- China

- /

- Electrical

- /

- SZSE:300438

3 Growth Companies With High Insider Ownership Expecting Up To 41% Revenue Growth

Reviewed by Simply Wall St

As global markets navigate a landscape marked by rising inflation and record-high U.S. stock indexes, growth stocks have continued to outperform value shares, capturing investor interest. In this environment, companies with high insider ownership can be particularly appealing as they often signal strong internal confidence in future prospects.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| Seojin SystemLtd (KOSDAQ:A178320) | 32.1% | 39.9% |

| Clinuvel Pharmaceuticals (ASX:CUV) | 10.4% | 26.2% |

| SKS Technologies Group (ASX:SKS) | 29.7% | 24.8% |

| Propel Holdings (TSX:PRL) | 36.5% | 38.7% |

| Pricol (NSEI:PRICOLLTD) | 25.4% | 25.2% |

| Laopu Gold (SEHK:6181) | 36.4% | 38.5% |

| On Holding (NYSE:ONON) | 19.1% | 29.7% |

| Kingstone Companies (NasdaqCM:KINS) | 20.8% | 24.9% |

| Plenti Group (ASX:PLT) | 12.7% | 120.1% |

| Fulin Precision (SZSE:300432) | 13.6% | 71% |

Let's dive into some prime choices out of the screener.

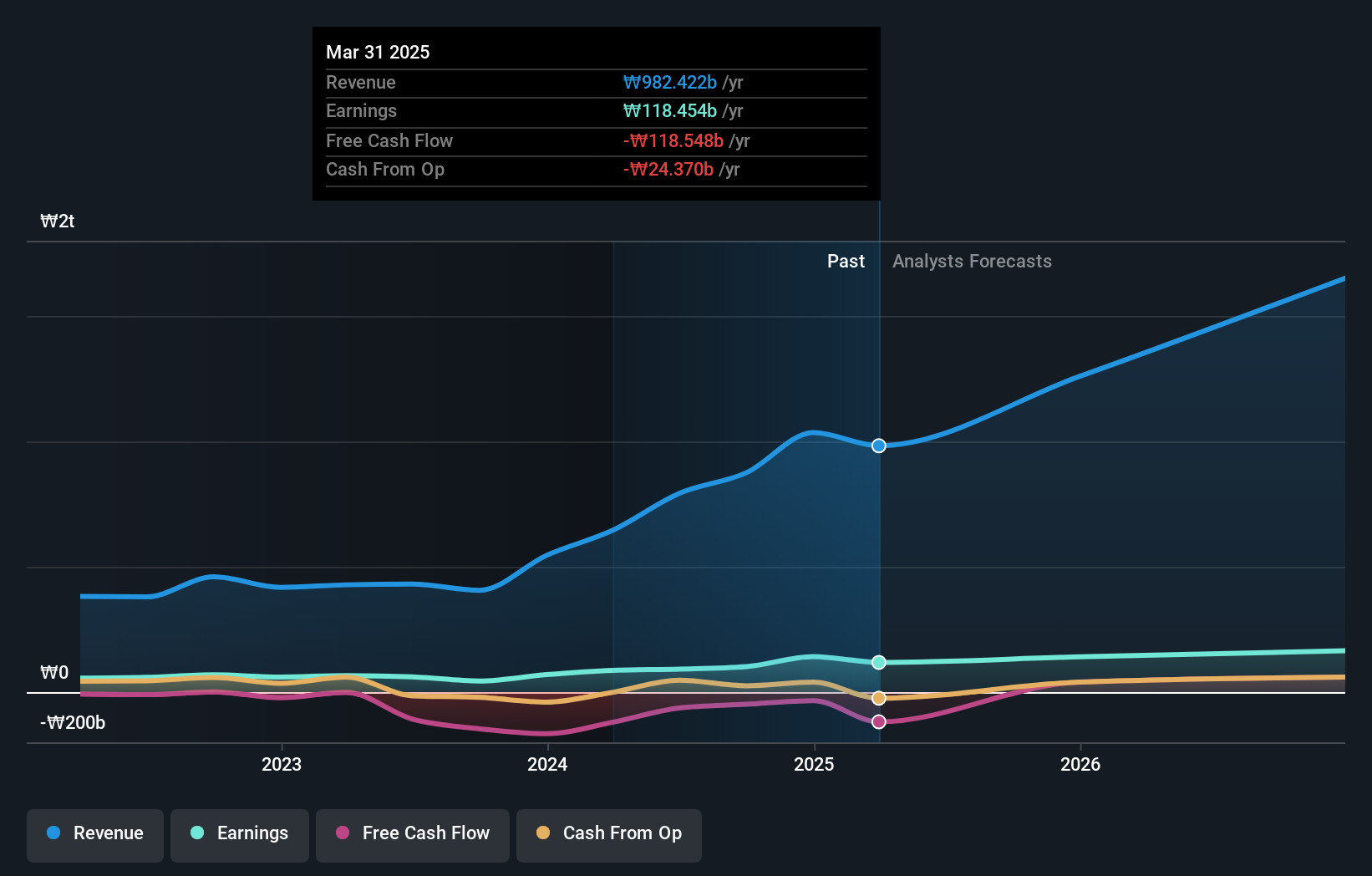

People & Technology (KOSDAQ:A137400)

Simply Wall St Growth Rating: ★★★★★☆

Overview: People & Technology Inc. provides coating, calendaring, slitting, automation, and other machinery solutions with a market cap of ₩1.08 trillion.

