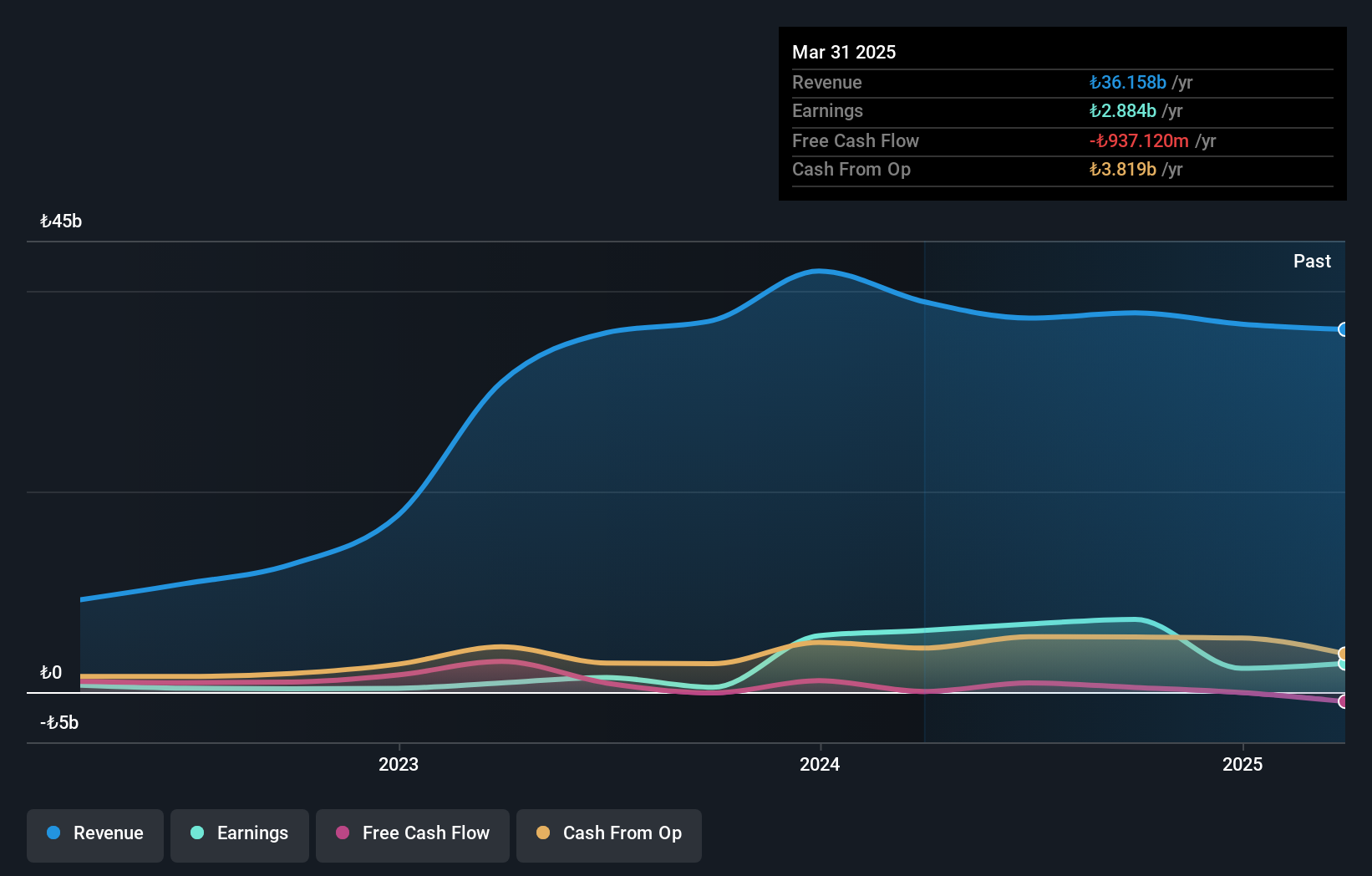

Baskent Dogalgaz Dagitim Gayrimenkul Yatirim Ortakligi, with its notable earnings growth of 1004.3% over the past year, seems to be outperforming the Gas Utilities industry. Trading at 76.2% below its estimated fair value, it presents a compelling valuation scenario. The company's debt-to-equity ratio has impressively reduced from 32.3% to 9.9% over five years, indicating prudent financial management. Recent results show third-quarter sales of TRY 4,334 million and a net loss improvement to TRY 611 million from TRY 1,077 million last year. Despite challenges in net income figures for nine months at TRY 1,436 million compared to TRY 116 million previously reflect significant recovery potential in this sector.

