- South Korea

- /

- Industrials

- /

- KOSDAQ:A052300

There May Be Reason For Hope In CT property's (KOSDAQ:052300) Disappointing Earnings

The market for CT property Co., Ltd.'s (KOSDAQ:052300) shares didn't move much after it posted weak earnings recently. We did some digging, and we believe the earnings are stronger than they seem.

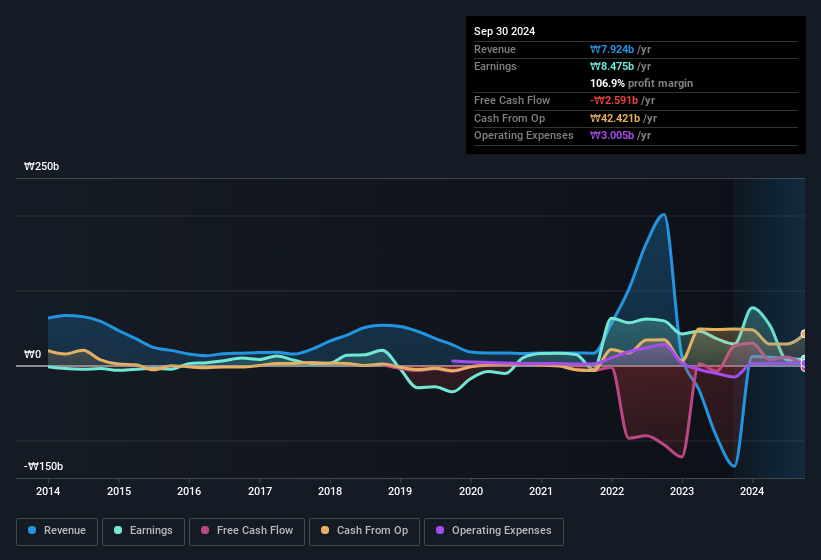

Check out our latest analysis for CT property

To understand the value of a company's earnings growth, it is imperative to consider any dilution of shareholders' interests. As it happens, CT property issued 17% more new shares over the last year. As a result, its net income is now split between a greater number of shares. Per share metrics like EPS help us understand how much actual shareholders are benefitting from the company's profits, while the net income level gives us a better view of the company's absolute size. You can see a chart of CT property's EPS by clicking here.

A Look At The Impact Of CT property's Dilution On Its Earnings Per Share (EPS)

CT property was losing money three years ago. And even focusing only on the last twelve months, we see profit is down 70%. Sadly, earnings per share fell further, down a full 71% in that time. Therefore, the dilution is having a noteworthy influence on shareholder returns.

If CT property's EPS can grow over time then that drastically improves the chances of the share price moving in the same direction. But on the other hand, we'd be far less excited to learn profit (but not EPS) was improving. For that reason, you could say that EPS is more important that net income in the long run, assuming the goal is to assess whether a company's share price might grow.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of CT property.

The Impact Of Unusual Items On Profit

On top of the dilution, we should also consider the ₩1.4b impact of unusual items in the last year, which had the effect of suppressing profit. It's never great to see unusual items costing the company profits, but on the upside, things might improve sooner rather than later. When we analysed the vast majority of listed companies worldwide, we found that significant unusual items are often not repeated. And that's hardly a surprise given these line items are considered unusual. CT property took a rather significant hit from unusual items in the year to September 2024. As a result, we can surmise that the unusual items made its statutory profit significantly weaker than it would otherwise be.

Our Take On CT property's Profit Performance

CT property suffered from unusual items which depressed its profit in its last report; if that is not repeated then profit should be higher, all else being equal. But on the other hand, the company issued more shares, so without buying more shares each shareholder will end up with a smaller part of the profit. Based on these factors, we think that CT property's profits are a reasonably conservative guide to its underlying profitability. So while earnings quality is important, it's equally important to consider the risks facing CT property at this point in time. Every company has risks, and we've spotted 3 warning signs for CT property you should know about.

Our examination of CT property has focussed on certain factors that can make its earnings look better than they are. But there are plenty of other ways to inform your opinion of a company. Some people consider a high return on equity to be a good sign of a quality business. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks with high insider ownership.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSDAQ:A052300

Ocean In WLtd

Engages in the glass, logistics, and real estate leasing businesses.

Flawless balance sheet and fair value.