Operations: The company generates revenue of ₩874.54 million from its machinery and industrial equipment segment.

Insider Ownership: 16.4%

Revenue Growth Forecast: 28.5% p.a.

People & Technology is poised for substantial growth, with revenue expected to increase by 28.5% annually, surpassing the Korean market's average. Although its projected earnings growth of 22.5% lags behind the market, it remains significant and supported by a strong Return on Equity forecast of 21%. Trading at a notable discount to its estimated fair value and offering high-quality earnings, the company presents an attractive investment opportunity despite no recent insider trading activity.

- Navigate through the intricacies of People & Technology with our comprehensive analyst estimates report here.

- Our expertly prepared valuation report People & Technology implies its share price may be lower than expected.

Huayi Brothers Media (SZSE:300027)

Simply Wall St Growth Rating: ★★★★★★

Overview: Huayi Brothers Media Corporation is an entertainment media company operating in China and internationally, with a market cap of CN¥8.35 billion.

Operations: Huayi Brothers Media Corporation generates revenue through its entertainment media operations both domestically in China and internationally.

Insider Ownership: 17.5%

Revenue Growth Forecast: 41.2% p.a.

Huayi Brothers Media is set for significant growth, with earnings forecast to grow 110.47% annually and revenue expected to rise by 41.2% per year, outpacing the Chinese market average of 13.3%. Despite recent share price volatility, the company anticipates high profitability within three years and a strong Return on Equity of 38%. Recent shareholder meetings focused on strategic share offerings and stock option incentives suggest active management engagement in driving future growth initiatives.

- Dive into the specifics of Huayi Brothers Media here with our thorough growth forecast report.

- In light of our recent valuation report, it seems possible that Huayi Brothers Media is trading beyond its estimated value.

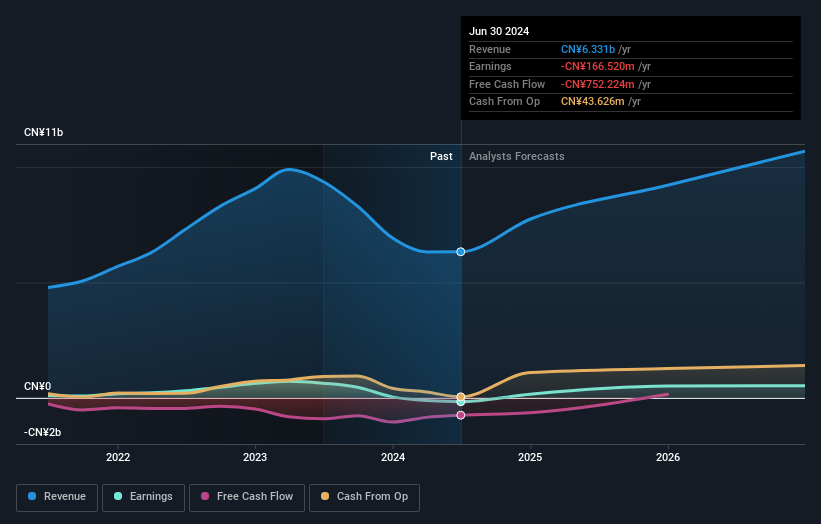

Guangzhou Great Power Energy and Technology (SZSE:300438)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Guangzhou Great Power Energy and Technology Co., Ltd engages in the research, development, production, and sale of various batteries in China with a market capitalization of approximately CN¥14.73 billion.

Operations: The company generates revenue primarily from its Batteries / Battery Systems segment, amounting to CN¥6.84 billion.

Insider Ownership: 34.5%

Revenue Growth Forecast: 18% p.a.

Guangzhou Great Power Energy and Technology is poised for substantial growth, with earnings projected to increase by 78.69% annually, surpassing the Chinese market's average revenue growth of 13.3%. While its revenue is expected to grow at 18% per year, insider trading activity has been minimal over the past three months. A recent shareholders meeting addressed potential project investments and audit firm reappointments, indicating ongoing strategic planning despite a forecasted low Return on Equity of 9.3%.

- Get an in-depth perspective on Guangzhou Great Power Energy and Technology's performance by reading our analyst estimates report here.

- Insights from our recent valuation report point to the potential overvaluation of Guangzhou Great Power Energy and Technology shares in the market.

Where To Now?

- Investigate our full lineup of 1465 Fast Growing Companies With High Insider Ownership right here.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:300438

Guangzhou Great Power Energy and Technology

Researches, develops, produces, and sells various batteries in China.

Reasonable growth potential with mediocre balance sheet.

Similar Companies

Market Insights

Community Narratives