HYUNDAI MOVEX (KOSDAQ:A319400)

Simply Wall St Value Rating: ★★★★★★

Overview: HYUNDAI MOVEX Co., Ltd. engages in the IT and logistics system sectors both domestically and internationally, with a market cap of ₩459.19 billion.

Operations: HYUNDAI MOVEX generates revenue through its operations in the IT and logistics system sectors. The company's market capitalization is ₩459.19 billion.

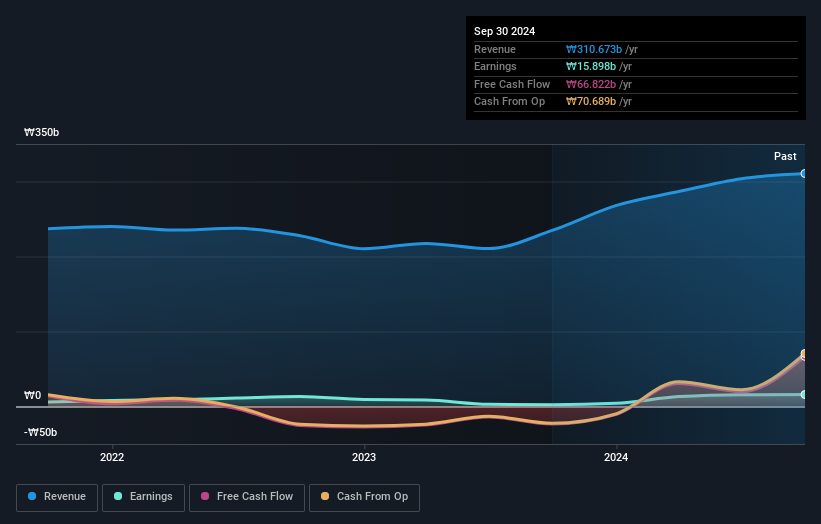

Hyundai Movex has caught attention with its impressive earnings growth of 607% over the past year, outpacing the construction industry's 12%. The company is debt-free, a significant improvement from five years ago when it had a debt-to-equity ratio of 29%. Trading at 95.5% below its estimated fair value, Hyundai Movex seems undervalued. The recent share repurchase program worth KRW 25 billion aims to enhance shareholder value, reflecting confidence in future prospects. With high-quality earnings and positive free cash flow, this small cap entity offers an intriguing mix of potential growth and solid financial health.

- Get an in-depth perspective on HYUNDAI MOVEX's performance by reading our health report here.

Examine HYUNDAI MOVEX's past performance report to understand how it has performed in the past.

Sino-Platinum MetalsLtd (SHSE:600459)

Simply Wall St Value Rating: ★★★★★☆

Overview: Sino-Platinum Metals Co., Ltd operates in China, focusing on the research, development, production, sales, and technical services of metal and non-metal materials with a market capitalization of approximately CN¥10.34 billion.

Operations: Sino-Platinum Metals Co., Ltd generates revenue primarily from its Metal Processors and Fabrication segment, which accounts for CN¥46.97 billion. The company's financial performance is characterized by a focus on this significant revenue stream.

