- South Korea

- /

- Auto Components

- /

- KOSE:A012330

Earnings grew faster than the 16% return delivered to Hyundai MobisLtd (KRX:012330) shareholders over the last year

These days it's easy to simply buy an index fund, and your returns should (roughly) match the market. But one can do better than that by picking better than average stocks (as part of a diversified portfolio). For example, the Hyundai Mobis Co.,Ltd (KRX:012330) share price is up 14% in the last 1 year, clearly besting the market return of around 4.8% (not including dividends). So that should have shareholders smiling. Unfortunately the longer term returns are not so good, with the stock falling 1.6% in the last three years.

Since the long term performance has been good but there's been a recent pullback of 3.1%, let's check if the fundamentals match the share price.

View our latest analysis for Hyundai MobisLtd

There is no denying that markets are sometimes efficient, but prices do not always reflect underlying business performance. By comparing earnings per share (EPS) and share price changes over time, we can get a feel for how investor attitudes to a company have morphed over time.

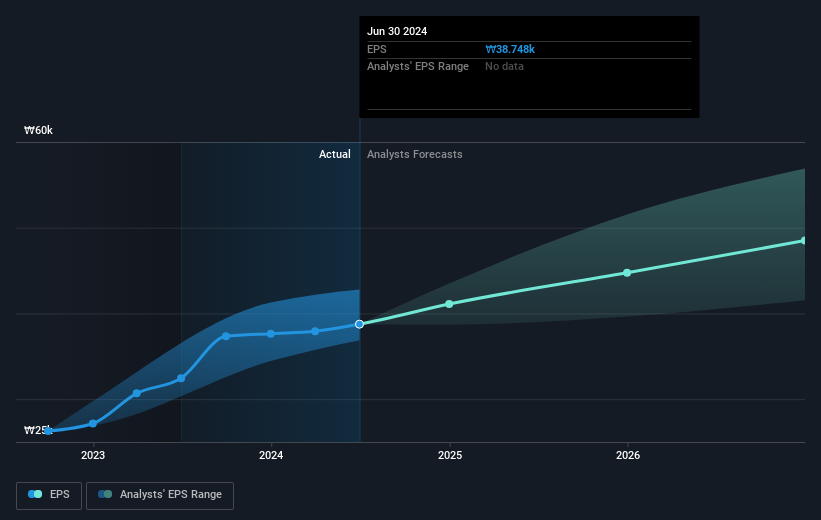

Hyundai MobisLtd was able to grow EPS by 19% in the last twelve months. This EPS growth is significantly higher than the 14% increase in the share price. So it seems like the market has cooled on Hyundai MobisLtd, despite the growth. Interesting. This cautious sentiment is reflected in its (fairly low) P/E ratio of 6.38.

You can see how EPS has changed over time in the image below (click on the chart to see the exact values).

We know that Hyundai MobisLtd has improved its bottom line lately, but is it going to grow revenue? Check if analysts think Hyundai MobisLtd will grow revenue in the future.

A Different Perspective

We're pleased to report that Hyundai MobisLtd shareholders have received a total shareholder return of 16% over one year. And that does include the dividend. Since the one-year TSR is better than the five-year TSR (the latter coming in at 2% per year), it would seem that the stock's performance has improved in recent times. In the best case scenario, this may hint at some real business momentum, implying that now could be a great time to delve deeper. I find it very interesting to look at share price over the long term as a proxy for business performance. But to truly gain insight, we need to consider other information, too. Take risks, for example - Hyundai MobisLtd has 1 warning sign we think you should be aware of.

For those who like to find winning investments this free list of undervalued companies with recent insider purchasing, could be just the ticket.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on South Korean exchanges.

Valuation is complex, but we're here to simplify it.

Discover if Hyundai MobisLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSE:A012330

Hyundai MobisLtd

Engages in the auto parts business in Korea, China, the United States, Europe, and internationally.

Flawless balance sheet and good value.

Similar Companies

Market Insights

Community Narratives