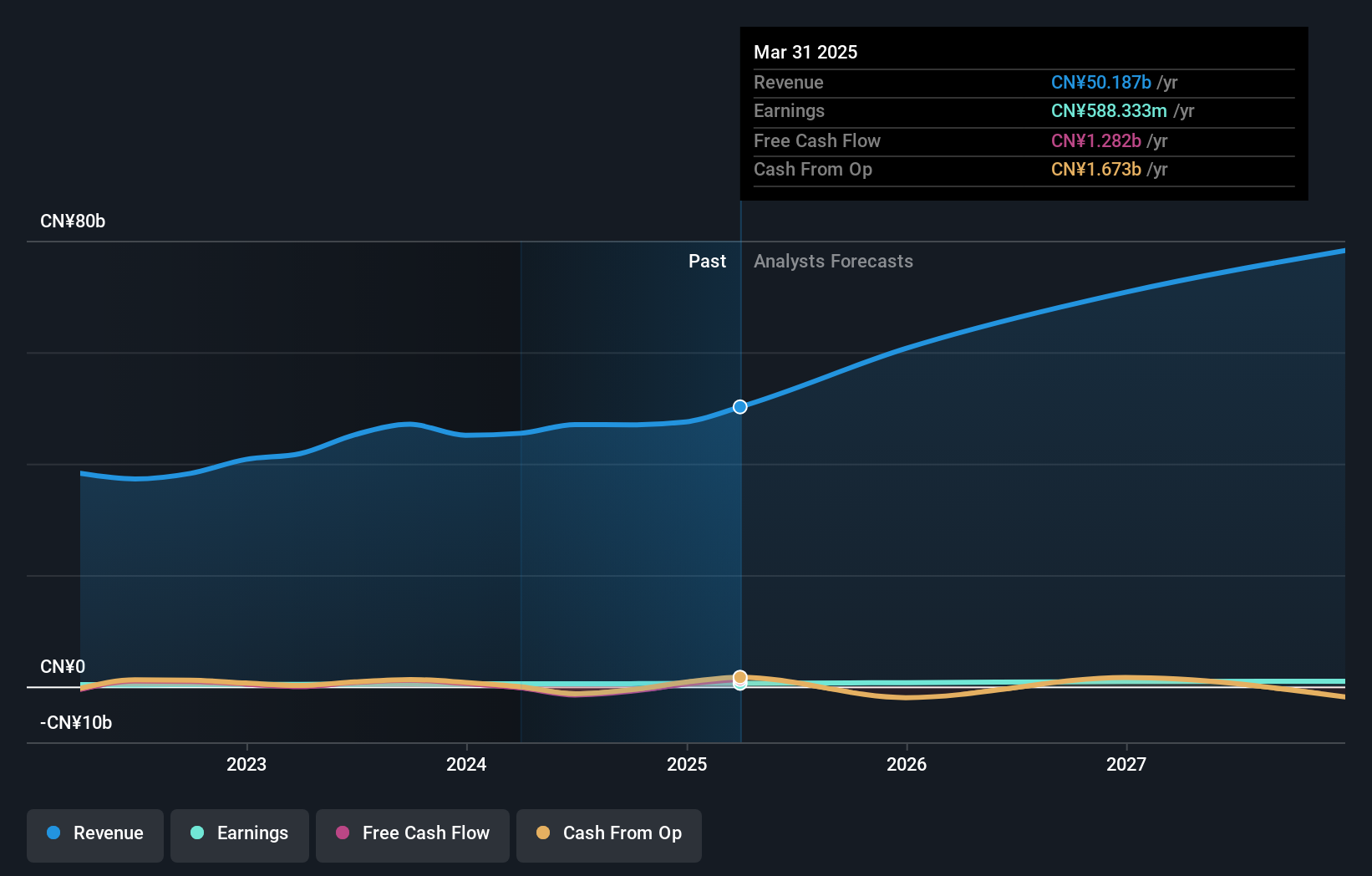

Sino-Platinum Metals, a relatively small player in the metals and mining sector, has shown resilience with earnings growth of 6% over the past year, outpacing the industry average of -2.3%. The company's debt to equity ratio improved from 69.5% to 60.1% over five years, indicating prudent financial management. Trading at a price-to-earnings ratio of 20.2x compared to the CN market's 33.2x suggests it's attractively valued against peers. However, high-quality earnings were affected by a one-off gain of CN¥212 million in recent results, which could skew perceptions of its performance sustainability moving forward.

Turning Ideas Into Actions

- Explore the 4650 names from our Undiscovered Gems With Strong Fundamentals screener here.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if HYUNDAI MOVEX might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About KOSDAQ:A319400

HYUNDAI MOVEX

Operates in the information technology (IT) and logistics system businesses in South Korea and internationally.

Flawless balance sheet with proven track record.

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|26.3% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|4.8% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor